Note: All information and commentary are as of June 30, 2022 except for M&A commentary on KSS and research posted for 1847 Goedeker.

*Correction: A previous version said our Q2’22 performance was -31.2%.

Fund Performance

In Q2 2022, Cedar Grove Capital Management, LLC (“Cedar Grove Capital” or the Fund” or “CGC”) returned -35.8% gross return compared to -16.4% for the S&P 500, -25.7% for the S&P Consumer Discretionary ETF XLY, -59.6% for the Cannabis ETF, and -23.9% for the Russell 2000.

Market Commentary

The first half of this year has definitely been one for the books. The only sector of the S&P 500 that was in the green was energy having been blessed with the Ukrainian war and the cartel’s hesitancy to pump out additional supply to meet the energy demands of the world.

The worst sector happens to be the one that CGC operates in, consumer discretionary. The market was quick to dump anything in that sector with complete disregard for how well the companies were doing in some instances, but not all. Multiple compression was the name of the game in the first half with earnings revisions coming down in certain areas of the sector in the second quarter.

Much of the collapse in retail names has come from margin compression brought on by consumers changing spending from goods to services, but not entirely. Companies that deal in hard goods, such as electronics, furniture, and apparel all did not anticipate the eventual shift once the world started reopening. The misinterpretation of consumer demands led to inventory build-ups which directly translated to missed earnings.

The change came about suddenly, which left a number of retailers with excess inventory in Q1, including mass merchants Walmart and Target, big-box electronics seller Best Buy, furniture chain Kirkland’s, apparel retailers The Gap and Urban Outfitters, and discount merchants Big Lots and Burlington.

What’s worse is that these inventory build-ups now need to be moved quickly to make room for the new inventory coming in, resulting in expected discounts which only prolongs earnings degradation.

Time will tell just how well retailers can weather the storm and if consumer trends from hard goods to services continue or slow down entirely.

Making matters worse, The University of Michigan’s gauge of consumer sentiment reached a final reading of 50 in June. That was the lowest reading on record going back to 1952, and down from both an initial reading earlier in the month and May’s 58.4 reading.

The Michigan survey showed about 79% of consumers surveyed expressed pessimism about future business conditions, the highest level since 2009, and 47% blamed inflation for “eroding their living standards.”

A souring mood for consumers, who face the highest rate of inflation in four decades, is a concerning sign because household spending accounts for about 70% of U.S. economic output. Retail sales fell in May, the first decline this year, and job and wage growth also slowed in May. Economists surveyed by The Wall Street Journal have raised the probability of recession.

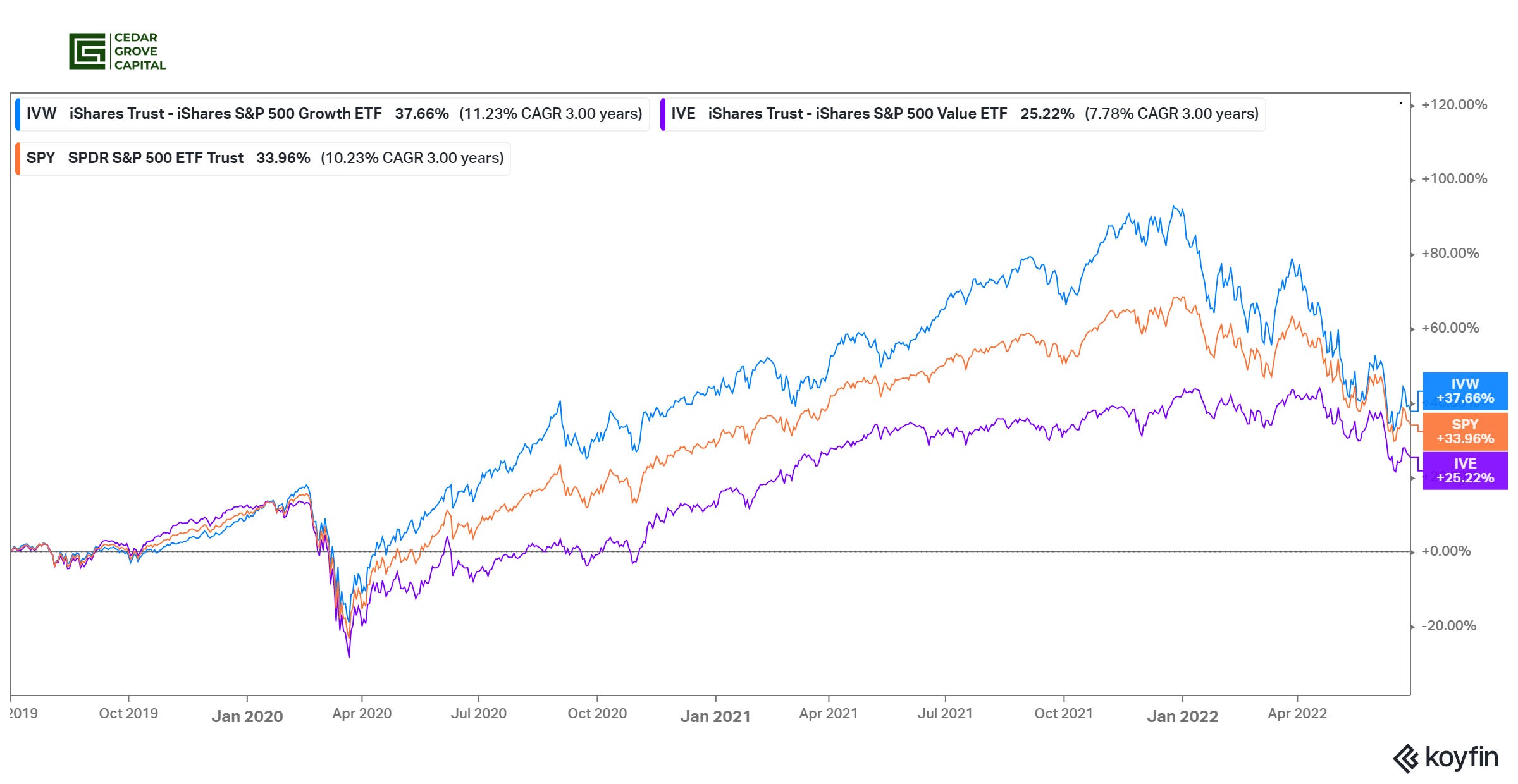

With so much pessimism in the market, the switch from growth to value is quite noticeable.

Performance spreads over the last three years have contracted dramatically to just ~1200bps as of June 30th. An emphasis on earnings and cash flow seems to be taking shape though there is still plenty of money out there chasing tech-related dreams.

We’ll see how well 2H’22 turns out when QT gains more steam and the FED continues to raise rates to combat inflation.

Current Portfolio

Select Investment Commentary

The second quarter was all about trading and trying to monetize on spikes in volatility and worsening economic conditions. I won’t go into all the trades but rather core positions instead. Mind you, given the onslaught that occurred in Q2, many positions selling had overlapping reasons that may have not been company-specific.

Sells

Agrify AGFY 0.00%↑

Agrify was a hard position to sell, mainly because I did not want to admit I was wrong given the 200% run-up I had last year on it. However, anything cannabis has been destroyed this year and that includes the ancillary players like Agrify. I decided to sell out, take the loss and move on. While top line is still growing at triple digits, their ability to reach profitability is questionable and management’s poor response to the short report from December should have been my deciding warning side.

Bark BARK 0.00%↑

Bark Box was another tough sell. While I called the pet trade very well going LONG Petco and SHORT Chewy, I got it wrong with Bark Box. I was initially impressed with their growth rates which were close to the original SPAC presentation but the company was failing to reach even positive adjusted EBITDA and the future looked bleak in ever achieving it. That being said, I consolidated my pet positions to just Petco.

Restoration Hardware RH 0.00%↑

The original thesis of wealthy spending did not hold up as planned. Consumer spending not only rapidly deteriorated but most spending left turned to services than physical goods that did not feed into service-oriented “experiences.” After two downward revisions and a very favorable share buyback, I decided to sell. While I do like the company, it is highly cyclical, and the wealthy are not repeating the way they have spent in prior downturns. When the dust settles, I will revisit the name but for now, it will remain on my watchlist.

Green Thumb Industries

As mentioned previously, cannabis has been wrecked this year for no other reason than delays and empty promises from the government. While I am a big fan of Green Thumb, I was not willing to ride that train down any further. Once more meaningful moves come down from politicians I’ll hop back in but for now, I’ll watch from the sidelines.

Coinbase COIN 0.00%↑

While we were initially right on our LONG call for COIN, we didn’t take the near 50% gains when it peaked in November. My assumption that volatile prices in crypto would be good for trading fees was wrong. Too much HODLing and rushes to liquidate holdings left many one-time fees and not the increase in trading I was expecting. This reduced the number of fees Coinbase generated and with a .98 correlation between the stock price movements of COIN and BTC, an extreme drop occurred. We exited at a loss but not nearly the next near 50% drop we would have experienced had we held on.

Scott’s Miracle-Gro (SMG)

Scott’s Miracle-Gro was a cannabis ancillary play through their hydroponics arm, Hawthorne. Last year, we believed that SMG’s core consumer business was worth the price that it was trading at (~$146) and you’d be getting Hawthrone for free. While once again we did predict this accurately, the November peak, related lack of cannabis regulation, and slow down in consumer spending for lawncare caused an earnings decline. We decided to sell and sit it out until a rebound.

Domino’s DPZ 0.00%↑

We were originally LONG Domino’s and published our research here. DPZ is having issues not just on the inflationary front of input costs but mainly from labor and its ability to hire for the delivery side of its business. This labor issue is causing some dents in SSS as franchisees which translated into a soft 1H. We still like Domino’s but opted to sell it to take a position in RCI Holdings as we felt the upside was more attractive and gave a better IRR for our liking.

Fiverr International FVRR 0.00%↑

Fiverr is another high-profile tech name that came crashing down. Same story as COIN as far as being right but not taking gains. Looking back, the multiple was high but we believed that the company would benefit from more gig work not only from consumers trying to make more money but also from companies looking to hire without offering full-time packages. This proved right to some extent but could not hold up against the onslaught of the tech sell-off. We sold out to preserve capital but would revisit the name should the valuation become more attractive.

O’Reilly Automotive (ORLY)

ORLY was a name that we felt could hold up given the long-term tailwind of used cars and how long consumers are holding onto them. However, we felt the valuation was getting extended and decided to forgo holding onto the name.

Evoqua Technologies (AQUA)

AQUA was a company that we were excited about because of its expertise in water purification on the west coast. However, the name did not hold up in the volatility of the first half despite aligning more with a utility. We sold the stock to focus more on our core competencies in the C&R space.

Innovative Industrial Properties IIPR 0.00%↑

We took a position in IIPR for the purposes of owning the real estate under the cannabis companies as we believed that that area of the industry would be better insulated from dramatic price moves. We started this position at the end of Q1 and the next day a short report came out by Blue Orca calling for their biggest tenant to become distressed. The stock sold off and we sold out with it. The stock has dropped an additional 50% since we sold it.

e.l.f. Beauty (ELF)

Nothing special here. We figured if vanity was getting destroyed then we were in a worse economic position than we thought. The quick rebound in the name clearly proved us wrong but by then, the stock became too expensive to get back in.

Williams Sonoma WSM 0.00%↑

WSM was one that we felt was misunderstood by the market. The name was hammered by pessimistic market expectations but the underlying fundamentals and trends were very supportive. The stock rebounded nearly 30% from the bottom where we bought it on the second go around after reporting better than expected results. We decided to once again cut our exposure to highly cyclical spending names like WSM.

Warby Parker WRBY 0.00%↑

I personally wear Warby Parker glasses but the stock was too rich. DTC model was not proving itself and retail foot traffic was slowing down considerably. National Vision’s slumping sales sent WRBY down with it and investors seemed to be losing faith. Our thesis proved right which led us to recognize a 19% ROI on the position and a near 4% gain for the overall fund in just this name alone.

Buys

Altria MO 0.00%↑

In an effort to capture income during all this volatility, we took a position in Altria as a dividend play. Staples have held up well this year and some have even had some significant gains YTD. Simple thesis, people just aren’t going to quit smoking. While growth is minimal and world governments fight back against smoking, handsome dividends still get paid out.

RCI Hospitality RICK 0.00%↑

While we haven’t published our research yet on RICK, we are very bullish on the name. We believe that the market is undervaluing the company on many fronts. Discounting not only the equity value of its real estate but not assigning a multiple on the Bombshells business that would be in line with other restaurant companies. Given that the main business of RICK is gentleman’s clubs, the market is unfairly punishing the company. With that being said, we felt that our capital would be better applied here, with RICK, and achieve a more desirable IRR and overall return.

If you’re interested in getting our research for this name when it comes out, hit the button below.

Kohl’s KSS 0.00%↑

Kohl’s is another name that we decided to take an arbitrage position in. A buyout offer came from FRG at $60 a share and in the following weeks, the rumors of financings were coming through and it seemed that Kohl’s was going to be taken private. While we were confident that the company would be taken private at or around the offer price, KSS board eventually turned it down (after June 30) and the deal fell apart.

This position will be updated in the following quarter but is marked as a buy during Q2.

Twitter TWTR 0.00%↑

Twitter we purchased for the sole purpose of arbitrage on the deal from Elon to buy the company. While much doubt was cast in the last two months, we believed that the merger agreement was air-tight to Twitter being in the right. We outlined our thesis here and shortly after, Twitter sued Elon Musk to make good on his deal. We too believe that Elon will be forced to make good on the original agreement at the original price agreed upon.

Urban-Gro UGRO 0.00%↑

With cannabis going into freefall this year, we revisited a name that we have written about last year (can view here) and held but sold out of in Q1. This company is an ancillary player in the cannabis and CEA space and with its stock price down so much and the fundamentals largely staying the same, we took a position in the company again. We believe that this stock should be trading close to its historical mean since it is a nanocap, of around ~$10 a share.

In our opinion, it is one of the safer ancillary names in the CEA space. A space that consists of Agrify (AGFY), Hydrofarm (HYFM), and GrowGeneration (GRWG).

1847 Goedeker Inc. (POL)

I actually came across this opportunity from David over at Kingdom Capital Advisors. He outlined his updated thesis here but got me into the name back in April via warrants on the stock.

Key points for the trade are outlined below pulled directly from his research.

From a multiple and growth perspective, it’s quite cheap and that’s mainly driven by the fear in the market for anything consumer related.

With a $1.20 share price (~$130m market cap) and $30m of net debt, the business is valued at less than 10x EV/TTM EPS and 5x EV/TTM EBITDA. If the company hits their FY22 growth and margin guidance, they will earn ~$650m revenue and ~$60m EBITDA, which would be 2.7x EV/EBITDA at today's share price.

Appliances have historically held up better than other furnishings retailers in similar downturns.

Spending on appliances pulled back 10% in 2009 - less than half as much as broader durable goods spending.

Margin expansion is something to consider heavily after the company received a $140M loan from BofA.

I expect future margin pressure from reduced pricing power to be offset by vendor rebates, increased ad spending to be offset by better fill rates (and better scale economics), and possible margin improvement from building out a better distribution network. Even with current margins, I own a business trading under 3x EV/EBITDA on this year's forecast, on which Bank of America underwrote a $140m loan.

First time buying warrants for a company but we’ve discussed the math and his research seems to be a sound strategy. Warrants at the levels we purchased them at would yield the better of the two (stock vs warrants) in terms of an ROI perspective.

Closing Remarks

Trading has never been my strong suit and it clearly shows. I deviated from what I excel at which is deep analysis both on the LONG and SHORT side. With that being said, going forward, CGC will be going back to our roots of what made us great in the first place and avoid trades.

Additionally, while diversification helps portfolio’s on the downside, it’s not as lucrative on the upswings. Given the precipitous drop in the market and consumer discretionary specifically, we will focus on a more concentrated portfolio rather than the traditional 12-15 positions we’ve held in the past.

We’re eager to realign accordingly and find the next opportunities coming out of whatever market this will go down in the history books as.

I also apologize for the lack of posts as of late but the fund has been elbows deep in private investment opportunities. While this has taken up a lot of our time, we’ll be sure to continue adding value to the newsletter when we can.

Until next time,

Paul Cerro | Cedar Grove Capital

Personal Twitter: @paulcerro

Fund Twitter: @cedargrovecm

Share this post