🚀 SPCE Coming Back Down to Earth

Despite Virgin Galactic's recent string of good news, this over-the-moon valuation cannot be justified

Summary

Virgin Galactic has had a string of good news from successful test flights to putting the first billionaire into space, but the stock’s future growth is already priced in

The company boasts questionable revenue targets given inherent risks and still no update on when they will re-open reservations

The space tourism business is capital intensive and SPCE will most likely need to raise additional funding to build additional spacecraft, spaceports and to fund operations effectively causing further dilution to shareholders

Big names, including the founder, Richard Branson, have either sold off their position entirely or reduced it

Business Overview

SPCE 0.00%↑ stock debuted on the NYSE on Oct. 28, 2019, becoming the first publicly traded commercial space tourism company after a reverse merger with Social Capital Hedosophia Holdings.

Virgin Galactic is an aerospace company that provides human spaceflight for private individuals and researchers. The company is focused on developing a spaceflight system to offer customers a multi-day experience culminating in a spaceflight that includes several minutes of weightlessness and views of the earth from space.

Their flagship spaceship, VSS Unity, is designed to hold up to six passengers along with the two pilots. The company has about 600 reservations for tickets on future flights, sold at prices between $200,000 and $250,000 each. While future passenger ticket sales have yet to be announced, UBS estimates that the price point for tickets will likely rise to between $300,000 to $400,000 per ticket, with prices potentially becoming more accessible as operations scale and costs are reduced.

However, the company is still not flying paying passengers to the edge of space yet, so there is no revenue coming in and losses are piling up. They have two more planned test flights, one of them being with the Italian Airforce for a research mission, that is expected to take place in late summer and early fall. Until those test flights are cleared, revenue-generating commercial flights are not to be realized until 2022 at the earliest.

Key points to remember as you read through the rest of this post:

They have a product (spaceship) but no revenue other than the current reservations

They are losing money while they continue to test their spaceship for commercial use and get full approval for commercial flights

At the end of the day, this business is not as simple as building a car

Investment Thesis - SHORT

While anything space-related is one of the “hottest” things to invest in at this moment, many are either pre-product or pre-revenue and boast valuations that are all aspirational.

FOMO (fear of missing out), is what’s driving investors to these companies to capitalize on them while they’re young to ride them out into the future. The problem with that is, many of these companies don’t plan on making any sales until years down the road, and while investors wait, they are paying for companies in the billions of dollars in valuation with little to show for it.

What I find funny is how you read articles and analyst reports that talk about being valued at 50x 2025E sales (as an example) like it’s normal practice. 1) 50x sales better have some outlandish growth rates to justify that and 2) how are you supposed to value a company that’s trying to convince you to look five years out as a point in time to determine what it's worth? Tomorrow the spaceship could explode and the stock sinks by half.

For now, the stock has been pumped by this momentum trade but without future reservations being bought, full approval status not happening yet, and years of future revenue already baked into the price, this stock is flying a little too close to the sun.

Big questions on making money

To understand how Virgin Galactic is expected to make money, you have to think about what its capabilities are.

Sending people up to space so they can experience gravity and views from the earth 80km from the ground

Transporting equipment and people to space (which the company already has a contract with NASA for a training program)

Transporting people and equipment from point to point

These are all very ambitious goals but they all have huge addressable markets, however, only the first point is the most immediate while point two is the next.

The company expects to generate $1bn in sales per spaceport (the hub they use to launch the spaceship), though analysts are expecting revenue of $550m in 2025. Each Galactic spacecraft is expected to make roughly 36 flights a year carrying about six passengers into space.

The uncertainty of the long-term outlook of the company is what makes the valuation hard to justify.

To point one, while going to space has massive bragging rights, there are a few flags that are worth noting that make this a blockbuster endeavor for the company.

1. How many can afford a $250,000 ticket?

At that hefty of a price tag, there aren’t that many individuals that can even afford that. According to Vertical Research Partners, about two million people can afford to go to space, with that high-net-wealth population growing at around 6% each year. It estimates that Virgin needs to transport around 1,700, or about 0.08% of those individuals, to space each year for its model to work.

That’s not that many people who would pay for a flight to be lucrative. What’s worse, is how many of those are to be repeat business? Something like going to space is a once-in-a-lifetime experience unless you have to throw away money to go multiple times throughout your life, which reduces the pool even further.

2. It’s not “technically” outer space

If convincing enough people was hard enough to surrender a quarter of a million dollars for a space flight, how about you find out that it’s technically not space. Virgin Galactic launches its spaceship Unity to an altitude above 50 miles (80 km), which NASA, the Federal Aviation Administration, and the U.S. military classified as space. Any person traveling above this line will earn astronaut wings for reaching that height.

However, another widely recognized boundary of space, the Kármán line, is at an altitude of 62 miles (100 km) above Earth. The SpaceShipTwo VSS Unity won't reach this milestone, which has led Virgin Galactic's competitor Blue Origin (which does fly higher than 62 miles) to call out Virgin Galactic for missing that mark.

So yes, it’s space, but not really space. It’s merely a point in space that happens to be one of the lowest points. Why pay that much money if you have to fight with people that have legitimate reasons to question you?

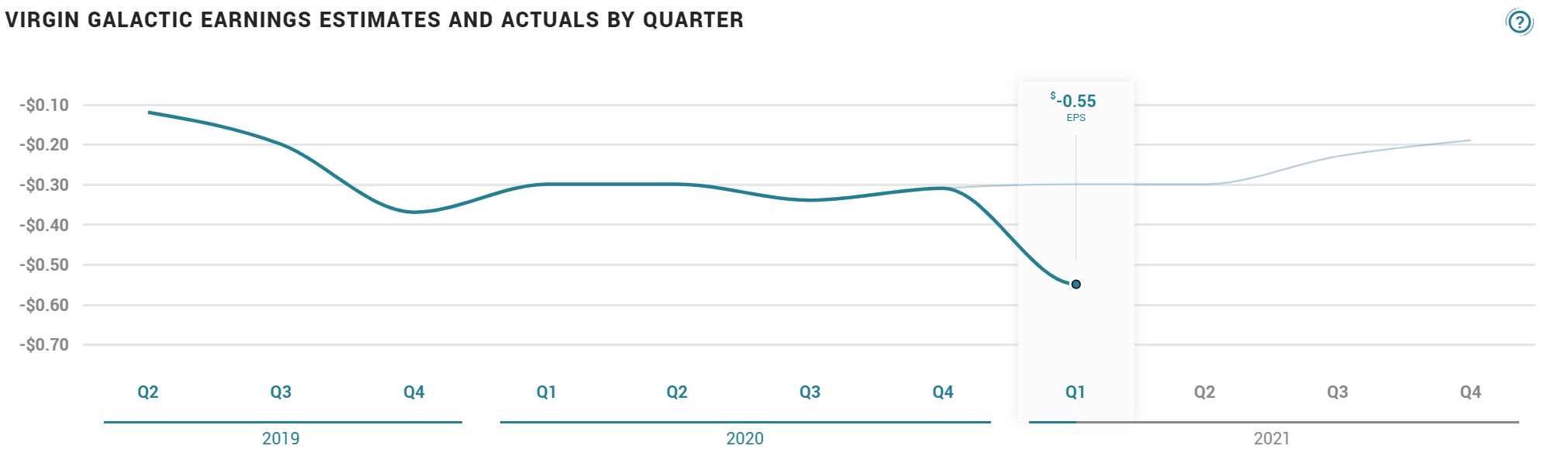

Losses are mounting

On May 10, Virgin Galactic reported a Q1 per-share loss of 55 cents, missing Wall Street expectations for a loss of 31 cents a share and widening from 30 cents a year ago, on no revenue.

Though the company has been in business for nearly two decades, they’ve equally lost money over all that time.

Available cash slipped to $617 million from $666 million in Q4. The company expects free cash outflow to worsen to $60 million in Q2 from $50 million in Q1. The longer the company is delayed by launching commercial flights, the more the company will continue bleeding its cash reserves.

More money needed to fund operations

Building a fleet of spacecraft is not a cheap thing to do let alone build out all the infrastructure for point-to-point travel. With massive losses continuing to pile up, $617m in cash in the bank, and recognizable revenue not expected until early 2022 at the earliest, Virgin Galactic is going to need more money.

Since going public, the company has had a few secondary offerings to boost cash reserves and remain in good standing to fund growth and operations until they can start really selling tickets.

Right after their most successful flight with Richard Branson, the company announced a $500m stock offering that sent the price down nearly 17%.

The spaceport that the company currently built for all its flights so far costs about $200m. Its new spaceship it’s working on finishing up will cost between $35 and $55m.

If you extrapolate its projected FCF loss of $60m in Q2, then you’re looking at a run-rate loss of $240m a year. Though this extra $500m will definitely shore up the balance sheet, to put gas on whatever embers are still burning, it may need more to do so.

With breakeven so far into the future, I would not be surprised if they raised more money in the next few years to fund operations and break ground on its future spaceports.

Key investors dumping shares

Key investors have also been publicly selling their positions in the company for various reasons, sewing doubt that the company has much more upside left.

Cathie Wood's exchange-traded funds launched a massive sell-off of Virgin Galactic shares in late March.

ARKX Space Exploration (ARKX) began with 672,000 shares back in March dumped all Virgin Galactic stock by May. Her ARK Autonomous Technology & Robotics (ARKQ) ETF sold 1.65 million shares during May and no longer has a position.

Richard Branson sold about $150m worth of shares, about 2.5% of the space tourism company, in mid-April, according to a recent regulatory filing.

In early March, Chamath Palihapitiya, the chairman of Virgin Galactic, tweeted that he sold his 6.2 million-share personal stake. The stock was worth about $213m. But he still owns 15.8 million shares via his special purpose acquisition company, Social Capital Hedosophia Holdings, which took SPCE stock public.

If key investors are dumping their shares, that’s not really a vote of confidence in the long-term growth potential of the company.

Competition is heating up

Space is a hot market and Elon Musk is arguably the one that revitalized the space race after it had been ruled as too costly by governments around the world.

Many companies have entered the industry in various capacities stretching from launching satellites into space, space tourism, asteroid mining, internet capabilities for the masses to even the ambitious goal of colonizing the moon and Mars.

To name a few companies in the mix:

Blue Origin (Jeff Bezos)

SpaceX (Elon Musk)

Virgin Galactic

Virgin Orbit

AST Mobile

Rocket Lab

Momentus

Astra Space

And this is just a shortlist. Many have an overlap since they involve rockets but the functionality, size, components are different in their own unique ways.

To say that Virgin Galactic is to make up the majority of space tourism is just a farce assumption. Though they have been perfecting their technology for the last two decades, first-mover advantage isn’t always an advantage when technology and improvements have significantly grown since then. Even Rocket Lab has made their whole business model based on 3D printing rockets to make them cheaper and reusable.

Competition breeds pricing pressure and in theory, a race to the bottom. This is exactly what happened in the food delivery space and ride-hailing (Uber and Lyft). Though I don’t believe that pricing pressure would happen immediately, it could impede on growth prospects as more companies come online vying for the same market that Virgin Galactic is trying to cater to.

This only reinforces my point that there are X amount of people that can even afford it, now imagine if five companies are doing the same instead of one.

Valuation

At the time of writing this, SPCE is currently worth ~$9bn based on its market cap. Depending on how you cut the data, reports show that the space tourism market is only going to be worth $3bn by 2027. Given Virgin Galactic’s $9bn market cap, it’s worth 3x the entire market in just a few year’s time with no plan on how to scale the business or achieve profitablilty.

Analysts already estimate that they will have revenue of $3m for 2021E, $57m for 2022E, and scale to $550m in sales in 2025E. At current estimates, that means that the company is being valued at 165x forward P/S. That’s absurd given that so many things can still continue to go wrong.

Weather delays or faulty flights would lead to either refunds or pushing back the list of people waiting to go up to space

As we’ve seen with SpaceX, there’s a lot that can go wrong with rockets, and blowing up is usually at the top of the list (hopefully that doesn’t happen)

Not being able to increase spaceships or spaceports to grow topline

All these three points just focus on revenue since the prospect of them earning any positive bottom line is as far away as the moon currently is.

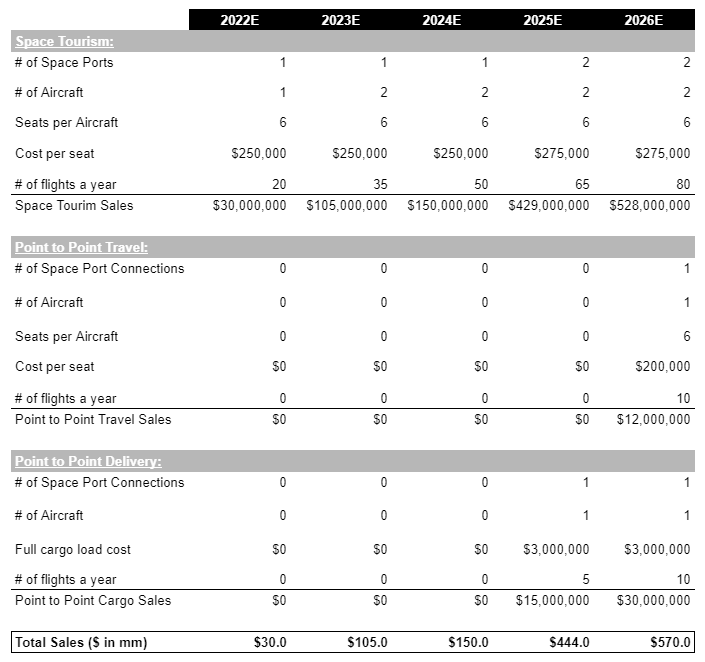

For my own model, I factored in three areas of revenue that I mentioned previously: space tourism, point-to-point travel of cargo, and also people.

Obviously, space tourism is the quickest way the company’s timeline to make money and I followed suit with P2P for cargo and then people.

To be completely frank, I have no idea how much the company would charge for a ticket for P2P travel or what a full payload would cost to transport cargo, so those prices are purely hypothetical.

Considering that they are charging $250,000 per ticket for a human ($1.5m per full flight), then a cargo load of double that ($3m) is not that farfetched.

Even with these numbers starting in 2022, factoring the number of flights that grow over time that aren’t affected by weather or any other issues bridges me to just $444m in 2025 compared to a consensus of $550m.

Virgin Galactic has 240m shares outstanding, of which 164.6m are available to the public for trading – which is known as float. Based on Friday’s closing price of $49.20, Virgin’s $500m offering would equate to nearly 10.2m shares.

Factoring in fully diluted share estimates after their $500M stock offering ~250m shares, at a more than a generous forward multiple of 200x and 2022E sales of $30m (13.5x 2025E sales), gets you a price per share of $24.00, best case scenario.

Even high-growth tech companies that have 20-30% CAGRs (pre-covid) don’t have forward P/S multiples like that.

Airbnb ABNB 0.00%↑ - 15.8x

Uber UBER 0.00%↑ - 8.6x

Lyft LYFT 0.00%↑ - 8.3x

Doximity DOCS 0.00%↑ - 38.8x

DoorDash DASH 0.00%↑ - 16.3x

200x is more than generous, frankly stupid, given TAM and the fact that this is a capital-intensive business and is a more high-risk industry than traditional transportation sectors like airlines.

Conclusion

Virgin Galactic is a really exciting company to follow and be a part of. I was a strong proponent of it when it first IPO’d and then again during the COVID-19 crash in March of 2020.

Though I am ambitious about their growth prospects and what they’re trying to achieve, the stock is more than priced in for all its revenue in the next six years.

Retail investors seem to be the one’s carrying the stock at this moment and with some dabbling from the WSBs community, the stock can easily go higher but eventually, reality has to set in.

*The current stock price at the time of this article: $30.20.