Trading Strategy Beat the S&P, QQQ, & DIA in 2022

How an embarrassingly simple trading strategy beat the S&P by 14 percentage points in 2022

If you like today’s post, please like and share. If you’re interested in premium content, be sure to subscribe to our paid newsletter.

If you need a reminder of what you get by going paid, click this link and you’ll also find a promotion at the end of this post.

Finding An “Edge”

In today’s world of investing and trading, everyone is looking for an edge. This “edge” can come from many different sources that allow the beholder to increase their odds of being correct such as

Quantitative models using statistical analysis (quant funds)

Inside information (illegal)

Hiring industry experts and consultants

Paying for proprietary data (credit card data, black box data, etc)

And many more

However, while many will spend an obscene amount of money in order to generate a profit for their PnL, I was curious if there was some type of trading strategy that could beat out other funds while utilizing the least amount of resources possible.

This is where I decided to look into a ridiculously simple strategy that I felt might be too good to be true.

While I’ll talk about 3 comparisons for the SPY 0.00%↑, QQQ 0.00%↑, and DIA 0.00%↑, it’s important to know what I was testing against and why I did it this way.

So with that, let’s take a look.

The Premise

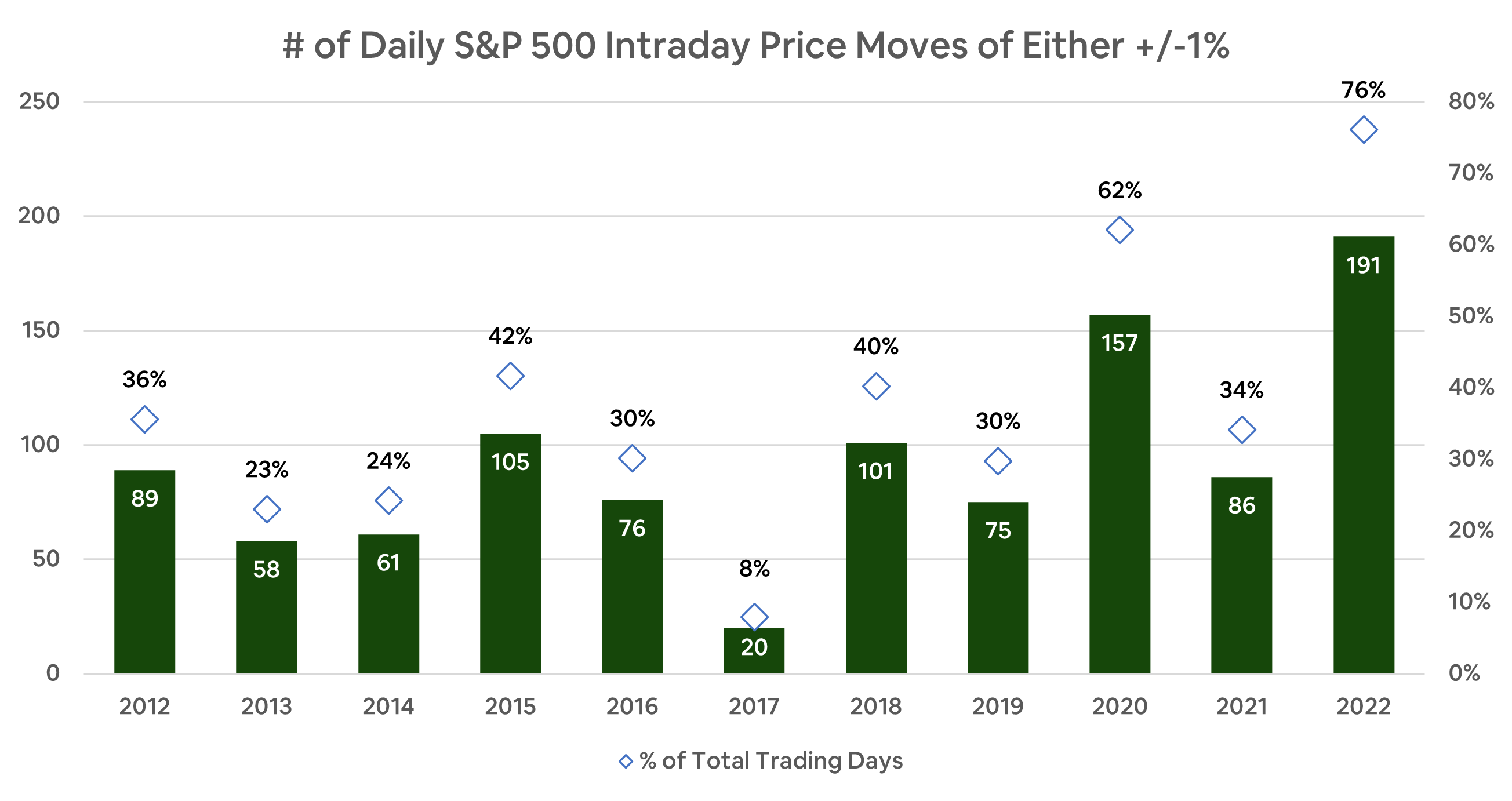

For very quick context, intraday volatility has exploded in recent years which can be seen in the chart below.

If you’d like to read a few more facts on the above chart, you can click the link below to continue on.

Anyways, with so much volatility happening during the day I wanted to examine 2 different strategies that carried different risks against my “control” case.

Control: The ETF that I’m comparing to and how its return was as if I bought and never sold

Test #1: Buying at the market open, and selling at the close every day incurring intraday market risk but eliminating overnight risk

Test #2: Buying at the close, and selling at the open every day incurring overnight risk but eliminating intraday risk

Fairly simple strategy right? I think so.

So the way all this was calculated was based on taking an initial $10,000 and buying and selling shares to the max whole share count allowed on a daily basis and rolling over cash until we could buy the next whole share.

What you’ll be shocked to see is just how well these strategies worked last year against the SPY, QQQ, and DIA.

SPY Results

If look at the SPY, the results are absolutely wild.

If you held onto the SPY at the beginning of the year and didn’t sell, you’d be down almost 20%, however, if you used the buy at the open / sell at the close trading strategy, you’d only be down a whopping 5.3% over the same time frame.

Similarly, if you used the buy at close / sell at open strategy, you’d still beat the SPY return but not as much as the former strategy.

Pretty crazy but let’s pivot over to the tech favorite QQQ.

QQQ Results

Compared to the results that we just saw for the SPY, the QQW results are somewhat similar.

If you held onto the QQQ at the beginning of the

year and didn’t sell, you’d be down 33%, however, if you used the buy at the open / sell at the close trading strategy, you’d only be down only 14.5% over the same time frame.

Similarly, if you used the buy at close / sell at open strategy, you’d still beat the QQQ return by ~11.9 percentage points.

Don’t get me wrong, so far you’d be losing money on all these strategies but in some instances, like the SPY, you’d be cutting your losses by nearly 72%.

But now let’s look at the DIA.

DIA Results

This is where the results get a little interesting because they aren’t exactly on par with the other two comparisons we’ve looked at.

Surprisingly, if you held onto the DIA, you would have outperformed the buy at close / sell at open strategy by 2.7 percentage points.

However, if you still used the buy at open / sell at close strategy, you would have not only been positive for the year but beat the control by 12.2 percentage points!

Pretty crazy.

Bottom Line

Using the buy at open / sell at close strategy seems to be the clear winner of all three ETFs that we did this for.

One very major point of all this that isn’t being accounted for is the taxes involved in this strategy. Without diving into the numbers further, I’m not quite sure how many up days we had compared to down days but I can with some level of confidence say this strategy is not tax advantageous.

Nonetheless, I’ll leave you to take this strategy as you will but it was still a great exercise to run.

Additionally, for those of you that don’t know, I do run another newsletter for our private side of the business through

. This newsletter is all about SMB topics in case you're interested.Lastly, if you’re interested in joining our premium community, you can enjoy a free trial below.

Until next time,

Paul Cerro | Cedar Grove Capital

Personal Twitter: @paulcerro

Fund Twitter: @cedargrovecm

HoldCo Twitter: @cedargrovech

be curious to know what the ballpark tax implications would be with this kind of thing. also curious if it generally works most years or just last year.