Q1'24 CGC Quarterly Letter

Frontrunning, expectation resets and calibration/consolidation

Fund Performance

In Q1 2024, Cedar Grove Capital Management, LLC (“Cedar Grove Capital” or the Fund” or “CGC”) returned 8.3% gross return compared to 10.4% for the S&P 500, 3.1% for the S&P Consumer Discretionary ETF XLY, 42.1% for the Cannabis ETF, and 4.9% for the Russell 2000.

Q1 Market Commentary

To sum up Q1 → there’s too much money sloshing around.

The hopium and frontrunning on multiple fronts are clear and apparent despite the underlying moves in those mindsets not actually materializing yet.

FED cutting rates 6x. Then it became 4x…then 3x…and now we’re entertaining the idea that there might not be any rate cuts this year. Depending on who you ask, that may or may not be a bad thing.

On the other side, we have the inflation bulls declaring victory and bears pointing to a possible resurgence in inflation. Both are problems when it comes to rate expectations.

AI taking the front-row seat even though most companies that have mentioned incorporating AI into their business don’t even quite understand how to use it in the first place. It’s nice to through the buzzword around to drum up excitement in your stock but aside from chat bots, there’s not much to show for it. Not to mention that there will come a time when the amount of capital that’s being invested will taper off and thus the parabolic growth that we’re seeing in semi-names.

Lastly, I would be remiss if I didn’t mention the absolute stupidity that’s going on in crypto prices and general euphoric conditions.

With so many coins that quite literally have no value, it looks like retail investors have gone to the casino again. As pictued above, retail net purchases of leveraged ETFs (TQQQ & SOXL) have greatly taken the market by storm since the beginning of March. This is no mere coincidence. Shall we mention DJT?

The absolute stupidty of the current sentiment is the casino spreading to Trumps spac that generated only $4.1 million in sales for FY’23 yet lost $58 million dollars doing so. Borrow to short the stock has ranged from 750% to 900%. With this being just one example of hundreds, it’s hard not to want to see the market correct itself and flush out this absurdity.

On top of the meme rally, this 10% upward move in the S&P once again is frontrunning FED cut expectations that keep getting dialed back with the market only recently starting to feel wobbly as of the Q2’24 start.

I’m expecting more of the same but while I’m not trying to be bearish, it does have me thinking about what would be the liquidity event that could trigger things?

Housing? CRE? Unemployment? NATO confrontation?

It doesn’t have to be big at the onset. Hell, the Great Fire of London started in a bakery…

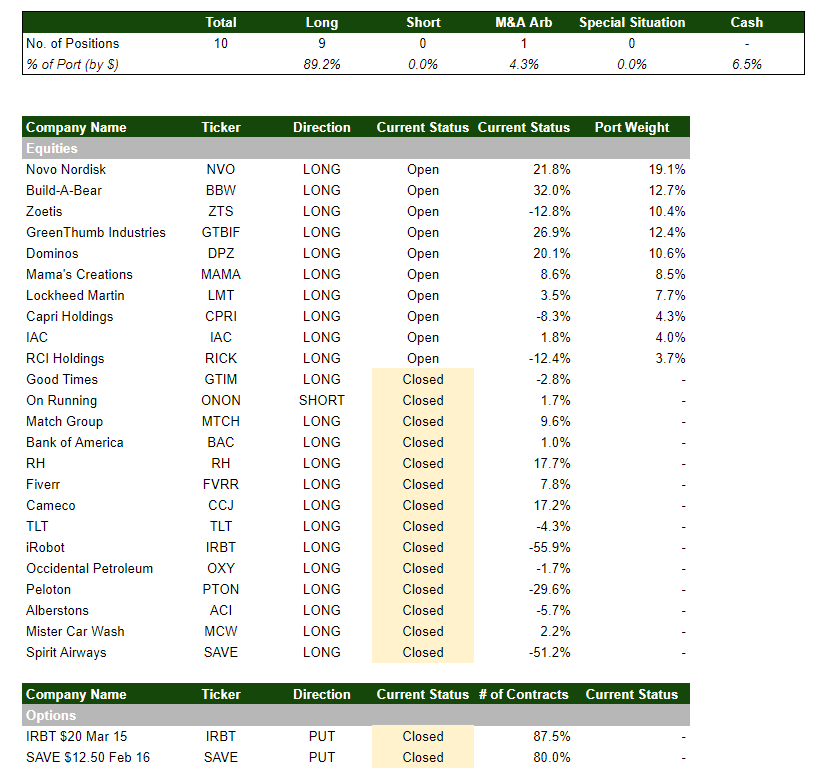

Positions Quarter-End

As I mentioned in my last letter, I was planning on consolidating positions greatly at the start of the year. 2023 I nearly doubled the usual number of positions I have in an effort to diversify the portfolio as a hedge for too many unknowns that happened last year.

In Q1, I exited 14 positions to bring the current count down to just 11. Over time, that number might be cut down by a fourth in an effort to concentrate on core positions with a return to an “ownership” strategy in LONG positions.

This return to “ownership” meant ending positions in energy (OXY & CCJ), certain technology names (MTCH & FVRR), and the ending of banks and shorts (BAC & ONON).

Notable Position Commentary

RH (RH) - Sell

RH was a tough one to sell. I’ve been bullish on the name for years and stuck by Gary ever since the collapse in price starting in 2022. I was a firm believer in the turnaround story and highlighted it in a past post calling for an inflection in the investor base.

While the massive buyback in shares was encouraging, I believe that capital allocation was really the only thing keeping the stock from collapsing even further. That and no clear sign of a return to growth led me to decide to exit the name. This stock very well could turn around in the next few years but I believe in the interim, there are better risk/reward opportunities out there.

Match Group (MTCH) - Sell

I was hopeful for for MTCH to accelerate growth and continue to produce sizeable FCF, however, with the announcement of the $500 plan I already felt uncomfortable. The short of the story is that I did not feel confident anymore in management’s ability to continue at the clip that it had and there was a clear underlying maturity curve in a number of the core brands.

Thankfully, Elliot Management stepped in with activism and allowed me to exit the position at a small gain. I think the company is going to continue facing challenges as the market for online dating matures and continues to saturate.

Peloton (PTON) - Sell

If you’ve followed me long enough, you definitely know how I’ve felt about Peloton over the years; bearish. That play has worked out and only recently did I flip LONG not because I believed in the company but rather because I made the argument that the company should not stay as a standalone company.

While I was hopeful that a potential deal could arise from several suitors — mainly either Apple (AAPL) or Lululemon (LULU) — no real hint came about. Considering this was merely a special situation trade, no materialization over the last few months made it easy for me to exit the name and redeploy capital elsewhere. Perhaps they will get acquired in the future but in the meantime, there are better opportunities out there.

Various Arb Deals - Sell

There’s quite a graveyard of investors who went long both the iRobot (IRBT) and Spirit Airways (SAVE) deals. I shared my follow-up thoughts recently in a post that also included a brief update on the Albertson’s (ACI) deal which I said would not happen (and it hasn’t) as well as the Capri Holdings (CPRI) deal.

Painful trades, but such is the risk when dealing with arbitrage. There’s currently only one arb trade on right now for Capri Holdings (CPRI) and Tapestry (TPR). You can read the update below.

If it weren’t for the two failed deals, my returns would have beaten the S&P by ~200bps. C’est la vie.

Closing Portfolio Remarks

Q1 has been an interesting one, to say the least. As I mentioned in my Q4 letter, most of that rally was attributed to rates that spilled into Q1. The CRE space is one to keep an eye on and I’m still expecting more pain to come in this industry though I will caveat it with the fact that there are tens of billions of dry powder from PE firms waiting to pick at the bones once bankruptcies and firesales start.

I’m excited to return to my core investing mindset of holding a few core positions with an ownership mindset. I’ll still be holding asymmetric trades in arb, SS, and event-driven names as they present themselves.

Looking forward to what Q2 has in store.

Until next time,

Paul Cerro | Cedar Grove Capital

Personal Twitter: @paulcerro

Fund Twitter: @cedargrovecm

Have you looked at Talgo SA (TLGO)? There is a bid from an Hungarian peer that is not really appreciated. Management is no shopping for an alternative (hopefully higher) bid. At current price it looks asymetric to me.