Rumor Has It…

Friday sparked renewed interest in Peloton PTON 0.00%↑ after rumors leaked that Amazon AMZN 0.00%↑ might be interested in acquiring the company. News of this sent the stock up as much as ~38% before settling down to $31.10, a ~26% increase from Friday’s close.

I decided to take to Twitter to share my opinion on the matter which set off a very healthy debate on the cases for and against this deal actually happening.

My Tweet, and sequential thread, garnered >63,000 views and many valid points on both sides of the fence.

In response to the level of interest, I decided to write this post to highlight the Bull and Bear cases of this proposed acquisition rumor and which side I lean on.

What I’ll Cover

The basics of both companies by pointing out high-level facts about each.

The case for Peloton getting acquired.

The case for no chance this deal happens.

Both points one and two will address the qualitative and quantitative parts (where applicable) of each.

What I Won’t Cover

I will not be building out a full-blown model for this discussion or incorporating any merger math here. While I will provide high-level quantitative numbers and figures for each case, that by no means should be taken as a signed-off audit.

I will not be making the cases for other companies potentially buying out Peloton. Strictly Amazon and Peloton.

Disclosure: I/we do not currently have stock, option, or similar derivative position in Amazon (AMZN) or Peloton (PTON) at the time of writing this article.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. This article is not meant to be taken as investment advice and you should do your own due diligence prior to taking any action.

Highlighting The Basics

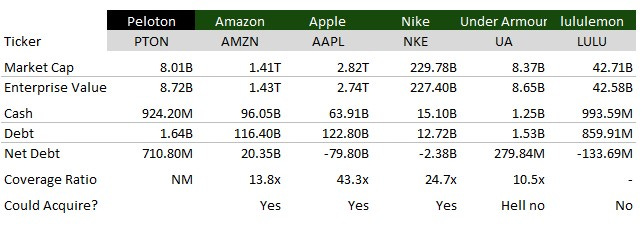

Who’s got the coin?

Amongst the comments that were shared in the Twitter thread, the below companies were on the shortlist for “who could acquire Peloton.” To help us all go into the deep dive portion of this article, I wanted to make sure we had an understanding of the companies basic size and balance sheet in order for this deal to/not happen.

Going to apologize for the formatting between the billions and trillions but this was more of a simple pull from Seeking Alpha for helpful visualization and not something that I created myself.

But let’s dive into some high-level facts and stats about each company that will be used in the arguments later on.

Peloton

Peloton, as you all may know, is a manufacturer of high-end fitness equipment (bike and treadmill) that allows users to either live stream fitness classes or subscribe to their on-demand video library.

If you’d like to read more on the company and how it ended up in the down position that it’s in, I would highly recommend reading Conor Mac’s Peloton and the Kiss(es) of Death article.

But aside from that, let’s dive into a few key things to know about Peloton.

Bike prices:

Bike → $1,495 - $2,035 + $250 delivery fee

Bike+ → $2,495 - $3,035, free delivery

Tread → $2,495 - $3,115 + $350 delivery fee

Subscribers

There are two types of subscribers on the Peloton platform.

Connected Fitness users (live classes) for $39.00/month

Digital-only users (video-on-demand) for $12.99/month

While Connected Fitness subscriptions grew to 2.492 million, digital subscriptions ended the quarter at 887,000. Preliminary earnings say that Connected Fitness subscribers would end at 2.77 million for Q2 of FY’22. Remember this!

User base HHI

62% of Peloton bike users in the US have a household income of between $50,000 and $150,000 so it’s a pretty wide range here.

Customers with a household income of more than $200,000 make up a further 21% of Peloton bike owners. The share of customers in this most affluent bracket has decreased significantly in the past seven years, down from 41% in 2014.

Financials

With the incredible demand for the company’s bikes in 2020, brought on by COVID, the company briefly became profitable and has unfortunately gone back down to hemorrhaging money in 2021 on an adjusted EBITDA basis.

While the CFO estimates that they will return back to adjusted EBITDA positive by FY 2023, that seems pretty skeptical by the way things are going.

Amazon

Prime

Amazon Prime is one of the best successes of Amazon to date. That’s how they book over $25 billion in fees alone from the over 200 million members that have signed up.

Based on eMarketer forecasts, the number of Amazon Prime users in the US is expected to reach 157.4 million by 2022.

Halo Fitness

Amazon’s Halo is its entranceway into the health and wellness space through fitness.

They have the Halo Band, which is basically a Fitbit, that includes access to basic features like steps, heart rate, sleep time, and sleep tracking. Premium membership costs $3.99/mo.

The membership also includes access to a library of hundreds of workouts and programs from partners like Halle Berry’s rē•spin, SWEAT, Orangetheory, and more.

Prime member HHI

The share of online consumers in the United States who are Amazon Prime members as of August 2018, by household income, aligns very well with Peloton demographics. Amazon has 41.6% of those that make $35k - $75k, 55.7% of those that make over $75k, and 58.5% of those that make over $100k.

While the differences between Prime and Peloton classes are big, that doesn’t negate the fact that people who sign up for one are likely to be a part of the other (i.e. Peloton subs are also Prime subs).

Why Amazon Buying Peloton Makes Sense

So there were a few reasons that kept coming up on why people in my Twitter feed were saying that it makes total sense for Amazon to buy Peloton.

Over 3.5 million cult-like subscribers on their platform.

Peloton is a high-quality name brand with best-in-class instructors.

High subscriber retention rate of >90%.

Leader in connected fitness, aka speed to market.

Amazon has a history of M&A into new spaces.

All of these points are valid points. I will not deny that in the slightest. If you’re looking at a company from a high-level point of view and I only gave you these points, you’d be interested as well. So let’s briefly go into each one and talk more about them.

1) Large number of loyal subscribers

So like I mentioned above, Peloton has 2.492 million connected fitness users and 887,000 digitally subscribed users. So, about 3.5 million for easy numbers. Amazon on the other hand has little to show for its Halo brand and if it wants to play catch up in the fitness space, 3.5 million subscribers is not a small number, and Peloton spent years growing its subscription business.

Not only does Peloton have numbers, but they also have instilled a sense of community that some would argue is almost kind of a cult. It’s almost like a status symbol to have a Peloton that if you brought it up in conversation, people would wonder how much money you make that you were able to shell out a few thousand dollars for a piece of fitness equipment.

One online article even highlighted a couple in Brooklyn that said,

“We’re not easily influenced,” Tolley told The Post. “But all these people were telling us it was the greatest thing, that we were going to love it. It started to feel like a cult. We felt like buying into it was becoming this crazy thing where everyone was feeding off each other.”

Cult-like followings are hard to replicate off the bat especially if you don’t have a first-mover advantage, which spoiler alert, Peloton has.

2) Name brand with top talent

Peloton is almost a household name at this point considering all the press it had. It has been seen in various TV/movie spots from Curb Your Enthusiasm, Sex in the City, Bad Boys, and even Billions.

That bright red “P” and white “Peloton” name are hard to miss whenever you do end up seeing a bike being put on display.

Additionally, with Peloton being a status symbol of top-notch quality, that means they also need best-in-class talent to help sell the experience. The instructors are what make Peloton truly special. Each of the instructors has a great personality and they make the classes fly by. Their messages are motivating, not just for that class, but often for life in general.

Messages like,

Many of you in this class may be going through a tough time. Over the past year of COVID we’ve all had struggles. Just know it doesn’t last forever. Showing up to these classes is training for taking on life’s challenges, preserving, and coming out on the other side a bit stronger.

If I was in that class, yeah, I’d be motivated too.

But good instructors don’t come cheap. Many have a huge social media following which allows them to bring over their constituents into whichever fitness company they’re working with at the time.

With great followings come great paydays. Interviews have shown that Peloton instructors make anywhere from a six-figure salary all the way up to over $500,000 in total compensation.

3) High retention

Like all subscription-related companies, retention is key. Lower retention means that people aren’t sticking on your platform long which means you aren’t making as much money per subscriber as you could on an LTV basis.

Peloton has an over 90% monthly retention which makes sense given just how loyal its members are to the platform. More loyal members = more money in the long run.

4) Leader in connected fitness

This one is an easy one because they basically pioneered this type of workout experience. While stationary bikes have been around for decades, Peloton was the one that really kicked off the “tablet on a bike” concept that propelled it into a new class of fitness. Because of its success, many companies have tried to replicate this now.

Some names that you may have heard of like Bowflex, NordicTrack, ProForm, and Echelon are all trying to carve out their stake in the connected fitness space.

Though all of the names mentioned above still do not have the same momentum or clout that Peloton has given how far of a head start they have in the space.

5) History repeats itself

So funny to see how Amazon started off as a simple online book store and then morphed into this behemoth that seems to touch almost every part of our lives.

While this change didn’t happen overnight, the company has a history of acquiring other companies in order to either help consolidate certain parts of an industry or to give it a beachhead into a new category.

Examples of this include:

Zoox - to use autonomous technology in either ride-hailing or its delivery network.

Ring - in a growing bet on delivering packages inside of shoppers' homes and on home security

PillPack - a move to compete with drugstore chains, drug distributors, and pharmacy benefit managers

Whole Foods - an entryway into grocery and food delivery

Honestly, the list goes on and on but you get my point. Buying Peloton seems like it fits the mold of an acquisition target since the only fitness-related product/service Amazon has is its Halo brand.

Valuation

So at this stage, Peloton might seem cheap even after its over 80% drop from its all-time high.

FY’22 sales (ending June 2022) estimates are at $4.23 billion and FY’23 is $4.99 billion. With an EV of ~$11 billion post rumor leaking, that means that PTON is trading at a 2.6x FY’22 and a 2.2x FY’23 EV/sales multiple. This might seem cheap because of all the points I listed above.

It’s impossible to look at it from any other metric because since they aren’t profitable above or below the line we have to look at sales. Could management think they are worth more than $11 billion? No doubt in my mind they think that, however, with recent terrible stock performance and investors calling for John Foley to be removed, a sale at any price above what it closed at on Friday could be very likely.

Bull Case Conclusion

Paying just over 2x next year’s sales for Peloton that’s estimated to grow top line by 18% might not be a bad price to gain access to a new category for the behemoth. A new brand to roll up into its portfolio, ~3.5 million new members it can leverage immediately and with the superior buying power and logistics of Amazon, cost-cutting could make it profitable much faster than anticipated.

I would also chalk up a deal like this to one like when Google paid a hefty premium for YouTube back in the day and now it’s one of their big money makers. The same could be said for Amazon acquiring Peloton. Pay a lot now, reap the dividends later on.

Why Amazon Will Not Buy Peloton

Okay, full disclosure, this is the camp that I’m in. While I agree that all the points above make it a logical choice to be acquired, I think it’s too expensive and that’s why Amazon should just build it.

Here’s why.

History of being the “cheapest” option

So for all of those that know, Amazon has released private-label versions of many of the products that it sells on its site. One of the best examples of this is their Amazon Basics brand which sells thousands of items that are in high demand by consumers at a much cheaper price because it comes directly from Amazon.

Amazon was quick to capitalize on lower-priced goods (low margin) that could be made up for in volume. My take was that Amazon would be able to create a new, cheaper bike that would be still great in quality, but at a more affordable price. This price would make it so that consumers that were on the fence about buying a bike or treadmill in the first place could possibly pull the trigger and buy one.

Not to mention I’m sure they could get free prime delivery instead of having to pay for shipping like Peloton now charges.

So in essence, a larger TAM from the price being cheaper than Peloton. Almost like comparing a Lincoln to a BMW. Still gets you to your destination at the end of the day but by shelling out not as much money.

Part of the Prime offering

To add fuel to the previous points fire, Amazon could also just create its own classes and roll them up into more “added value” to Prime. They might need to considering they are raising prices for their membership.

Beginning Feb. 18, for new members and March 25 for existing members, annual costs will jump from $119 to $139 while monthly costs increase from $12.99 to $14.99.

The company said the 17% increase is a result of "continued expansion of Prime member benefits as well as the rise in wages and transportation costs." Benefits include the expanded free two-day shipping and Prime Video content.

Cough, Cough. That new video content could very well be workout classes. Long shot I know but hey, Amazon became who it is with long-shot ideas.

Even if Amazon converted 1% of its over 200 million Prime members, that’s still a free 2 million members converted to its bike in a short amount of time.

Peloton subs could be Prime members

While I have no hard facts of Peloton subs being prime members, I would put a bet down with confidence that a large majority of Peloton subscribers are already Prime members. I dropped in the HHI data of Peloton and Amazon in the beginning because I wanted to highlight exactly who they cater to.

The reason that I have a problem with this is that it begs me to ask if many of Peloton subscribers are also Prime members. If this is the case, you’re essentially saying that Amazon should acquire the customers it theoretically already owns through Prime. Double paying for a user that you had to acquire for one of your channels while paying again to get them within their fitness world?

No way. That seems like an unnecessary cost to them and is just a terrible M&A execution process.

Instructors are a commodity

The case for Peloton having great instructors and that’s what Amazon would also be buying holds up just as well as a piece of hair in the wind. It doesn’t. While I agree that a sense of community is very important for a fitness brand, I think the instructors go where the money and the perks are.

If Amazon wanted to pay existing instructors more, give them stock options, or other incentives to pull them over to help them grow their own connected fitness classes, I think they would do it.

However, if existing ones don’t want to, the great thing about this industry is that there are always up-and-coming fitness instructors that want to make a name for themselves and if given the opportunity, would seize it. It’s almost like the modeling industry, models are a dime a dozen while also a revolving door. Fitness instructors are no different.

Dime a dozen that come and go all the time.

IP isn’t worth that much

In some more bad news for Peloton, rival Echelon Fitness has persuaded the US Patent and Trademark Office that two of Peloton’s patents related to streaming and on-demand classes aren’t actually patentable.

Two of the patents in question — Nos. 10,322,315 and 10,022,590 — relate to a “system and method for providing streaming and on-demand exercise classes.” In the court’s final decision, the appeal board agreed with Echelon, saying

“The inventions weren’t unique enough compared to prior patents and therefore shouldn’t have been issued in the first place.”

While it may not be the biggest blow Peloton has faced in recent months, it does raise questions about the company’s tendency to be heavy-handed with patent lawsuits.

According to a Bloomberg report, the risk with Peloton’s patent strategy is that it could backfire if courts deem that its “revolutionary technology” isn’t so revolutionary after all. My money is that it isn’t given the fact of the most recent loss to Echelon.

Certain aspects you can’t copy? Sure. But if companies were given a closed door, it’s the successful ones that figure out a way to get around it. Amazon is one of those guys.

Company in shambles

Another point is just how the company is doing right now. While they might not be in the gutter, they aren’t in the best spot either. Business Insider reported that Peloton is considering laying off 41% of its sales and marketing staff and closing down stores. They also hired McKinsey to help it figure out how to cut costs.

Morale is low. Employees who found themselves once to be rich might be grappling with the reality that their shares aren’t worth anything anymore. They’re also mad that John, the CEO, sold a lot of stock to then throw parties and buy $55 million dollar homes in the Hamptons while the company was struggling. A leaked picture of the cancellation of ordered bikes sent the stock tumbling 24% on the news.

The acquisition of Precor to expand Peloton’s equipment production stateside, with one goal being to speed up the delayed delivery times of its home bikes because of current high demand, in hindsight was probably a waste of money.

This is a mismanaged company that is struggling to find its footing. Why would Amazon buy it now and try to turn it around? They could very well just let it bleed a little more and get a better price if they wanted to buy them at all.

John holds the power

John Foley built this company from nothing and I think on a Podcast with Reid Hoffman, he even said he pitched the idea to I think a hundred different investors who basically told him it was a bad idea. He went with it anyway and it became what it is now, minus all the bad PR and the stock tanking.

Since starting the company in 2012, it may be difficult to engineer any deal if John isn’t supportive, as he and other insiders have shares that gave them control of over 80% of Peloton’s voting power as of Sept. 30, according to a company proxy filing.

That means he and his other insiders could very well veto a deal if they think they can get more than Amazon is willing to pay no matter what the little guys beg him to do.

Valuation

Liked I mentioned in the bull case for acquisition section, we can estimate that PTON is worth $11 billion in EV post the 26% run-up in the stock after hours on Friday. While the 2.6x or 2.2x sales might seem cheap, I wanted to use a metric that I’ve become fond of as we start to see more subscriber-based companies become public.

The metric is EV/subscribers and you can see my post where I briefly break it down here with other consumer-oriented companies (How Much is Each "Subscriber" Worth?).

When looking at Peloton to other subscriber-based businesses, I chose Spotify and Netflix, the numbers are pretty off.

Per subscriber, PTON is estimated to be worth $3,295 compared to Spotify’s $74.50 ($31 billion EV with 416 million subs) and Netflix’s $874.50 ($194 billion EV with ~222 million subs).

Seriously? I will admit, this omits the factor of the hardware of Peloton which I get (before anyone comes at me with that) but if you’re betting on the company to become a leader in the digital space, a) not very many people can still afford a Peloton no matter how many interest-free 43 month offerings you can give them and b) per household you only need one, technically.

Bear Case Conclusion

I think that Amazon to buy at these levels would be grossly overpaying. Yes, while Peloton does have a great brand, a growing loyal community with an excellent fitness machine, it’s just too expensive.

If the all-in price was $8 billion, I’d be more inclined to say they’d do it but up until Friday, this company had a strong downward trend even after releasing preliminary results to slow the bleeding.

I think if the deal could be valued at sub $8 billion, then it could be a very real thing, otherwise, no dice. Additionally, like all other big strategic companies out there, Amazon does have its own in-house M&A team. This “rumor” could very well just be them looking into it because that’s their job. Literally looking at anything and everything that could remotely make sense to acquire.

Doesn’t mean they’ll do it, just that they’re taking a peek under the hood. If that ends up being the case, PTON could very well nose dive again.

Closing Arguments

Both sides have great points. The debate in my thread was very healthy and no one was out of line which I appreciate. I think none of us know what will happen here but I think there are two main themes here.

Bulls want it to happen because they’re so down in the hole that this buyout could be a saving grace. If they weren’t in the hole then they would probably have said Peloton could eventually figure it out.

Bears don’t think it could happen because Amazon can just build it themselves and do to Peloton what it did to Diapers.com.

Either way, it will be interesting to see how the market reacts to this come Tuesday when Peloton reports official Q2 FY’22 earnings.

Until next time,

Cedar Grove Capital