Twitter: The Modern Comeback Story

How an age-old tech company went from a slow burn to coming back with some sharp teeth and "reach for the moon" goals

Summary

Twitter’s aggressive M&A activity can bring in great value-additive capabilities and offerings as it plans to fully launch its first subscription service

Diversification into various revenue-generating businesses will allow the company to not only rely on its historical core business model while bringing in new users onto the platform

Twitter Blue can become a very promising foray into a more stable, revenue-generating business once they figure out how to efficiently build its offerings

Business Overview

I’m going to handle this report a little differently this time. Usually, I would go in-depth to a point about who the company is and how they’ve performed historically but this one is pretty self-explanatory and I want to focus more on its new initiatives.

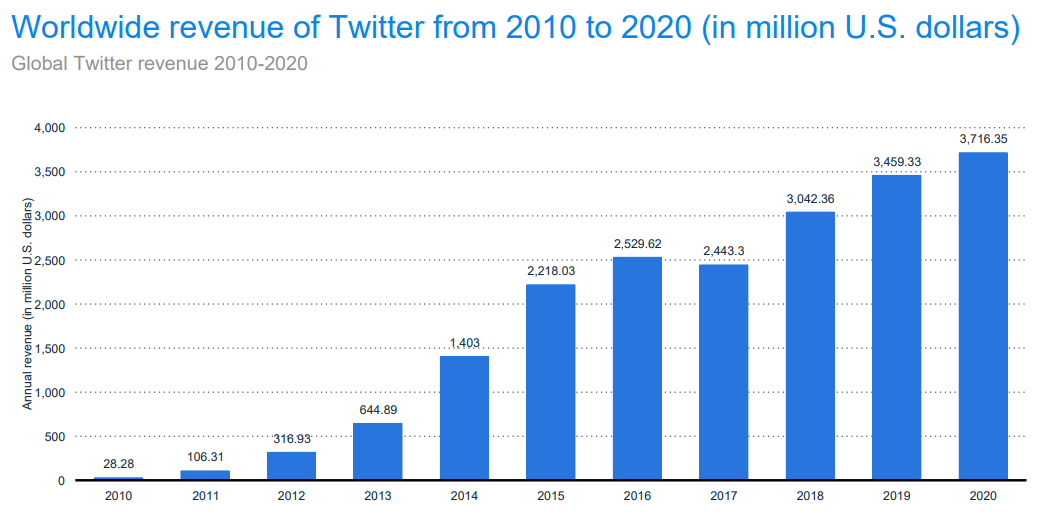

As a quick check off the box though, its revenue and adj. EBITDA is growing and they are profitable on a net income GAAP basis.

As many of you know, Twitter TWTR 0.00%↑ created the short form SMS text that later became known as the “tweet”. Each tweet can support 280 characters and is a way for people to essentially share their short status updates or thoughts that they have going on.

Their business model was very similar to Facebook, get users to stay on the platform for as long as possible and sell advertisements along the way. However, unlike the scalability of Facebook, Twitter never really changed its core business and has only managed to increase mDAUs (monetizable daily active users) by 82% from Q1’17 - Q1’21 (109 to 199).

The platform gained wide popularity during Trump’s presidency since that was his preferred medium to speak to his constituents.

Twitter’s Bet on the Future

Twitter knows that they aren’t going to get much growth if they continue this course, and with rival companies popping up like Clubhouse, Substack, TikTok, etc., Twitter is aggressively making sure it does not fall behind. The company has three goals they are trying to achieve.

Double development velocity by end of 2023, resulting in doubling the number of features per employee that directly drives either mDAU or revenue.

A goal of 315M mDAU in the 4th quarter of 2023, which requires continued compounding growth at about 20% per year from the base of 152M mDAU they reported in the 4th quarter of 2019.

Double total annual revenue to over $7.5b by Q4 2023. This requires them to gain market share with performance ads, grow direct response advertising, and expand their products to small and medium-sized businesses throughout the world.

This aggressive stance on building the future of Twitter all starts with keeping more users within Twitter, and its services, and attracting new ones. Twitter should be able to capture a large number of dollars as more eyes shift to mobile, video, and audio platforms.

Ecosystem bet fueled by M&A expansion

What helps make for a great business to invest in is the ecosystem that they create. I’ve written a few posts in the past (Petco and Barkbox) where I talk about how each has created various products/business lines that keep people coming to them instead of going elsewhere. This effectively builds a defensible moat and makes it harder for customers/users to go elsewhere.

Apple is the gold standard for building an ecosystem, keeping its users within the iOS platform amongst all its products, and developing a strong hatred for anyone that contained the green texts (yes, I am one of those green text people #teampixel).

So how is Twitter trying to build its own ecosystem? Simple, by buying or building their own capabilities to compete with other players currently popping up in the market.

Twitter Spaces (audio) -> Clubhouse

Twitter Fleet (stories) -> Instagram/Snapchat

Twitter Revue (newsletter) -> Substack

Twitter Scroll (app/website noise) -> I relate this to a Hulu/YouTube premium where you pay to remove ads, not that they are competing with Hulu/YouTube

Twitter Blue (membership) -> Patreon, OnlyFans (for the business model, not how it’s widely used now)

We’re focused on two specific things. Enabling new use cases for conversations on the serivce and rethinking the incentives of the service.” - Dantley Davis, Head of Research and Design

Spaces - the Clubhouse of the Twittersphere

Audio has come a long way — from early music streaming services to audiobooks, podcasts, and more. Technology continues to streamline access to audio resources, with wireless earbuds and other hands-free wireless tools reducing friction and making it easier to listen and issue voice commands.

Podcasts, specifically, have exploded in recent years. As of the end of 2020, Spotify, one of the dominant forces in the market, was hosting 2.2 million podcasts, and around 25% of its monthly active users engaged with podcast content in the fourth quarter of last year.

People seem to love the connection that comes with audio, and they also love the ability to multitask while listening or interacting. Instead of sitting down at a keyboard or focusing on a phone or TV screen, audio allows you to interact and connect in diverse settings — while cooking, running, or watching your children at a park.

Since we’re talking about how Twitter can replicate and apply its own flair to already existing products, let’s look at how well Clubhouse is doing. Clubhouse launched in April of 2020, right after the world went into lockdown and since then, the company has over 10M weekly active users.

Interestingly, Clubhouse is actually pre-revenue, meaning they have no system in place to actually monetize anything at this current point in time. How over 180 VCs thought they were worth $1B is beyond me but that’s for another discussion. The company thought of monetizing their platform to allow users to send payments to the hosts to support them, almost like a tip.

The way I see Twitter possibly monetizing their Spaces platform can be from:

Playing advertisements before the audio room takes place or during (i.e. YouTube)

Holding exclusive rooms and taking a cut from the host who charges a “cover” to enter and listen in

Take a fee of tips that are sent to the host (facilitating the transaction) by users to take part in the audio room.

These are all hypothetical numbers but you can see what I’m getting at by being able to monetize and considering how Twitter already has ~200M mDAUs, converting even a small % of them into a Spaces user won’t be difficult I imagine.

Revue - the answer to go head to head with Substack

Revue is a Dutch startup that allows users to publish and monetize email newsletters. While Revue hasn’t driven the same wave of “is this the future of media?” think pieces as Substack, it counts major publishers like Vox Media and The Markup as customers.

Newsletter writers typically offer a mix of paid and free options and earn money primarily through subscriptions. Platforms like Revue and Substack take a cut of those subscription dollars. But while Substack’s cut is 10%, Revue’s is 6%. Twitter said it would lower Revue’s cut even further, to 5% in an attempt to attract new writers.

The financial details of the acquisition were not disclosed. According to Crunchbase, Revue had raised €400,000 from various angel investors so we can’t imagine that an initial uptick in revenue is in the cards, but this isn’t necessarily the near-term objective is it?

If you want to compare Revue with possibly achieving the status of Substack then let’s look at how it could scale. As of late, Substack has 12 million people who visit the site every month and has over 500k+ paying subscribers.

If you were to estimate each subscriber paying, on average, $10 a month for a year, at a 5% cut, that only equates to $3M in incremental revenue. Which is nothing.

Keeping users within the ecosystem is what Twitter is aiming for, not really collecting the 5% fee that they would get on paid subscriptions. In fact, the 5% fee is quite non-material but the amount that they could earn from ad revenue is multiples of that considering over 12M people visit the site every month.

Twitter Scroll

Scroll, a subscription service that offers readers a better way to read through long-form content on the web, by removing ads and other website clutter that can slow down the experience. The service will become a part of Twitter’s larger plans to invest in subscriptions, the company says, and will later be offered as one of the premia features Twitter will provide to subscribers.

This is what I meant by comparing it to Hulu/YouTube where you want to see the content but then you keep randomly getting shown video ads or surveys to complete. Scroll essentially gets rid of all that and shows you a seamless user experience while you’re on the platform.

For the time being, Scroll will pause new customer sign-ups so it can focus on integrating its product into Twitter’s subscription work and prepare for the expected growth.

Twitter Blue subscription

Twitter’s first foray into a subscription offering is via its newly launched Twitter Blue service for $2.99 a month. The service is only being tested in Canada and Australia as of the moment but the subscription will allow Twitter users to access premium features, including tools to organize your bookmarks, read threads in a clutter-free format and take advantage of an “Undo Tweet” feature — which is the closest thing Twitter will have to the long-requested “Edit” button.

This service offering is in its infancy and many have voiced that Twitter is charging users for what seems to be basic product update functions is outrageous, though the company has stated that they are using this as a starting point to figure out what does and doesn’t work. I believe that as a part of Twitter Blue, many of the other capabilities that the company is building out could be incorporated into this overall subscription service and making it more of a value add to have it than to not.

Again, the dollar value is not the end all be all from the service since if you consider just 5% of Twitter’s users convert to Twitter Blue (~10M), that’s only $359M worth of annual revenue for the company (assuming no-churn). Far from the bridge to get to $7.5B that is planned.

We’ll have to stay tuned to see how this plays out but the emphasis that I want to call out is that they are actively, and aggressively, trying to explore various revenue-generating opportunities, aka putting their money where their mouth is.

Valuation Support

The whole premise for going long Twitter is if you can truly believe that the company will either achieve or come close to achieving its ambitious goal by the end of 2023.

Doubling revenue is no easy feat for a company, however, Twitter is not just relying on its existing products but also aggressively building out its product framework and going head-on with acquisitions, as I mentioned previously.

But how do we bridge the gap so quickly?

Adding more monetizable daily active users (mDAUs)

Twitter has increased its annual mDAU net adds each year since 2018, with mDAU growth driven by product improvements growing 3x over the past 3 years. The company ultimately hopes to increase top of funnel by making the platform appealing to larger audiences and then improving retention with better relevance of recommendations using Topics, Lists, & Search to drive personalization.

“A few years ago it may have taken 6 months to a year to get a single feature or new product to our customers. While we are in a better position today, consistently bringing this down to under a few weeks is a goal of ours.” - Jack Dorsey, CEO

Diversification and durability of revenue streams

Twitter’s multi-year product roadmap centers around

Monetizing additional surfaces (i.e. Fleets) & leveraging signals from Topics/Lists to improve ad targeting & monetization.

Diversifying revenue beyond ads through features like subscriptions & commerce.

Currently, 85% of Twitter’s ad revenue comes from brand ads vs. 15% from direct response advertising, but investments in measurement & conversion should help bring the ratio closer to 50/50 over time.

Crunching the numbers

So when it comes to valuation, and how the main goal here is to double sales, I wanted to take a look at the whole company in regards to others in the space on an EV/Sales multiple.

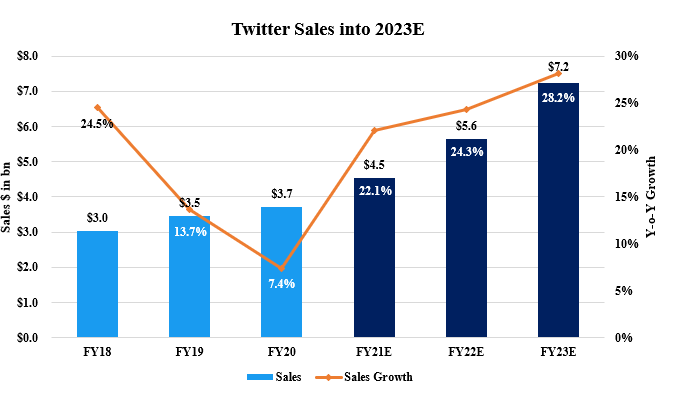

Though I am optimistic that Twitter can achieve its goal of doubling revenue, I ended 2023E with $7.2bn instead of the goal of $7.5bn+. I wanted to leave room for a margin of error should not everything go as planned.

Revenue growth for fiscal years 2021 through 2023 is high but this accounts for all the planned M&A activity and integration, product improvements and buildouts, and the long-anticipated full launch of Twitter Blue.

When it comes to competitors to comp against, there aren’t many pure plays so I went with Alphabet GOOGL 0.00%↑, Facebook META 0.00%↑, and Snapchat SNAP 0.00%↑. All are involved in the advertisement space and each has its own platform(s) that they operate.

Looking at forward sales multiples, Twitter is always below the average but above the median. Because I’m only comparing Twitter to three companies, I’d rather look at the average considering that the basket of companies is very aligned as far as ad-driven business models. I included the median in case many of you figured I was being biased so I thought I’d save the trouble and include it.

For the multiple that I used for Twitter’s FY 2022E sales, the average is 9.5x, however, I actually increased it by 20% to account for the added growth that behemoths like Google and Facebook aren’t commanding, but that Snapchat is.

Looking at 2022E sales growth, Google is at 16.7%, Facebook at 19.3%, Snapchat at 48.7% and I have Twitter pegged at 24.3%. Because of the nature in size, and growth prospects mentioned throughout this entire post, I felt that the additional bump of 20% in the multiple was justified leaving me to base Twitter’s future value off of an FY 2022E EV/Sales multiple of 11.4x (this accounts for the 20% increase from 9.5x).

This gets me to an implied share price of $80.30. This means there’s a 33.2% upside from yesterday’s closing price of $60.25.

Conclusion

I thought Twitter was stupid and personally on its way out, but I was one of the people that tried it out during Trump’s presidency to get his tweets and other information and found the platform to be useful when used effectively.

Having converted and become a believer, I think that Twitter is on track to finally deliver on promises to bring its company to the next level and make it into the great company it can be.

I would be foolish to not mention that any hiccup in their growth journey (e.g. regulation, failed integrations of acquisitions or product developments, etc.) could seriously cast down on the viability of achieving their 2023 targets.

*The current stock price at the time of this article: $59.83