As disclosed in my May 12th post, I held a long position in Mama’s Creations (MAMA) and still do. This company is not sexy and does not require you to understand a complex industry, factor in geopolitical exchanges, or even how AI will impact the business.

No, this is one boring business but it’s a business that’s made its mark by selling (at first) Italian meatballs to grocers, supermarkets, clubs, and C-stores across the country. In the last year alone, the stock is up >111%, +420% in the last 2 years (when the transformation started taking place), and ~27% YTD.

If you’ve been following the story, you’d know that there is no surprise that under the helm of Adam Michaels (CEO), MAMA has been able to grow topline 11%/quarter for the last 10 quarters and improve LTM FCF/share by 10x over the last 7 quarters.

But while you might ask yourself how much more juice is left to squeeze out of this lemon, I believe that MAMA is looking to be a steady growth investment with lower volatility than other hot stocks out there.

With continued management execution on growth and reinvestment, I think there’s a path to stock surpassing $10/share in the coming years. In this post, I’ll go over

Top sales growth drivers

Reinvestment for margin expansion

Potential Future Value

However, before I get to the future of the company, we first need to understand what happened that led to MAMA having their share price rise over 4-fold in just two years.

The Transformation Under Adam

Mama’s Creations, formally known as Mama Mancini’s, is a marketer and manufacturer of fresh deli-prepared foods that can be found in over 8,400 grocery, mass, club, and convenience store locations across the U.S.

| Seeking Alpha")

While the above is just a sample of what they offer, they actually sell over 50 different products from their 3 different brands: Mama Mancini’s, Creative Salads, and Olive Branch.

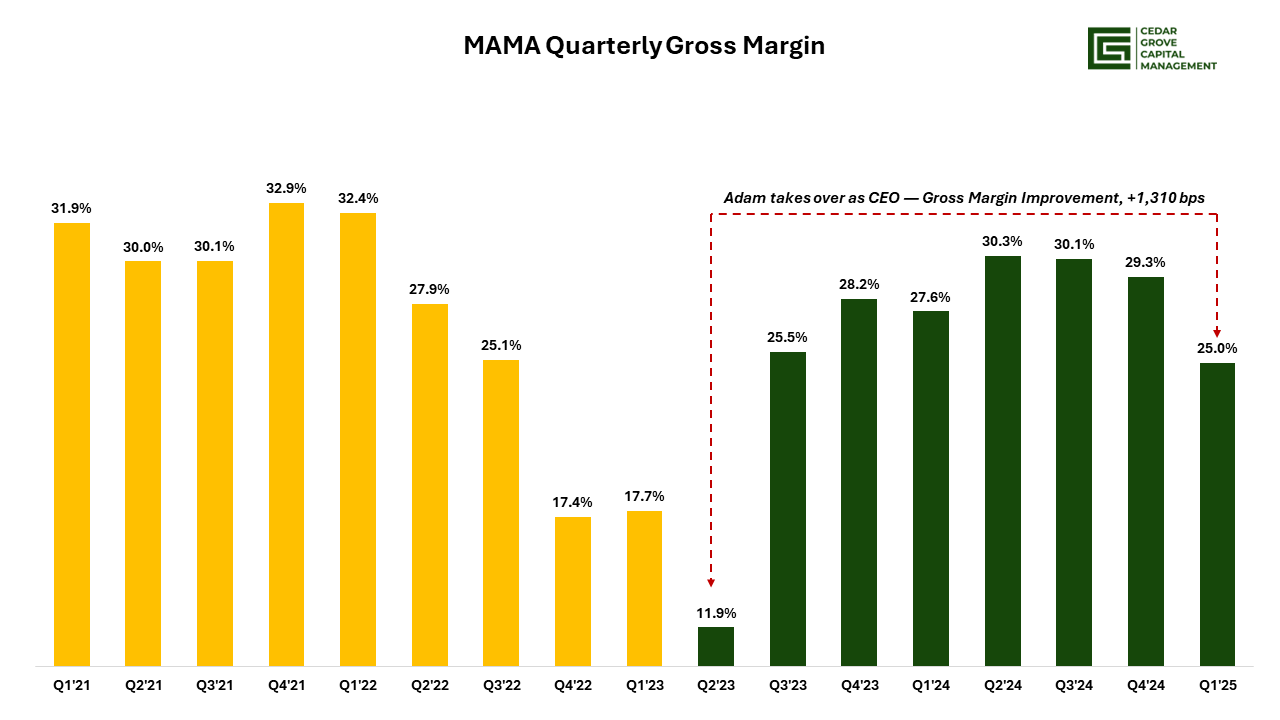

Prior to Adam taking over, sales were still growing but margin improvement below the line was lackluster and FCF generation was failing to impress. Adam comes in the summer of 2022 with an emphasis on improving operational efficiencies and setting up the future of what MAMA will be.

This came in the form of, to name a few

Equipment/technology investment

Optimizing labor costs

Price increases

Product penetration

Accretive M&A

Customer expansion, etc

Adam was able to and continues to introduce new equipment that helps optimize production capacity and cut down on overtime hours (labor cost), negotiate better terms with suppliers, and leverage strategic price increases on customers.

Since Adam took over at the end of summer 2022 (FY’23 - Q2), the company has been able to ramp gross margins back up to near-peak Covid levels by ~1,310 bps. In tandem, FCF/share has also increased nearly every quarter since he took over and the company’s balance sheet is healthy and leverage is going down.

So where do I see the company going after the run-up it just had? It all starts with doing more of the same. Let’s begin.