If you enjoyed today’s post, please hit the heart button and if you have any feedback, comment below.

Hi there, welcome to another earnings recap post by Cedar Grove Capital Management. Just a heads up, if you’re reading this in an email and it abruptly cuts off, that means it was too long to send this way so you’ll have to click through to read the rest.

Today we’re going to be going over earnings for two companies that I’ve talked about quite a bit over the last 1.5 years.

Xponential Fitness XPOF 7.41%↑

Peloton Interactive PTON -1.57%↓

One of these companies I have not completely taken a 💩 on which was Xponential Fitness. In fact, I was doing quite the opposite. This company was the one I was trying to get people on board with for the longest time. Going on podcasts talking about it, writing articles, and updates, and voicing how cheap it was on Twitter.

I literally made a post on June 22, 2022 where I visually outlined why it had immense operational leverage in its path of fitness franchise expansion in order to show people of its potential.

If you’d like a recap of this with nice pretty charts and visuals, you can click below, it’s free.

Since then, the stock has rebounded by over 163%, and before anyone says that “I just got lucky” with this stock seriously needs to go and read the post above because what I said was going to happen actually happened.

This isn’t me gloating since I definitely don’t bat 1,000 but one of the best things about this stock is that it’s not hard to understand the business, what drives it, and what was positioning it for success.

The reason I wanted to say this is that you don’t need to invest in tech to get tech-like returns.

So with that said, let’s dive into the recent Q1'23 earnings report and share my notes with you all.

Xponential Fitness (XPOF)

Aside from the stellar return that XPOF has had over the last 9 months, what’s important is understanding why it’s had the run-up that it’s had.

This all revolves around a few key points.

Were they going to get affected by an inflation slowdown and consumers ditching fitness in the name of saving money?

How have the number of studios grown and will continue to grow?

How much is each unit (studio) making (i.e. AUV)?

All of these were necessary to reverse sentiment, pop the stock but also keep the momentum going. Any slowdown in these metrics would not allow it to keep up the momentum it was having.

Now I’m about to throw a few charts at you just to show you how the KPI performance has been related to the points I made above.

First off, since this is a franchise, let’s first look at how studio growth has been since that is a sign of franchisee demand to get in.

While it has decelerated slightly, it still grew by 4.4% with over 2,000 studios now contractually obligated to open globally. This is despite interest rates from lenders rising between 0.25% and 0.5%.

It’s important to note that because of Xponential Fitness’s smaller box footage, the ability to still attract franchisees is still there since the cost to open one is much smaller than say a traditional gym like Plant Fitness PLNT -0.81%↓ which can go well over in excess of $1.5 million.

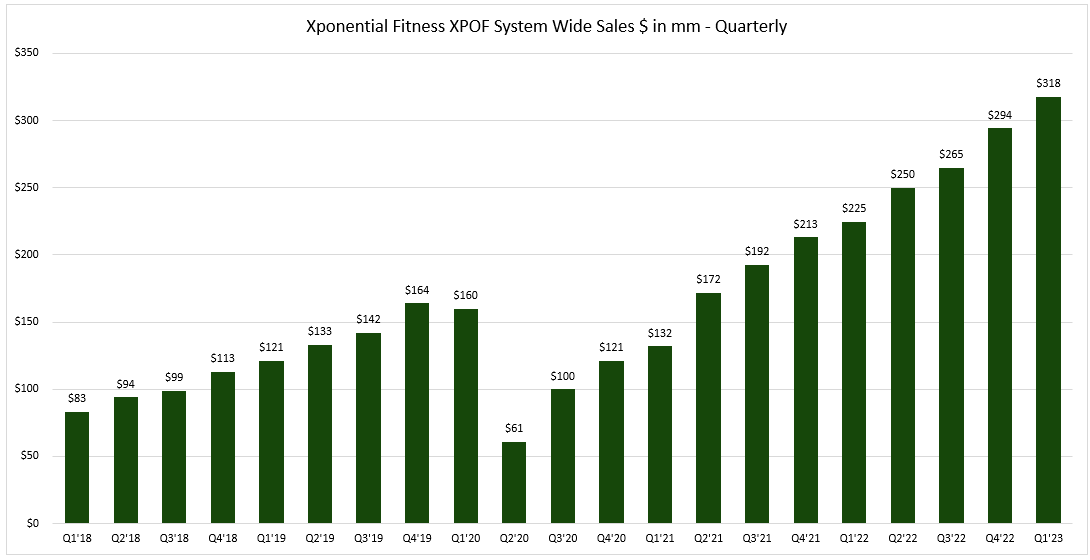

If we pivot to how much these studios have generated in system-wide sales, the number is equally as shocking.

Like in good fashion, it’s quite literally up and to the right posting a 41.5% jump YoY.

But while overall SWS were up over 41%, how did same-store sales compare?

Still posting double-digit growth on units that have been open for at least 13 calendar months.

And the last chart that I want to share with you is the average unit volumes (AUV). I’m going to specifically show you North American AUVs because that’s where the bulk of the studios are located and where they drive most of the SWS at the moment.

Another home run on the KPI front. So the notion of the consumer pulling back on fitness, while might be happening for Peloton (more on this in a bit), is not happening at Xponential Fitness.

“The acceleration in growth in our North American AUVs and same-store sales in combination with the growing membership base, demonstrates that consumers continue to view their health and wellness as a vital part of their budgets and not discretionary spend.”

- CEO Anthony Geisler

But I don’t want to make it seem like everything is rosy at the company right now. While these charts look great, the stock did come off its after-hours pop for what I believe could be a function of a few reasons.

The company did miss EPS estimates and while topline growth was still great, investors could have interpreted the earnings miss as a sign of taking longer to get to GAAP profitability.

Investors were expecting better free cash flow (ex-SBC) from the prior quarter (which was down) despite it doing better YoY.

Shares outstanding have ballooned and insiders are selling even though the CEO is on a share plan and the PE fund that owned XPOF prior to being public has been gradually selling its stake.

Regardless, XPOF has really proven why the rally it’s had since last summer is justified. They continue to execute expansionary efforts, not just domestically but also abroad, improving the revenue that each studio makes which directly decreases the payback period for franchisees and shows that not all fitness companies are built the same.

Despite the price action on earnings day, this one is still looking like a winner.

Peloton Interactive (PTON)

God, where do I even start? How about my thoughts when earnings came out?

I don’t try to be an asshole when it comes to Peloton, it just comes naturally since it’s just too easy to not be one. There were far too many people that wanted to really believe that connected fitness was here to stay. The stages of denial for Peloton went from

They’ll bounce back! People love their bikes! to,

Okay well someone will come around to buy them. Probably Amazon! to,

They just need to slow the cash burn so they can focus on growth again!

All of these were jacked up on hopium despite the last one being the most realistic.

At the end of October last year, I shared my thoughts on the company and why I thought expectations were overblown. You can check it out below if you’d like.

Despite my warnings and consistent negative tweets, the stock is actually now down ~13% YTD despite the short squeeze that happened at the beginning of the year. The same short squeeze that took me for a ride.

But how bad were earnings? Well, in my opinion, pretty bad. Let’s dive in.

Connected Fitness Subs & Growth

Connected fitness subscribers are people who own a Peloton product, such as its Bike or Tread, and pay a monthly fee for access to live and on-demand workout classes.

CF Subs are the bread and butter of the company. It’s what many bulls have been leaching onto as if were the last lifeboat on the Titanic that will get them to safety.

They’re not wrong, the subscription gross margin hovers around the ~68% range, though this was a contraction of (40bps) YoY but a +20bps QoQ.

If the company can get more connected fitness subs, then they can get better operational leverage through this channel stream to really get sticky, recurring revenue.

However, this is the issue that I have with it. It heavily relies on customers’ access to get the bikes. This is why the company has cut prices, brought back S&H charges, introduced lower-priced offerings, and even brought on a new program launched last year that gives people the ability to rent the bike instead of outright purchasing it upfront.

While this may have helped during last year’s “throw everything out but the bathroom sink”, I don’t believe that it can last much longer.

While subscription revenue is increasing at (1st image), connected fitness product revenue is decreasing which means the growth factor of getting new CF subs in the door is going to be tough.

This was actually confirmed in guidance when McCarthy said

“This upcoming quarter will be among our most challenging from a growth perspective.”

and gave new guidance of 3.08 million to 3.09 million CF subs. It’s actually marked the first time that Peloton has guided for a decline in CF subs.

The reason this is important, besides the obvious is that even though the company added ~74k CF subs, the number of members on the Peloton platform actually didn’t change at all and remained at 6.7 million.

We’ll see how this bodes well with many Americans traveling this summer and probably doing many things other than wanting to stay home and workout.

Cash & Free Cash Flow

What’s good though is PTON’s cash balance and burn rate. In Q2’23, PTON ended with $871 million in cash and cash equivalents and an undrawn $500 million revolver.

Good because if they needed it they can certainly use it if needed. Fast forward to the most recent ER, cash and cash equivalents are now $873.6 million with an amended $400 million revolver.

Free cash flow burn has materially decelerated, mainly from the over $1.7 billion in restructuring charges the company endured in 2022, and even though SBC made up ~$250 million in add-backs to adjusted EBITDA.

Interpret that how you want but that sucks. I’m not trying to find reasons to hate the stock, there are plenty of them just by scratching the surface but what Barry has accomplished so far to stem the bleeding is pretty amazing.

I made a joke last year about when the market would bottom and how it was tied to Peloton.

Given that it’s gone as low as $6.62, perhaps the market bottom isn’t that far off.

Hell, even the bond has come off the recent start-of-the-year highs.

Until then, I’ve already closed my short and should it get cheap enough for a buyout target, I could change and go long purely off of a speculative trade.

I think the whole thing is radioactive and really wouldn’t touch it in the short term with all the macro stuff going on and the fact that they had to recall 2.2 million bikes due to a defect which I think is a laughable joke.

Until next time,

Paul Cerro | Cedar Grove Capital

Personal Twitter: @paulcerro

Fund Twitter: @cedargrovecm

HoldCo Twitter: @cedargrovech