SMG: Buy two, get one free

Why the market is currently mispricing Scotts Miracle-Gro business segments

Quick note

Since this is an email newsletter, I am capped by how long I make these so in an effort to only focus on the meat of why I wrote this week’s post, I’ve cut down the fluff of walking you through the business in detail.

I’ll only be focusing on my thesis and the supporting evidence to back up my valuation assumptions. If you haven’t read my recent article prefacing this company, please take a look: Oversold is an understatement (quick and informative read). Hope you enjoy it!

Summary

SMG was a big non-tech winner in 2020 taking full advantage of the boom in housing over the last year

Its stock has pulled back so much YTD that it has wiped out all of its 2020 returns and then some

Its hydroponics business, called Hawthorne, is its fasted growing business segment having grown over 50% YoY the last three years

Hawthorne is almost absent from SMGs valuation and you would essentially be getting the company’s value for free at these prices

Aside from getting a business for free, you’re also getting a modest dividend yield and a less volatile company during times of increased market volatility

Business Overview

Scotts Miracle-Gro SMG 0.00%↑ is a manufacturer, marketer, and seller of branded consumer lawn and garden products, as well as indoor and hydroponic growing products.

The Company operates through three segments:

U.S. Consumer - consists of the Company’s consumer lawn and garden business located in the geographic United States

Hawthorne - consists of the Company’s indoor and hydroponic gardening business

Other - consists of the Company’s consumer lawn and garden business in geographies other than the United States and the Company’s product sales to commercial nurseries, greenhouses, and other professional customers.

The Company's consumer lawn and garden brands include Scotts and Turf Builder lawn and grass seed products; Miracle-Gro soil, plant food and insecticide, LiquaFeed plant food, and Osmocote gardening and landscape products; and Ortho, Home Defense and Tomcat branded insect control, and weed control.

Financial Performance

Over the past few years, SMG has been doing quite well. Revenue growth has increased ~31% in 2020 and ~18% in 2019. Considering that the company specializes in the home and garden space, these growth rates are pretty stellar.

The company has been historically net income positive and has been paying out dividends consistently with a dividend yield of ~1.8%.

They also generate significant free cash flow which they then use to pay down debt, issue dividends that I previously mentioned, and authorize share buybacks. The company currently has a $750 million buyback authorization and has allocated $250 million for the coming months.

Also, though this company doesn’t keep much cash on hand, it does have levers to pull as far as dividends paid out, being able to issue new debt and pause share buybacks. Speaking of debt, their leverage ratio has done down over time dropping from ~2.7x in Q1’20 to ~1.0x in the most recent quarter.

Investment Thesis

So Scotts Miracle-Gro is a pretty unsexy and simple business. It sells chemicals and fertilizers under various brands in and outside the US with household names like Miracle-Gro and Roundup. They also operate a hydroponics business called “Hawthorne” that caters mainly to the cannabis industry - this is the business I believe you’d be getting for free.

So what factors play a role in the growth of SMG?

Existing market - People who either already own or just recently purchased a home might want to invest in renovations

New market - New homes being built that will one day need lawn maintenance

Seasonality - people don’t tend to their lawns as much in the wintertime as compared to the spring and summer times

Cannabis - Indoor growing via hydroponics

I’ll be touching on all these points in my thesis after a quick stock drop explanation.

Recent stock decline

When I was first looking at SMG, it was in August and was trading at about $174 a share. Now in mid-October, the stock price has cratered to just $147. This steep decline is brought on by two factors.

After their Q3 earnings, Wall Street was fearful of a Q4 slowdown after posting a huge beat for Q3. The company reiterated FY21 EPS and sales guidance while lowering gross margin expectations and analysts were hesitant that SMG could continue the growth that it had or if they would end up posting a surprising beat.

Broader stock market selloff brought on by events such as Evergrande, debt ceiling deadlines, interest rates, etc.

Though the slowdown in the market might seem warranted at first glance, I believe it’s overblown and the stock is cheap right now, here’s why.

Home renovations during COVID

Back in March of 2020 when everyone thought the world was ending and people were locked in their homes, people ended up spending a lot of money renovating their homes to pass the time.

While the US economy shrank by 3.5% in 2020, spending on home improvements and repairs grew more than 3%, to nearly $420 billion, as households modified living spaces for work, school, and leisure in response to the COVID-19 pandemic1.

Though this encompasses all types of home improvement, a recent survey conducted by OnePoll on behalf of lawn care company TruGreen, the survey found that half of those polled have invested in new plants and garden updates as well as new outdoor seating over the past year2.

Also, 57% of respondents agreed they plan to use their outdoor space even more once the pandemic subsides which signals regular maintenance in order for this to become a reality.

Some forecasts estimate that there will be 9% growth in 2021 followed by 4% growth in 2022. Some issues that might get in the way however are headwinds such as supply chain bottlenecks and availability of labor.

Housing starts

The term housing starts refers to the number of new residential construction projects that begin during any particular month. This includes building permits, housing starts, and housing completions data—all of which are compiled from surveys of homebuilders across the country.

A housing start is counted when construction begins on the footings or foundations of a residential structure. The data is divided into different categories:

Single-family homes

Townhomes and condominiums

Multi-family structures with five units or more such as apartment buildings

In last month’s data, over 1.6M housing starts were recorded. This is almost double what the figures were in April of 2020 when the world went into lockdown and only two-thirds the number of the January 2006 peak before the great recession.

The reason I want to point this out is because of the shift from urban living to suburban living caused by the pandemic. This Black Swan event led to millions of people fleeing their rentals to either live at home until the pandemic subsided, become a nomad via platforms like Airbnb or finally bite the bullet and buy their first home.

With new homes still being built as supply chain issues have subsided from earlier in the year, we’ll continue to see the need for more lawn and garden expenditure going forward.

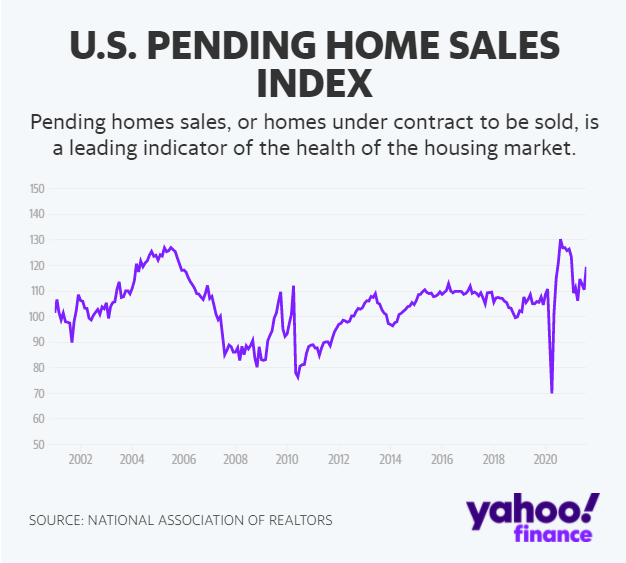

Pending home sales

Another metric that I wanted to highlight is pending home sales. The Pending Home Sales Index (PHS), a leading indicator of housing activity, measures housing contract activity and is based on signed real estate contracts for existing single-family homes, condos, and co-ops.

I treat this economic indicator as one of the key factors that can directly contribute to the lawn and garden market considering new homes could benefit from a revamp once purchased or even to list on the market.

The PHS index rose 8.1% in August to a seven-month high of 119.5 from the previous month. The results outpaced the expected 1.3% increase in sales, according to Bloomberg analysts’ consensus estimates. Contract signings rose in all four regions of the U.S.

The 100 level is based on a 2001 benchmark and is consistent with a healthy market and existing-home sales above the 5 million mark.

The rebound in activity was surprising to some experts who thought rising home prices would deter buyers.

However, some relief in inventory will likely slow down record-breaking home price growth. Total housing inventory, or homes available for sale, at the end of August, totaled 1.29 million units, down 1.5% from July’s supply and down 13.4% from one year ago. Inventory is still tight but the declines are not as severe. By December or January 2022, analysts expect inventory "to turn the corner and increase."

Cannabis market ripping

If you read my recent articles that talked about the cannabis industry (Oversold is an understatement, Why your cannabis stocks aren’t higher) then you will know how much I’ve stressed is not accurately being priced in.

Since 2012, 18 states and Washington, DC, have legalized marijuana for adults over the age of 21. And 37 states have legalized medical marijuana — meaning that a majority of Americans have access to cannabis, whether medically or recreationally.

SMG’s Hawthorne business has seen some pretty impressive growth rates, having jumped to over $1bn in sales in FY’20. This represents growth of over 54% from the prior year and an ~94% increase from 2018 to 2019.

The share of Hawthorne as a percent of total SMG revenue has also increased from 13% in FY’18 to 25% in FY’20.

As more states continue to come online and projected cannabis sales are expected to hit ~$42B in 2026, Hawthorne, the leading hydroponics supplier in the country (leader ahead of Hydrofarm and GrowGeneration) is prime to benefit.

What management says

As millennials embrace homeownership, it’s creating a new generation of SMGs customers, and they’re taking up gardening and lawn care at higher levels than baby boomers, the company says. Another plus is the migration of Americans to the Sun Belt, where the growing season is longer than in the Northeast or Midwest.

On an earnings conference call in August, CEO Jim Hagedorn noted that Scotts “picked up a nearly decade’s worth of growth in a year” in its consumer business during the fiscal year ended in September 2020, as sales grew 24% against an average of 2% annually in the prior 10 years.

The company is projecting sales growth of 7% to 9% for the consumer business in the current fiscal year ending on Sept. 30, but expects a “slight decline” in the coming year, Hagedorn said. Longer-term, the company sees 2% to 4% annual sales growth in the division.

Valuation

So I’m not here to be the overly optimistic one. The point of bringing up all these factors was not to paint the picture that the sun is shining brighter than ever and that unicorns and fairies are abundant and no one realizes it. It’s because there’s still good data coming out and the stock has just dropped too much.

Can anyone say, “buy the dip?”

Here’s a quick recap of what I mentioned above that ties into my valuation.

The overall market might be slowing down, though marginally. Homeowner trends still point to future growth in lawn and garden care and coupled with new housing starts and pending home sales, new homeowners are expected to continue spending.

Management expects leveling off from a fast-paced 2020 with earnings normalizing in 2022.

YTD stock price decline of 27% is too steep for the positive catalysts still at play and there’s more reward than risk at current levels.

With this being said, let’s look at how I valued each part of the business. Historically SMG has been valued as just a chemical and fertilizer business but even in their financial statements, they label companies such as Spectrum Brands and Central Garden & Pet as competitors.

For the sake of this valuation exercise, I wanted to combine companies in both the fertilizer and household products categories and then incorporate the hydroponics business separately, as shown below.

Fiscal year 2021 is already baked in. Management has reiterated guidance on both top and bottom lines so we can already forget about playing with that. This implies revenue at ~$4.8B and EPS at ~9.15. However, I am betting that management is slightly conservative in their estimates in hopes for a beat and worst-case scenario, matching what they guided to.

With this being said, I valued my FY’22 estimates on a slightly inflated FY’21 estimates (sales of ~$4.9B and EPS at $9.37).

For FY’22, I valued SMGs US Consumer business declining by 5% as a broader slowdown in the domestic space but grew its “other” business (outside the US) by 3%.

With Hawthorne, I was aggressive, applying +25% YoY growth rate because I really think analysts don’t understand how many operations are coming online in states at the moment and the need for hydroponics in both cannabis and vertical farming is growing.

Though about half of Hawthorne’s sales come from California right now, I believe that management is aware of how fast this business segment is growing and will continue to fuel to fire and dominate the top spot for market share.

Using my combined US Consumer + Other sales estimates of ~$3.3B and the blended median comps rate of 2.4x, I got $8B in EV just from that one sector. Applying the same logic to SMGs hydroponics business with companies of relative growth rates and garnered $5.3B in EV.

Combining both and working backward, I arrived at a per-share price of ~$195 which represents a +32% upside at these levels.

In case you aren't aware yet, this is rudimentary sum of parts valuation.

With these factors in mind, the per-share basis that I’m valuing SMGs hydroponics business at is ~$56. This means that I’m valuing the other two businesses at ~$138 per share and you’d be getting the hydroponics business basically for free.

I hope you enjoyed reading and please let me know your thoughts on my logic in the comments section below!

Disclaimer: I do currently have a position in Scotts Miracle-Gro (SMG) at the time of this post being published. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from the Substack subscription). I have no business relationship with any company whose stock is mentioned in this article.

https://boston.cbslocal.com/2021/03/29/home-improvement-diy-spending-projects-harvard-study-pandemic/

https://people.com/home/over-50-percent-of-americans-say-they-invested-in-renovating-their-home-and-yard-this-year/