📈 Urban-Gro will grow your returns

Missed out on Agrify's stunning 200% return? This might be the next one.

Summary

The company is jump-starting growth by pushing more into the high margin and recurring services revenue post its recent acquisition of MJ12 Studio

One step closer to being able to offer a full end to end turn-key solution to clients that can be highly lucrative for the company

Strong secular tailwinds will allow the company to continue to capture market share in not one, but two industries - cannabis and vertical farming

With $50mm in cash and little debt, the company is not under threat of running into liquidity issues anytime soon and has amassed a war chest for all its planned growth initiatives

Business Overview

Urban-Gro UGRO 0.00%↑ is a vertical farming company that is very similar but not 100% to Agrify AGFY 0.00%↑. The company specializes in engineering, designing, and building indoor farming facilities. Once they have built out these facilities, they then integrate complex environmental equipment systems into those facilities.

Similar to Agrify, it aims to sell its farming equipment units but by becoming a leading turn-key solutions provider. Meaning, that they own the full process from start to finish.

Recently the company acquired MJ12 Studio, a leading global horticulture company that engineers and designs commercial controlled environment agriculture systems. This acquisition greatly expands Urban-gro’s services offering by creating the industry’s first fully-integrated architecture, engineering, and cultivation systems integration company serving the cannabis and food-focused CEA sectors.

Financial Highlights

Urban-Gro has had a tough time maintaining its topline growth rate over the years. The company has only grown revenue from $20mm in 2018 to just $26mm at the end of 2020. This represents a CAGR of only 13.5%, in comparison to 161.4% for Agrify (AGFY) during the same time.

However, the company plans to revitalize this growth with three areas of focus (which I’ll talk about more in the next section).

Continued expansion of high-margin services offerings

To become the leading provider of turnkey, indoor, high-performance cultivation facilities

Expansion into the European market

What should quickly be noted is just how small their other business sales are in comparison to current equipment sales, which accounted for over 95% of sales as of Q2 2021.

If the company is to expand its services business, it will have to be able to make up more of sales, proportionately, than it currently does.

Perhaps the most notable thing from the Q2 2021 earnings was the huge increase in their backlog, which increased from $15.2mm at the end of Q1 to $27.9mm at the end of Q2.

Backlog consists of signed contracts that historically have taken two quarters to convert to recognized revenue. The backlog doesn't contain anything from the MJ12 acquisition, this is all organic and the result of investing in growth.

Though management has not issued any guidance after this two-quarters of backlog, they do mention that there is still plenty in the works but only feel comfortable reporting what is signed and sealed.

Strong Secular Tailwinds

As part of being a vertical farming equipment maker, naturally, they fall into supplying the cannabis side of things.

The global cannabis market size is set to gain momentum owing, observes Fortune Business Insights in an upcoming report, titled, "Cannabis/Marijuana Market, 2019-2026" owing to its increased use for medicinal purposes. According to the United Nations Office on Drugs and Crime (UNODC). Cannabis has therapeutic and medicinal benefits. As per the report, the market size was USD 10.60bn in 2018 and is projected to reach USD 97.35bn by 2026, exhibiting a CAGR of 32.9% during the forecast period.

Additionally, under the same principle as above, the company can supply the farming space as well, and have mentioned this in their most recent call transcript.

“So not only are we continuing to capture more market share in the global cannabis market, but we're also successfully expanding our reach within the food-focused vertical farming market as well.”

The vertical farming market is projected to reach USD 7.3bn by 2025 from USD 2.9bn in 2020; it is expected to grow at a CAGR of 20.2% during the forecast period. Major drivers for the growth of the market are high yield and numerous other benefits associated with vertical farming over conventional farming, advancements in light-emitting diode (LED) technology, year-round crop production irrespective of weather conditions, and the requirement of minimum resources.

If you’d like to read more in-depth on the vertical farming space, I’ve written a recent article (~5min read) explaining why it’s so important and why it makes for a great investment.

Key Growth Initiatives

Further Expansion into Services

Services by default are higher in margins compared to physical equipment. Naturally, you would want to move towards a more services-oriented business increasing blended margins. Even to an extent, this shift from hard goods to services can be perceived differently at a valuation level which could help out with the multiple the company can command. More on this later.

“With the successful acquisition of MJ12, we've now expanded our existing offerings to include architecture and interior design services. And as a company, we're diligently working to blend our existing engineering and cultivation design services into their 70 open projects, definitely phenomenal, cross-selling opportunity for our team.”

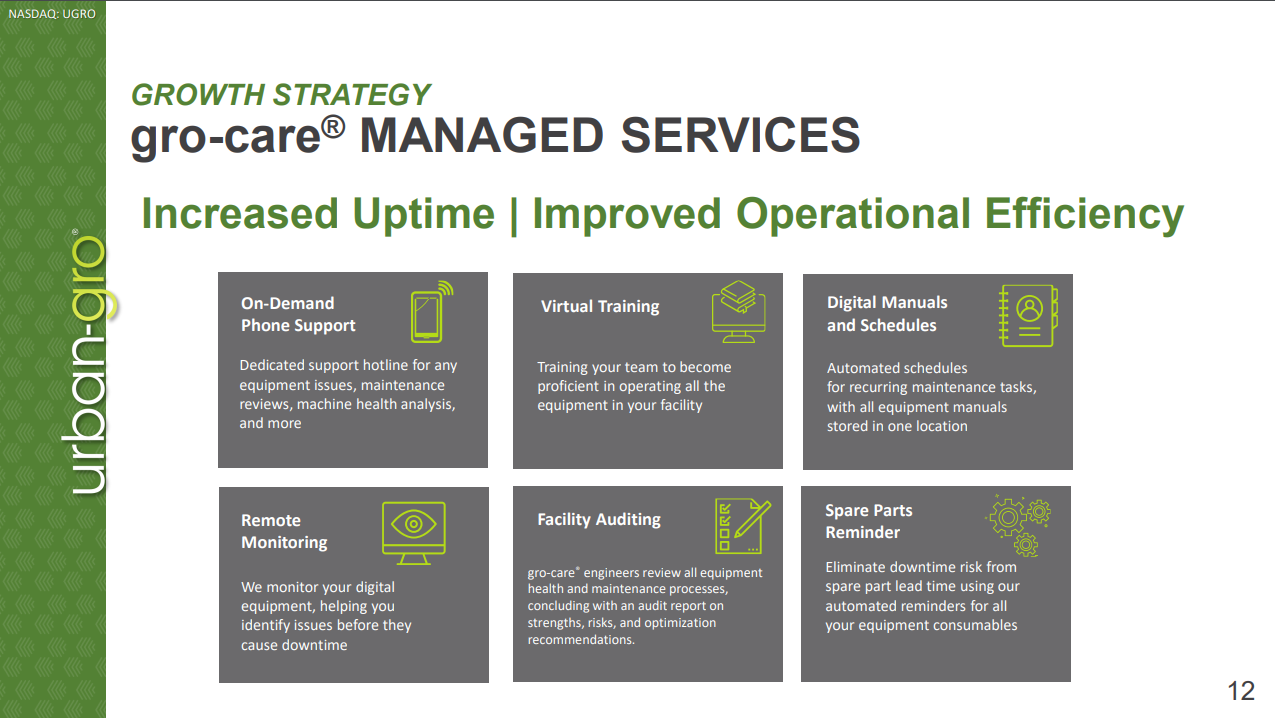

Additionally, besides expanding overall services, the company is looking to grow its in-house ‘gro-care’ service. This ‘gro-care’ service offers facilities with providing training support, monitoring, and a variety of programs, including maintenance.

Through the company’s expertise in over 450 facilities, this service offering further supports the company’s ability to provide a full service offering that many facilities and operators desire.

Becoming a Leading Provider in Turn-Key Solutions

Urban-gro defines turnkey as delivering, a fully operational, customized, high-performance facility. Basically, they handle the full build of the actual facility from start to finish to then sell as a finished product. This isn’t just selling equipment or providing services here or there, but quite literally building out an entire facility and handing over the keys once the sale is complete.

This is very similar to what Agrify is doing with its own turn-key solution that is targeting between a 40% and 50% IRR. Should Urban-Gro even get half the targeted IRR that Agrify is, this can become a very profitable business line.

European Expansion

The European market is prime for growth. Currently, the cannabis market is valued at roughly $250mm with a market expected to exceed $3bn by 2025. This leaves for a lot of whitespace for Urban-Gro to capture and gain a foothold on the continent.

“In addition to making significant advances working with our commercial agents that we signed in Q1, we've retained the Vice President of Sales based in the Netherlands, who has strong horticulture ties, who has strong horticultural ties to the European and Middle Eastern markets.

Further later this month, we're opening - we're both opening our European entity in the Netherlands, and we're also exhibiting in a large cannabis tradeshow in Germany.”

The company has been very vocal that they want to move quickly into Europe and labels its turn-key solution as key for their success there.

“They [clients] want the on-site project management, and they want somebody there to help guide and hold their hand as they start up the facility and train their teams. So they - this acquisition really was fueled by the demand that we saw over in Europe.“

The above quote is in relation to the reason for the MJ12 Studio acquisition. I do have some reservations about this which I’ll touch upon in the next risks segment.

Some Risks to Highlight

Revenue

They're still a small company and are still trying to revitalize their sales growth with an emphasis on services revenue. Having seen a decent jump over the last few quarters, y/y growth rates are hard to predict given the nature of its business.

We should start to see this normalize over the next year or so as they establish more of a footing of what normalized revenue growth will look like.

Gross Margins

Since they are still establishing their business segment base, we can expect large fluctuations in gross margin as they try and move towards services-oriented sales vs. traditionally equipment-heavy sales.

“So the margins that we see in any given quarter become a little bit dependent on well, what customers bought what products from us during that, or what systems from us during that quarter.

But we're keenly focused on looking to try to improve all of our margins to the extent that we can and taking advantage of opportunities that are out there to us.”

Here’s a quick understanding of what each revenue stream targets for gross margin as well.

Equipment Systems - mid-teens to mid-thirty percent

Consumable Products - high-teens to high-twenty percent

Services - thirty to sixty percent

Overall, margins will be highly contingent on swings from high margin services to low margin equipment sales as time goes on.

Concentration Risk

Given that the company is still relatively small, they have two customers that leave them exposed should they cut their relationship with UGRO. As reported in their most recent quarterly earnings, six months ending June 2021, one client represented 46% of sales while another represented 15%.

Liquidity Challenges

Urban-Gro is a small company (micro-cap) and thus has not garnered a lot of attention like other mainstream vertical farming-related companies. The average daily volume is only 245k shares so if you need to move quickly, spreads might eat into your profits or extend losses.

Should you take a position in this company, planning to scale it upwards or downwards must be noted.

European Expansion

Europe is lagging behind the US in both cannabis and vertical farming capabilities. I do believe that international expansion is a natural next step for many companies though my fear is that Urban-Gro might be too young to take this on.

International expansion is a costly step and though they have $50M in cash in the bank, setting up a new European headquarters, sales team, and whatever else is needed to make sales might eat into their war chest.

Valuation

As I’ve mentioned before, Urban-Gro (UGRO) is a small company, only having a market cap of $164mm as of Monday’s close. With $50mm in cash on the balance sheet and no debt (they paid it all off earlier in the year), their enterprise value sits at just $113mm.

Factoring in management guidance of $54-$59mm for fiscal year 2021, that implies an FY’21E EV/Sales multiple of just 1.9x (using top of the range). At face value, this seems incredibly low to me for a few reasons.

The addressable market is only getting bigger and even if Urban-Gro were to only capture small players in the U.S. and Europe, I’m still very bullish towards that demo.

Using this guidance of $54-$59mm, implied y/y growth is estimated at 128%. Trading at 1.9x for a company essentially doubling revenue is ludicrous.

Transition into a more services-oriented business and eventually, less of a hard goods business (proportionally) should command a slightly higher multiple.

By no means am I to suggest that Urban-Gro should be valued in the same lines as Agrify. They simply aren’t apples to apples. More like tangerines to oranges. In the same family but slightly different, plus Agrify is just growing much faster than Urban-Gro at the moment which brings me to my next point.

Agrify is trading at the same FY’21 EV/Sales of 10.6x and has a growth rate that is ~3x more than Urban-Gro. Even if you want to keep it simple and give the company 1/3 of the multiple that Agrify has, then that leaves you with a multiple of ~3.5x.

Taking into account sales guidance and shares outstanding, this implies a share price of $19.85, a 27.4% increase from Monday’s close.

Conclusion

If you haven’t noticed already from my previous posts, I’m a big fan of vertical farming. I would almost put my excitement for this industry as up there as when I was when I first discovered Telsa back in 2014 (was the first stock I ever owned).

Having the option of getting on the ground floor of a small company that has a massive opportunity is abundant in the land of vertical farming, just not many are currently public.

Urban-Gro is unique because of how they historically have done business and what they are focusing on in the immediate future to drive long-term growth.

With little short-term risk of the company going under (remember, no debt), a healthy balance sheet, a recent acquisition that is immediately accretive, I believe that Urban-Gro has great potential to be more than what it currently is.

To estimate the value of this stock at just under $20 a share is just bananas and just like when I pitched Agrify multiple times when it IPO’d and when it dropped almost 50%, look at where we’re at now.

Note: Price at the time of writing: $13.48.