Background

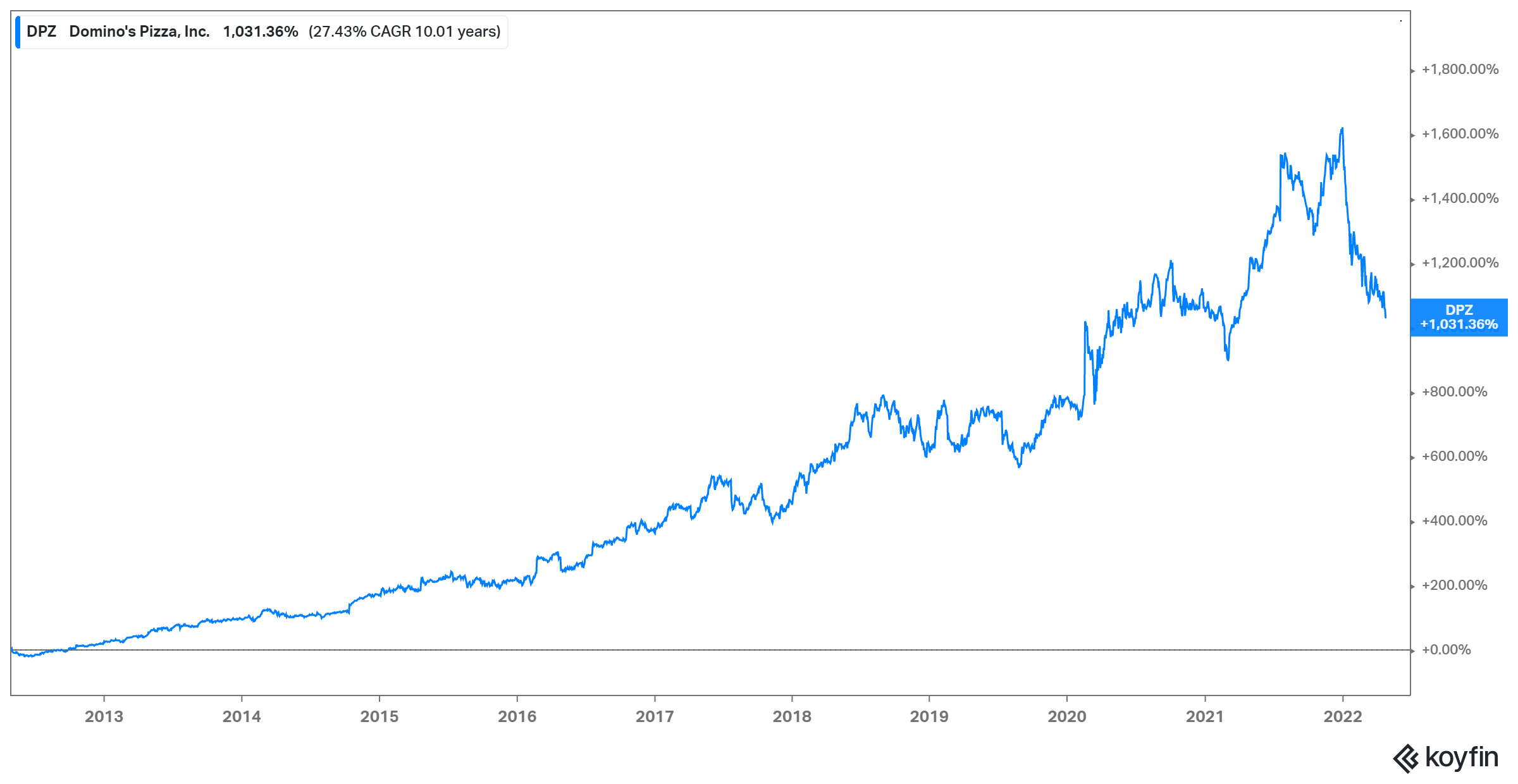

Domino’s Pizza DPZ 0.00%↑ has had a stellar run over the past decade, rising over 1,030% during that time. The company has shown its ability to rapidly expand overall store count, expand margins, and not only fend off app-based delivery companies but go toe to toe with them.

Underlying business fundamentals remain strong for the company and while headwinds with inflation have put pressure on the company, for now, recent price action has led to an attractive opportunity to start a position in a long-term compounder.

As part of my posts going forward, I’m trying to limit them to a short form deep dive instead of the 4,000+ word reports I typically write. With that being said, the following will be Cedar Grove Capital’s current quick viewpoint on the stock, while the attached investor presentation will be an expanded explanation of the overall business, its financial performance, and what has and will continue to drive future success.

TL;DR

The company is experiencing both commodity inflation pressures and increased labor costs putting a recent damper on the stock price

With the end of COVID lockdowns, consumers hungry for experiences, and tough 2021 comps to beat, many on the street expect Domino’s to experience lackluster growth during 2022

Domino’s is a strong brand, a great compounder, and with a price decline of already 35% YTD, and a modest dividend yield of just over 1%, ~$700 million left in its current share repurchase program, pricing power, and international runway, it’s hard to ignore the company at these levels.

While we believe that management’s recent measures can help offset some near-term costs, price volatility is a very real concern but a healthier and stronger DPZ seems in the cards for 2H.

2021 Full Year Results

To give you quick context before we dive into our LONG thesis, we’ll go over key business/financial results and management commentary from the earnings call.

Business & Financial Highlights

Same-Store-Sales

SSS growth was mixed with U.S. stores growing +3.5%

U.S. company growth declined (3.6%)

U.S. franchise growth increased +3.9%

International SSS grew +8.0% for the year

Store count

Grew net new units +1,204 to end the year with 18,848 global stores

999 of those stores were international while 205 were U.S. based (193 franchise stores and 12 company-owned)

Sales & other

Global retail sales reached $17.8 billion in 2021, up 11.7%, excluding the impacts of foreign currency and the 53rd week compared to 2020

Diluted EPS for fiscal 2021 was $13.54, an increase of 9.3% over the prior year

Generated $560 million in free cash flow, up +36% from 2019

Share repurchases for the year totaled $1.32 billion (~2.9 million shares and an average price of $453) and there is a remaining share repurchase program balance of $704.1 million

Dividends totaled $139 million in the form of quarterly $0.94/share payments including two dividend payments totaling $68 million paid in Q4

Select Management Commentary

While overall results weren’t bad, they also weren’t great. Management commentary led many to believe that the effects of commodities and labor shortages would increase during 1H and lead to some margin compression.

Costs (Food + Labor)

We currently project that the store food basket within our U.S. system will be up 8% to 10% as compared to 2021 levels. We previously told you that we estimated that changes in foreign currency exchange rates could have a $4 million to $8 million negative impact on royalty revenues in 2022 as compared to 2021. Based on the current outlook, we now estimate that this could be an $8 million to $12 million negative impact. - Jessica Parrish, Controller & Treasurer

When it comes to SG&A, Richard Allison (CEO) mentioned how they expect wage increases to continue going forward into 2022

In our corporate stores during 2021, we rolled out increases in team member compensation and benefits totaling more than $6 million over and above required minimum wage increases. In 2022, we are currently anticipating committing an incremental $8 million investment in team member wages over and above required 2022 minimum wage increases in our corporate stores.

Labor Challenges

Domino’s also is suffering from a labor shortage not just for its stores but also for its delivery driver network which does not use third-party apps.

Second, we saw staffing challenges intensify across the country as the year progressed, resulting in reduced operating hours and other service-related challenges in many stores across the network. We saw that urban markets were generally more impacted than our rural markets. We believe these staffing challenges posed a more significant headwind on orders and sales during Q4 than they did during Q3 and much more so than in the first half of the year.

Given numerous pressures from all sides directly leading to the stock’s recent decline, we believe this opens up a buying opportunity for a great company with a long successful track record.

The Value in Domino’s

Domino’s has shown since its total company overhaul over a decade ago that Americans and foreigners love their pizza, and that the company has found the right product-market fit for what they offer.

But contrary to what many think, Domino’s does not just offer pizza. No, what they offer is far more than just a cheesy slice of bread with sauce and toppings. They offer the consumer three main things that have led to its massive growth and expansion.

Speed

Convenience

Affordability

1) Speed

Domino’s is known for just how fast they can get their pizza to your door and ready to eat. It takes a pizza maker just 1-2 minutes to prepare the dough and spread the toppings and another ~7 minutes to cook the pizza. If you’re picking up your pizza, it can be ready in under 10 minutes and if you’re waiting on a delivery, it can take up to 30 minutes on average.

Some of these pizza makers are so fast that one worker was able to make three large pizzas in an impressive 47.56 seconds. Pretty wild and I’ve included the link here for you to check that out.

2) Convenience

What the company has prided itself on, and also pioneered, was making it so simple for a customer to order a pizza. They were one of the first to implement and invest in digital ordering through their own native app which helped the company shift from less efficient phone orders to a more efficient digital process.

Because the company made it so easy to request your order for carryout or delivery with a few simple clicks, many found Domino’s a great dinner option from the working family all the way to a college student’s dorm. This translated to 75% of U.S. retail sales being completed through their online digital channel.

3) Affordability

One of the main things that I love about Domino’s is how affordable it is. This is not to be mistaken exclusively for quality as I’m sure I will get much push back on this. Domino’s is not going against your local pizza restaurant, they are going for lower and middle America (and internationally) that want quality pizza at a great price.

I mean, I’m Italian and I would go to my local pizzeria for a pie but here in NYC that cost starts at ~$20 and can go much higher depending on what toppings I pick. For Domino’s, you can get two medium 2-topping pizzas for $5.99 each (~$13 with tax). How do you beat that? You can’t. And that’s why there will always be a product-market fit for them.

But these aren’t the only things that the company has going for it. While doing my research, there were a few interesting callouts that I believe warrant enough attention as to what makes Domino’s such a great franchise.

The Franchise Itself

What I love about the Domino’s franchise is that 95% of franchisees started off by delivering pizza. Talk about an owner that’s worked their way up. Having a skilled operator of these restaurants is definitely a big help but there’s more to love about it.

If we look at the average AUV of U.S. Stores, it’s surpassed $1.3 million in 2021 and even international stores are approaching the $1 million mark.

If we look at store-level EBITDA, U.S. stores back in 2010 were $67k, and in 2020 they were $177k (est) representing a 10-year CAGR of 10.2%.

Additionally, given the average cost to open one in the U.S., we’re looking at cash-on-cash returns of >40% and internationally, cash-on-cash returns are averaging under 3 years.

International Growth

While some might argue that domestically, store footprint has a limited runway, internationally this is far from the case. Having posted 112 consecutive quarters of SSS growth, the franchise overseas is on fire.

Looking at the company’s investor presentation, the amount of whitespace abroad, specifically in emerging markets is ~3x from current levels. With ~7,500 stores left in emerging markets generating close to $1 million in AUV per store, that’s close to $7 billion in incremental revenue per year in the long term.

Loyalty Program

Domino’s has a “Piece of the Pie” loyalty program where you can earn points based on your orders (with a valid account) which allows customers to continue coming back and using the service. There’s plenty of data out there about how consumers treat loyalty programs with a points factor and a pizza-oriented one is no different.

The company boasts of having over 20 million active users on the program with over 70 million enrolled, so their marketing list is quite extensive should they want to push any new and exciting promotional offers to spur demand.

2022 Headwinds

But in the face of so many inflationary headwinds, what does Domino’s currently have in its arsenal to leverage? Well, a few things.

Pricing Power

One thing that I love about a company is having true pricing power. However, at least in the world of Fintwit, it seems that many skipped Econ 101 in school and do not actually understand what pricing power actually means.

Pricing power only exists if the company has the ability to raise prices on its goods/services without having demand destruction. I believe that Domino’s has this.

If you think about it, their biggest national offer (Mix & Match deal - 2 for $5.99 each) is quite a compelling offer. Should they raise it by say, a $1 to $6.99 each, do you think that there will be demand destruction enough to offset the price increase? No.

You move a total bill of ~$13 after tax to ~$15. Not that bad and you still get the same level of speed, and convenience.

Emphasis on Carryout

In the world of convenience and digital ordering, so many companies and applications have conditioned us to order virtually anything we want for delivery. Things as simple as a soda can be delivered via Gopuff because we’re that lazy. But what if we went back to moving our feet (or car) and picked up our order instead if it were cheaper?

Domino’s believes that going back to pickups could be a winning factor for future growth. In fact, on a per ticket basis, online carryout orders are 25% higher than phone orders. Management even said,

The carryout business opportunity is 2x that business in pizza than delivery. And so we want to be aggressive there.

But what if there was an incentive on top of your pickup order to help motivate/convince you?

Domino’s has done just that. With the driver shortage posing a near-term issue for the company, they’ve taken a few measures to promote us, the consumer, to come to pick up our order instead.

First, they’ve added a $3 “tip” for each online carryout order to be used on the customer’s next order (ends May 22). This means that I can order online for a pickup and get $3 in credits to be used on my next order if I just simply go and get it instead of getting it delivered.

This definitely helps lower-income families and individuals that might be feeling inflationary pressures on their wallets. Since a portion of this $3 would be paid out to the driver, it helps offset labor costs while creating repeat business.

Secondly, they’ve further incentivized one of their national offers. The two for $5.99/each deal is now only that price if you order for carryout. Should you choose to select delivery, the price is now $6.99/each. Two things arise from this change, 1) you can incentivize people to go pick up their order to save a few bucks (i.e. not having to pay for the increase in price but also getting the $3 tip), and 2) this helps offset costs both on the commodity side and labor shortage side.

Lastly, as of late January, the company’s signature $7.99 deal is exclusive to online only and is a carryout offer.

These combined changes, $3 tips, increased prices for delivery, and the signature deal being online carryout only should help offset rising input costs somewhat in the first half of 2022.

Recession Beneficiary

Another thought that is in the back of everyone’s minds is how well will the company do if a recession comes. Well, we all know when recessions do come, consumer spending rolls back dramatically. But when it comes to food, where do consumers shift to?

According to BLS data, the CPI relative importance of Food goes up during recessionary environments but then goes back down. What’s interesting to note is the slight drop in the limited-service food away from home category. This leads me to believe and partially helps validate that while consumers will still go out to eat, they will be more choosy with where they go.

If we look at Chipotle CMG 0.00%↑ and McDonald’s MCD 0.00%↑ for instance from January 1, 2007, to April 26, 2010, their stocks actually outperformed the S&P 500 dramatically.

Granted, I did leave DPZ out because they had not gone through their total company transformation yet and that this was a different type of recession, but nonetheless, money spent in tight situations still flows to certain areas.

Regardless, I believe that the new Domino’s would be a great beneficiary of a possible recession (should one come).

Valuation

The biggest question that anyone is asking these days is, “how much is it worth?” Well, if we look back in time, the median NTM P/E multiple over 10 years was 29.1x, 5 years was 30.4x, and 30.6x over the last 3 years.

Given how the company is trading for less than that at the current moment, a potential multiple expansion could be warranted later in the year should conditions improve.

However, I believe that 2022 is too much of a risk to price anything appropriately. I’m instead opting to price DPZ based on 2023E EPS of $16.43 with a modest multiple of 28x. This is just two turns above where it currently is trading at and two turns less than the 5-year median considering it is a mature business.

Even at these levels, you’re still getting ~$460/share with near term price risk of ~$303 based on $13.53 EPS and 22.5x multiple. The risk-reward at these levels looks like something worth chewing.

If you have any thoughts or comments, feel free to hit reply, and don’t forget to sign up for the newsletter via the link below.

Until next time,

Paul Cerro

Cedar Grove Capital