TOC

Deal Specifics

Activision Context

Deal Price Action

What We Know

Odds of the Deal

Trade Strategy

Important Factors

1) Deal Specifics

Earlier this year in January, Microsoft MSFT 0.00%↑ announced it will acquire Activision Blizzard ATVI 0.00%↑ for $95.00 per share (a 45% premium to its previous closing price), in an all-cash transaction valued at $68.7 billion, inclusive of Activision Blizzard’s net cash.

"With Activision Blizzard's nearly 400 million monthly active players in 190 countries and three billion-dollar franchises, this acquisition will make Game Pass one of the most compelling and diverse lineups of gaming content in the industry" - Microsoft

Microsoft also boasted Game Pass has surpassed 25 million users. With each user paying $16 a month, that’s about $400 million in monthly revenue.

With Activision Blizzard, Microsoft now owns a huge new range of franchises it can make available through Game Pass, attracting even more users.

2) Quick Activision Background

Activision’s gaming portfolio includes iconic franchises like Warcraft, Diablo, Overwatch, Call of Duty, and Candy Crush, in addition to global eSports activities through Major League Gaming.

In 2021 alone, Activision’s top three franchises—Call of Duty, Candy Crush, and Warcraft—collectively accounted for 82% of net revenues (~$7.2B). No other franchise comprised 10% or more of its net revenues.

3) Deal Price Action

Though the buyout offer came in at $95/share, the price only rose ~26% to ~$82 a share after the news still leaving plenty of upside on the table.

Since then, however, the price has come down ~4% from its post-deal announcement close of ~$82 to ~$79/share. At this level, there technically is an upside of ~20% left in the stock, but what’s holding the market back?

First, we need to weigh what exactly is going on before we access the arbitrage opportunity.

4) What We Know

Antitrust concerns

The review of Microsoft's deal will be up to the Federal Trade Commission and not the Justice Dept., which is a discouraging sign for the deal's prospects. That's because the FTC under Lina Khan - previously a vocal critic of big tech - has acknowledged taking an aggressive stance against dealmaking.

In recent years the FTC and DOJ have come to agreements about dividing responsibilities to review antitrust concerns over major deals. And the FTC has sued to block two big ones so far: Nvidia's deal to buy Arm and Lockheed Martin's proposed purchase of Aerojet Rocketdyne Holdings.

Microsoft has largely escaped the recent rush to clamp down on tech giants like Amazon, Alphabet, and Meta — until now. The company argues that, even after buying Activision, it would still be far smaller in video games than Sony or Tencent. And in a sign of its confidence in the deal, Microsoft will pay Activision up to $3 billion in breakup fees if regulators block the transaction. No small sum.

Microsoft expects the deal to take up to 18 months to close but the Biden administration has been steadily increasing its antitrust enforcement efforts, with a focus on the tech industry.

Four senators have expressed its concerns of this specific deal as well. Sens. Elizabeth Warren, Bernie Sanders, Cory Booker and Sheldon Whitehouse said, "We are deeply concerned about consolidation in the tech industry and its impact on workers" in a letter to FTC Chairwoman Lina Khan.

The senators want the FTC review to assess whether the deal could exacerbate the allegations of sexual abuse, harassment, and retaliation that have become prevalent as Activision faces federal and state probes over misconduct.

FTC Chair Lina Khan, though - now likely with enough support from aligned commissioners - will examine the deal with an eye to the combined companies' access to consumer data, the game developer labor market, and the deal's impact on those workers who have accused Activision of discrimination and a hostile workplace, according to The Information. And the FTC is also looking into the potential impact on a competitive metaverse. The probe is still in its early stages and expectations are that barring an FTC suit, Microsoft can close the deal soonest sometime in 2023.

What MSFT is Doing

In an effort to gain good regulatory standing for the deal, Microsoft announced a new set of Open App Store Principles that will work on the Microsoft Store on Windows and the next version of marketplaces the company has for games.

In a blog post, Microsoft's President and Vice-Chair Brad Smith said the principles were developed

"in part to address Microsoft's growing role and responsibility as we start the process of seeking regulatory approval in capitals around the world for our acquisition of Activision Blizzard."

In addition, Microsoft said it intends to keep "Call of Duty" and "other popular" Activision Blizzard titles on Sony PlayStation beyond existing agreements and said it was interested in "taking similar steps to support Nintendo’s successful platform."

As part of the new principles, Microsoft said all developers would have access to its app store "as long as they meet reasonable and transparent standards for quality and safety."

In addition, Satya Nadella-led Microsoft said it would not require developers to use its payment system to process in-app payments, in stark contrast to what Apple has done with its own app store.

Microsoft also explained that it would not prevent developers from communicating directly with customers via their apps for what it coined "legitimate business purposes, such as pricing terms and product or service offerings."

Quick Recap

Concerns against deal

Too much consolidation in the gaming industry

MSFT to make ATVI portfolio exclusive to Xbox

Company culture - sexual abuse, harassment, and retaliation

Responses to Concerns

Will allow titles to be played on other consoles

Will not restrict developers to only use payments on Xbox

Will not restrict communications between developers and customers

As for harassment concerns, it seems more like an Activision thing and not so much a Microsoft thing.

5) Odds of the Deal

So I actually asked Twitter if it thought the deal was going to close or not and the results suggested, at least on Fintwit, that it expected it to close.

While I was hoping that some would give their reasoning as to why or why not, I only received one reply which has a point but not really further than that.

Given where the current price is (a ~20% jump since the announcement) and what’s left on the table (~20%), it seems that the market is predicting a ~46% chance of the deal closing. This was from a high of 60% immediately after the deal was announced.

To figure out the implied odds of the deal getting done, arbitrageurs take the stock gain of $13.64 (current price from the price pre-announcement) and divide that into the total potential advance of $29.61 a share measured from the January 14 close if the deal gets completed.

But why the skepticism?

As Microsoft pointed out in announcing the deal, the transaction will make it the world’s third-largest player in gaming by revenue, trailing only Tencent Holdings and Sony—and the largest U.S.-based player.

Microsoft's gaming business generated $15 billion in revenue in fiscal 2021, while Activision generated $9 billion. The addition of ATVI would mean Microsoft will control 14% of the $200 billion+ gaming industry. Not a crazy amount if you ask me.

Even with the sheer size of what they would then control, they’ve made public statements (above) about them not restricting content to just Xbox, making developers use their payments system and or being able to communicate to consumers. These were all red flags that were initially raised for deal review after the announcement was made.

Additionally, a $3 billion breakup fee is not a small sum (>4% of TV) considering most breakup fees range from 1-3% of the total transaction value. I don’t think Microsoft leadership would wager so much on a fee if they didn’t believe the deal would close.

For all these reasons, I am actually bullish on this deal actually happening and believe that the company has taken the necessary steps to win points with Lina Khan.

With this being said, let’s take a look at how I’m thinking of playing this.

6) Trade Strategy

While traditional M&A arbitrage would entail going long one name and short the other, considering Microsoft’s size and how it only went down -2.43% after the announcement, it would take a large position to offset any losses.

Because of this, I’m actually looking to go LONG ATVI via CALL contracts while simultaneously going SHORT via PUT contracts. There is also another component of selling OTM CALL options at higher than deal value to generate some income while lowering my LONG CALL option premium.

Below I’ve included two tables that show where CALL/PUT options are trading for ATVI as of close 4.19.22. Nothing to really look at because I’m just using this as a reference point for anyone reading this.

Scroll past them to get to the math.

So like I said above, this is a three-part trade. We already know that Microsoft said the deal would close in FY’23 (end of June, 2023) so we have a rough sense of time. Realistic option dates only extend to March of 2023 so that’s what I’m using for this exercise.

Considering that I’m looking so far in advance, this is all theoretical and does not mean that I’m executing at this price.

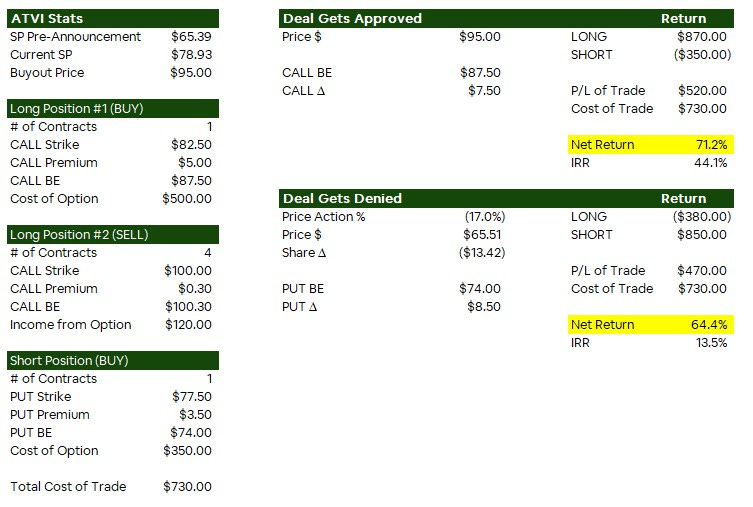

So the way I structured this trade (and for easy numbers) was buying 1 CALL option at $82.50 strike with a $5 premium bringing my breakeven (“BE”) to $87.50. Then, I would buy a PUT option at a $77.50 strike and a $3.50 premium to bring my BE to $74.00 as part of this hedge. Lastly, I would then sell CALL options at the $100 strike with a $.30 premium, over a few months as time went on to lower my overall cost.

Factors that this trade does not include:

Volatility

Time

Interest rates

If SHORT CALLs get executed

1) Deal gets approved

If the deal gets approved at the $95 value, my PUT contracts become worthless but I can recognize the full intrinsic value of the option ($7.50) plus all the premium I made selling the $100 CALL options (should they not get executed).

This brings my P/L of the trade to $520 in the black. Given that my cost of the trade (excluding if my SHORT CALLs get executed) is $730 bringing my total return to 71.2% and if I factor in a March 2023 time, an IRR of 44.1%.

2) Deal gets denied

If the deal gets denied, I believe that the stock price will quickly retrace back to where it was trading before the announcement if not more ($65.50). Because of this price drop, my LONG CALL contracts become worthless but I can still keep the premiums I made on the SHORT CALL contracts. Additionally, the now ITM PUT contracts I believe would be worth $8.50 in intrinsic value.

This brings my P/L of the trade to $470 in the black. Given that my cost of the trade (excluding if my SHORT CALLs get executed) is $730 bringing my total return to 64.4% and if I factor in a March 2023 time, an IRR of 13.5%.

Again, realize that there are factors that these trades do not account for (above) that could greatly affect the returns both for or against me.

7) Important Factors

There are two important factors that might not deter me from executing this trade, but they will provide some light on the matter before I decide to do so.

One of these factors deals with the Oracle of Omaha, Warren Buffett. Warren Buffett's Berkshire Hathaway (BRK.A, BRK.B) purchased a nearly $1B stake in Activision during Q4 as shares were beaten down from the "frat-boy culture" lawsuit filed by the California Department of Fair Employment and Housing. The stock fell to as low as $56 before Microsoft announced its intent in mid-January to acquire the game developer for $95 per share.

At Activision's closing share price of $79.06 on Monday, Berkshire's stake would be worth almost $1.1B - a solid profit, but who knows if the conglomerate is still holding the position? Considering Warren likes to do M&A arbitrage trades only after a deal is announced, I’m going to be paying very close attention to his quarterly letter due soon to see if he is indeed riding out the buyout offer.

The other factor deals with SOC Investment Group who in a written letter advocated for shareholders to vote no for the deal saying

“This transaction fails to properly value Activision and its future earnings potential, in significant part because it ignores the role that the sexual harassment crisis—and the Activision board’s incompetent handling of it—has played in delaying product releases and depressing the share price”

It also said it’s

“skeptical that any transaction with Microsoft (or a similar acquirer) would be viable, given the shift in the climate of anti-trust enforcement, as well as evident sources of potential harms to competition stemming from the merger”.

The vote is due April 28th so we’ll see if a) they vote no which leads to an obvious no on the deal, or b) they still vote yes and then the only thing stopping them is the FTC.

Both of these factors are what I will be watching out for in the coming weeks.

Until next time,

Cedar Grove Capital