TL;DR

Having originally agreed to be acquired for $61/share in cash by Amazon in 2022, the deal price got revised down over the summer to $51.75/share

Given the FTC’s assault on big tech, Amazon is coming under fire for its history of anti-competitive practices on the Amazon website, thus putting the deal at risk

What was a rumored sure thing from the EU commission, they have changed their tune on the matter and believe that Amazon owning IRBT would lead to anti-competitive practices

Given IRBT relies heavily on user data to map out their homes, the other questionable point comes in whether should Amazon have access to that level of user data

As you can see, iRobot IRBT 0.00%↑ has had quite the rollercoaster of an acquisition journey. Here are some key dates to be aware of:

8/5/22 - Amazon AMZN 0.00%↑ agrees to acquire IRBT in an all-cash deal valued at $61/share.

9/20/22 - FTC makes second request for more information regarding the acquisition.

7/16/23 - UK clears AMZN to acquire IRBT.

7/25/23 - Deal gets revised down from $61/share to $51.75/share, mainly driven by IRBT taking on a new $200 million credit facility to continue operations.

11/24/23 - Reuters announces that unconditional approval from the EU is imminent.

11/27/23 - EU says the deal raises antitrust concerns.

Needless to say, there’s been quite a lot of ups and downs for iRobot over the last 14 months. Regardless, I’m going to break down what’s been going on for this deal, the concerns raised by each commission, and any counterpoints to the risks.

Deal Mechanics

On top of the acquisition prices that I quoted earlier, we need to look at the original timeframe and terms of the agreement between both parties. In a filing from August 5th, 2022 (below), we can see that they marked the timeframe for “possible” termination after August 4th, 2023 — so 1 year from the original announcement date.

Additionally, in regards to the termination fee, iRobot would be entitled to receive $94 million under a few circumstances

It takes longer than an additional year for the deal to close (two, 6-month extensions) to satisfy antitrust conditions.

Under appeal, Amazon still loses.

Not bad and to put this into perspective, at the original offer price on August 5th, 2022, the termination fee was ~5.8% of the total market cap. Fast forward to the recent close and that fee is now ~8.6% of their total market cap.

So both parties still have time for the deal to go through but given that the EU Commission opened an investigation on July 6th, 2023 and the FTC has been on the case since a month after the initial announcement, I don’t believe that it will take that full year to satisfy.

The EU has even said that they have until February 14th to make a final decision on the matter.

But let’s talk about why there are even issues about this deal and the implications of each.

Antitrust Concerns

While the title of this section is very broad, there are a few sub-categories specifically that we need to talk about that directly lead to the EU and FTC having antitrust concerns.

Competition & Pricing Power

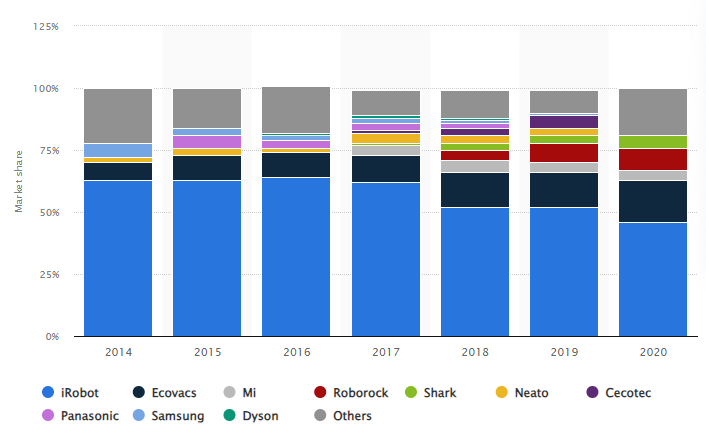

So when it comes to competition, several robot vacuums on the market are similar to iRobot. According to Statista, robot vacuums at the price point of $200 or more account for roughly $3.39 billion in 2020. Granted with the implications of COVID, that number has certainly gone up dramatically.

For well over a decade, iRobot fended off new entrants from some of the best-known names in vacuums — including Hoover, Black & Decker, and Bissell — and maintained its undisputed market leadership.

But even if we look at 2020 figures, iRobot only commanded 46% share of the market which I know many of you might read and think how could this deal ever happen? Don’t be too hasty though, that 46% worldwide share in 2020 is much lower than its 64% worldwide peak share in 2016, meaning that other players are doing well to compete with IRBT.

Take for example the Asian market. A company called Ecovacs Robotics is turning up the heat in its sphere of influence against IRBT. Ecovacs Robotics Deebot vacuum products range from 1,000 yuan to 6,999 yuan, or about $141 - $986 USD.1

In comparison, iRobot's two-in-one top-notch model, the Roomba Combo j7+, carries a suggested price of $999.99 in the U.S. — and is apparently not officially sold in China.

While I don’t believe the real problem of antitrust concerns comes from how much market share the brand has, it’s the fact that Amazon is the one buying them. For everyone living under a rock, Amazon has been under fire over the last few years for using its ability to price out competitors on the very same marketplace it charges businesses to sell while humorously selling its own goods.

This is no bueno with the FTC and frankly, businesses in general. In its lawsuit, the FTC makes a few key points here.

Anti-discounting measures that punish sellers and deter other online retailers from offering prices lower than Amazon, keeping prices higher for products across the internet. For example, if Amazon discovers that a seller is offering lower-priced goods elsewhere, Amazon can bury discounting sellers so far down in Amazon’s search results that they become effectively invisible.

Conditioning sellers’ ability to obtain “Prime” eligibility for their products—a virtual necessity for doing business on Amazon—on sellers using Amazon’s costly fulfillment service, which has made it substantially more expensive for sellers on Amazon to also offer their products on other platforms. This unlawful coercion has in turn limited competitors’ ability to effectively compete against Amazon.

Biasing Amazon’s search results to preference Amazon’s own products over ones that Amazon knows are of better quality.

So basically Amazon is a bully to anyone but itself. And that is one of the main reasons why the commissions have a problem with Amazon buying the company.

The fear would be Amazon buying up IRBT, giving it the leverage of superior logistics, cost-based pricing, and marketing treatment to assert market dominance.

Pulling from the EU Commission warning,

Amazon could demote other robot vacuum cleaners on its platform and promote its own products with such labels as “Amazon’s choice” or “Works With Alexa.” The commission also said Amazon may find it “economically profitable” to shut out rivals.

Not a good look, but this goes directly against what its neighbor, the UK Competition and Markets Authority (CMA) had to say about the deal which was that it wouldn’t result in a lessening of competition.

Remind you, that this is the same CMA that I covered greatly during the MSFT 0.00%↑ and ATVI 0.00%↑ acquisition. The hardballers I believe just wanted to pound their fists on the table to get a conditional win which is why I don’t think this thing happens without some concessions.

Data Harvesting & Privacy

Amazon is already in the home robot space under the Astro brand. That weird little Wall-E-looking thing that literally no one wanted, asked for, or trusted.

But while it doesn’t vacuum anything at the moment, it still has much of the foundational technology that iRobot has to run its equipment. Meaning, that it still maps out your home, listens to conversations, etc.

Giving Amazon the data to map out your living space down to the inch might sound like an invasion of privacy, probably because it most likely would lead to that.

I mean, it’s not the first time that a hardware company spied on its customers. Take Ring for example. The doorbell security company was featured on Shark Tank and later acquired by Amazon in 2018 for $1 billion. A suit by the FTC was in regards to employees having unrestricted access to the cameras and consequently spying on women with cameras placed in their bedrooms and bathrooms.

In May 2018, an employee gave information about a customer's recordings to the person's ex-husband without consent, the complaint said. In another instance, an employee was found to have given Ring devices to people and then watched their videos without their knowledge.

In February 2019, Ring changed its policies so that most Ring employees or contractors could only access a customer’s private video with that person's consent.

All of which as a consumer you don’t want to hear. So with Amazon’s security products through Ring and Blink, which gives access to audio and video, pairing this functionality with understanding your home might set people off.

When you think about how Amazon would even try to leverage this information, the only real obvious path is to potentially recommend things in your UX to fill up space in your home. Amazon has denied this, saying

We do not use home maps for targeted advertising and have no plans to do so.

However, According to iRobot, customers can opt out of having its robots store the layout of their homes.

iRobot co-founder and CEO Colin Angle said that

iRobot does not – and will not – sell customers’ personal information. Our customers control the personal information they provide us, and we use that information to improve robot performance and the customer’s ability to directly control a mission.

But when you want to talk about customer data, Amazon was still cleared to acquire One Medical which arguably is way worse considering that the data under that company is all healthcare-related information, albeit protected (allegedly) under HIPPA.

So while we probably wouldn’t want Amazon to have more of our data, legally speaking, there isn’t much in the direct path of why they shouldn’t be allowed to. And in the courts, that’s all that matters.

If The Past Says Anything

One of the best POVs to look at is when you can see what deals have been allowed to pass through regulatory scrutiny, and Amazon has not been shy with its buying.

The announcement of the iRobot deal follows Amazon's previous acquisitions of Kiva Systems in 2012, Evi Technologies in 2013, Blink in 2017, Ring in 2018, One Medical, and MGM in 2022.

But let’s take a look at One Medical for a moment because there’s a key part that I believe applies to this.

When Amazon closed its $3.5 billion takeover of primary care provider One Medical in February, the FTC sent a warning letter citing specific concerns about the transaction but took no future steps.

The key part is “took no future steps.”

This is very similar to how the EU sent its warning letter (charge sheet) to Amazon last month. While Amazon might still gain unconditional approval to buy iRobot, the charge sheet indicates that officials are looking for remedies from the company to address their concerns.

This is why I don’t believe the deal will be struck down by the EU but rather, worst-case scenario, there will just be some concessions.

Pivoting to the FTC, they’ve been investigating the deal since last year and despite the multiple requests haven’t come back with anything meaningful as to why the deal should be blocked. Not that they still can’t but after 15 months, if you haven’t come points yet, the odds of you coming with any at this stage are unlikely.

Granted, this IRBT deal is unique because while there are plenty of instances where a big tech firm has bought product-related companies, IRBT commands a large market share in the industry.

Conviction or Lack Thereof

To evaluate arbitrage situations, you must answer four questions:

How likely is it that the promised event will indeed occur?

How long will your money be tied up?

What chance is there that something still better will transpire -- a competing takeover bid, for example?

What will happen if the event does not take place because of antitrust action, financing glitches, etc.?

To the first point, there’s still a large spread from Friday’s close to the amended closing price to the tune of about 32.5%. Given the concerns from the commissions, and one of them already signing off, I believe the deal will go through, conditionally.

I’ve provided an unbelievably simple representation of how I feel each commissions odds of approving the deal below.

The additional reason why I’ve applied such weight besides what I mentioned above is because of the way the stock price has reacted given both a) Reuters announcement of pending unconditional approval and b) when the EU announced it had issues.

In the span of 1 month, the price is already almost back up to where it was post Reuters making that announcement. This leads me to believe that investors digested both the good and bad and believe that the charge sheet will allow Amazon to ensure changes or conditions in order for the deal to go through.

To the second point, given EU Commission says they’ll have a decision by Feb 14th, we can most likely expect the FTC to follow suit shortly after with theirs if they haven’t given it by then. I suspect ~3 months timeframe is a realistic pathway without considering any appeal filings.

The third point is null, there’s no one going to be coming in to bid over this, mainly because that window has closed but also because if IRBT accepted, it would have to pay Amazon $56 million. Given its current financial status, that’s a no-go.

The fourth point is an interesting one because should the deal fall apart after appealing, the price of the company’s price will crater more than it already has since the announcement.

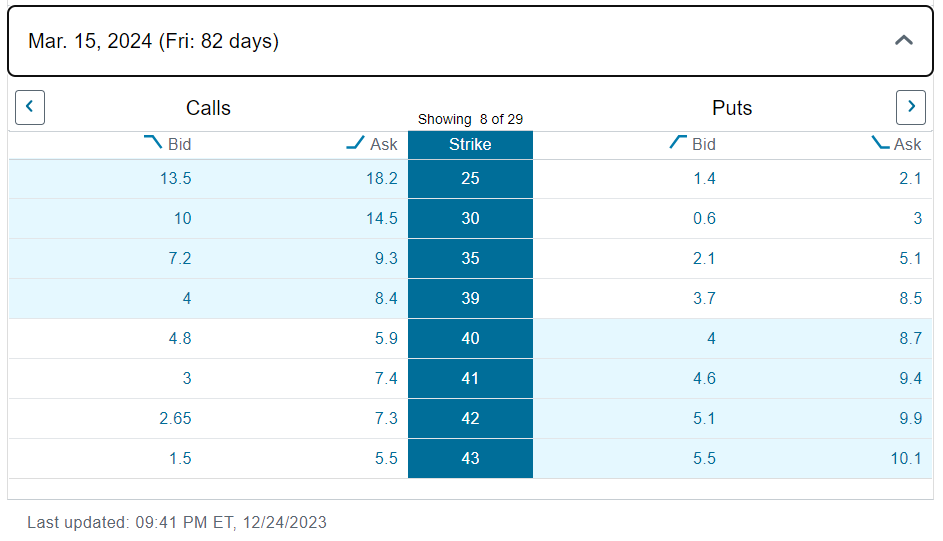

Looking at options chains 3 months out, things are still looking pricey.

There could be opportunities for an options trade but you’re going to have to determine your level of comfortability based on the premiums you’d be paying.

Bottom Line

This has already been a long and drawn out process but I believe that the end is in sight. The commissions will need to get comfortable that Amazon will make sure that pricing competition will not impede their competitors on the platform and consumers are protected from data harvesting.

While I believe there are remedies that can satisfy these conditions, IRBT getting almost 10% of its market cap in cash if the deal falls apart would support the fallout to a degree, though I would not be holding onto the stock in such a event.

Until next time,

Paul Cerro | Cedar Grove Capital

Personal Twitter: @paulcerro

Fund Twitter: @cedargrovecm