WW Update: Survey Says, More Pain Ahead

Recent ER suggests there's more pain to come in this pivot-play

Factoring the after-hours price movement, WW 0.00%↑ is down:

75% from when I started the short position (albeit covered much too early)

68% YTD and,

50% since my public post.

In my above post, I highlighted my thoughts on why WW was grossly overvalued and the company was due for a plunge. Mainly,

The core business decline will continue putting downward pressure on the overall company before a successful (if successful) pivot can be properly rewarded.

The ramp-up of WW Clinical (formerly Sequence) isn’t enough to save them let alone justify the valuation at the time.

Lastly, a bloated balance sheet. Not from the perspective of a maturity wall but from the variable rate debt should operating earnings decline.

Don’t get me wrong though, I have nothing against the company or what it’s trying to accomplish. In fact, I understand the pivot that Sima is trying to do mainly because it’s necessary. If not, WW could very well end up in the bankrupt graveyard with the likes of Jenny Craig1, Atkins International2, LA Weight Loss3, and Nutri-System4.

This is quite the, “adapt or die” situation, and I have to respect the awareness to do so. However, that doesn’t mean I had to be comfortable with the price.

Yesterday, WW released its earnings and the stock was sent down ~27% in after hours.

I believe there were 3 main contributors to this decline.

Revenue & EPS miss (rev miss $.91 million and EPS miss of ~$1.02).

Guidance showing continued overall growth decline.

Oprah seemingly cuts her losses.

Guidance was incredibly lackluster. Revenues are expected to be down once again, to $845 million at the midpoint with operating income down to $105 million at the midpoint.

Compare that to my pessimistic predictions and you’ll see just how bad that is.

Combine that with Oprah not looking for re-election to the board and donating her WW stock to the National Museum of African American History and Culture, it’s not hard to see why the stock dropped so much.

Having once been the new image of WW, having your star brand ambassador throw in the towel, the vote of confidence isn’t strong with this one amongst investors.

Additionally, the interest rate swaps on their debt ($500 million notional) is expiring at the end of Q1’24 (Mar 31).

On the earnings call, Heather Stark (CFO) made a note that they’re currently looking at alternatives to hedge but given the high interest rate environment, nothing looks favorable at the moment.

However, despite this, there were some bright spots.

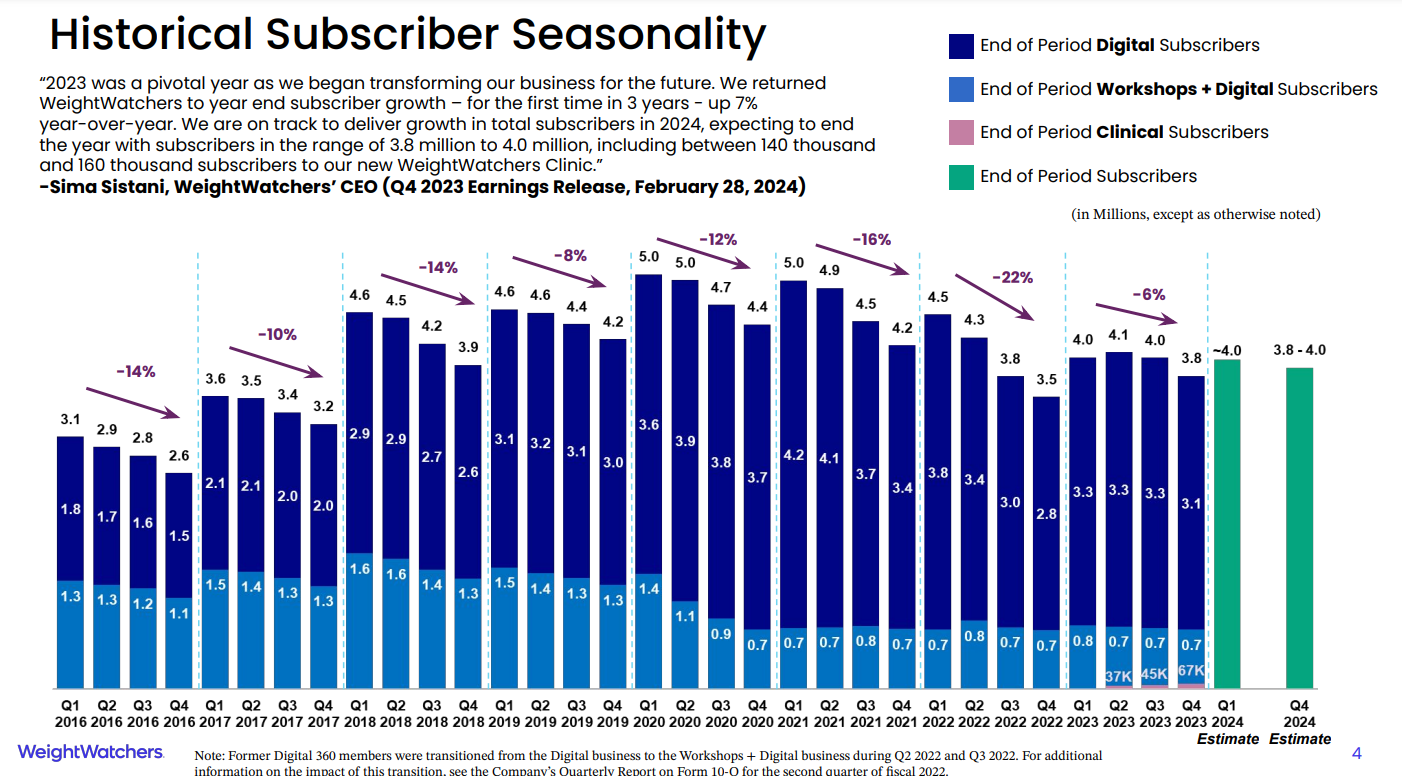

First off, they seemed to stem the bleeding a bit in core subscribers declining through the year at the slowest clip (-6%) in almost a decade.

I’ll caveat this with it’s most likely due to clinical subs pairing their weight loss services together which is why management believes that subs will likely remain flat by the end of 2024.

Secondly, I was surprised about where the company ended with clinical subscribers (67,000). That was nearly double my estimate of 38,000.

What’s more encouraging is their confidence in their ability to end 2024 with roughly 145,000 clinical subscribers. ~2.2x EoY’23 figures and nearly 3x my projections.

The issue at the moment is that it’s just not enough to really turn the business around this year or even in 2025. Is it necessary? Yes, but the pain isn’t over for those betting on the pivot.

Parting Thoughts

This would have been one of the best shorts I’ve made so far but unfortunately, I covered too early mainly out of fear of getting squeezed out like I did in Q1’23 with other names.

Despite this, had I held on to this name through earnings, I would have covered once the market opened. The lemon has been squeezed and if there’s more downside, it’s not worth the risk.

On the flip side, I understand that many want to believe in this turnaround. I don’t blame you. The drug works and the demand speaks for itself. While this might potentially be true, we don’t know to what degree the core business of WW will degrade until the clinical side starts really picking up the slack.

Looking at the current financial state, which don’t forget, another $16 million payment as part of the Sequence deal will be handed over to Sequence management on the 1st anniversary of closing (right around the corner), the turnaround doesn’t look great.

Thinking for yourself and analyzing other risks/rewards in the market, there is no question that there are better opportunities at the moment. This isn’t the hill to die on in the name of generating alpha. To be frank, I’m not sure what LONG alpha you’re going to be generating from this company any time soon unless it’s earnings-driven.

Otherwise, the beta is not worth it. This is me speaking from my perspective on how I would handle it but to each their own. I’ll keep watching from the sidelines but for now, the chapter for CGC is closed on WW.

If you liked today’s post or the original notes, please consider sharing them. If you’d like to send me a private message with a question, do so below. I enjoy sharing notes and ideas with others to see what we could be missing.

Until next time,

Paul Cerro | Cedar Grove Capital

Personal Twitter: @paulcerro

Fund Twitter: @cedargrovecm