SMG: Earnings Support LONG Thesis

After SMG reported better than expected earnings last week, things are looking up

Quick thesis recap

If you’re just following along for the first time, I recommend you read my original post of Scotts Miracle-Gro (SMG: Buy two, get one free) where I speak about things in-depth. If you prefer not to, I highlight the key points of my LONG thesis below.

The company saw a stellar pull forward of its sales during COVID and thus an increase in their stock price - analysts assumptions of a steep slow down in a post COVID world were overblown

Hawthorne, its hydroponics business, is the fastest-growing segment of their business and I don’t believe that the street has fully grasped the full potential value this business has for future growth

At the time of writing my original post, I believed that SMGs core business (excluding Hawthorne) was valued at the then trading price and you would be getting their hydroponics business basically for free

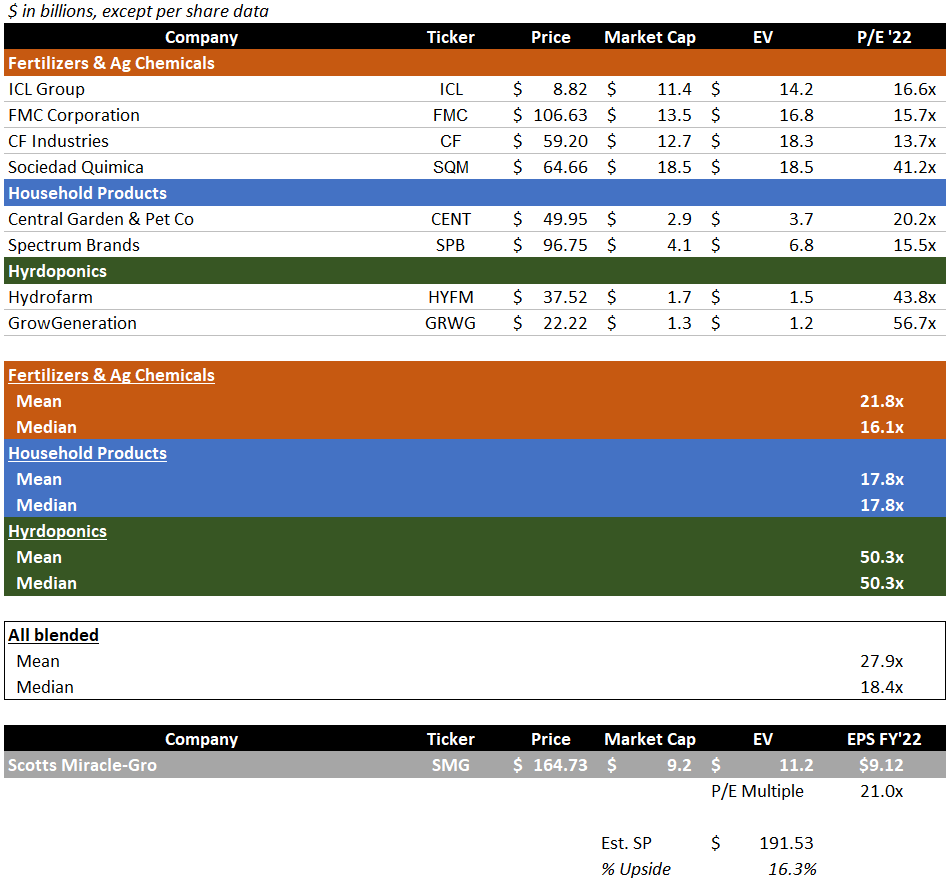

I valued the overall business via a sum of the parts (SOTP) value methodology and came to the estimated share price of $195 or a +32% upside

Additionally, and not a good reason but, before their earnings print last week, the stock was trading within 10% of the price it was before we all went into COVID lockdown. This made no sense to me given the progress that the company has made in over a year and a half as if nothing even happened.

I briefly touch base on their earnings and forward guidance before I give my thoughts on my valuation after this earnings release.

Earnings recap

The biggest takeaway that I want you to go in with when reading all the subsequent information is that the last quarter of their fiscal 2021 year was not as bad as everyone thought it was going to be. This includes management that gave the ultra-conservative forecast in the first place.

So, what transpired?

SMG reported a loss from continuing operations of $48.7 million or 87 cents per share in fourth-quarter fiscal 2021 (ended Sep 30, 2021) compared with a profit of $4.2 million or 7 cents per share in the year-ago quarter.

Barring one-time items, adjusted loss was 82 cents per share against earnings of 6 cents a year ago.

Net sales went down 17.1% YoY to $737.8 million and beat the consensus mark of $695.4 million.

This is actually important because management was guiding for a heavier drop in Q4 than expected. Management guided for a 45% drop in its US Consumer category and a 16% increase in its Hawthorne unit to end the year with 7-9% growth in US Consumer and 40-45% growth for Hawthorne.

What actually happened was that US Consumer only dropped 25.7% and Hawthorne dropped 6.5% bringing the full-year growth figures to 12.2% and 34.9%, respectively.

This was surprising news since the US consumer business makes up 65% of the company's sales and that’s what pushed the stock up ~10% after the print.

Forward guidance

Scott’s gave guidance for fiscal 2022 that includes non-GAAP adjusted earnings of $8.50 to $8.90 per share on company-wide sales growth of 0 to 3%. The company said that this increase will be helped by a second pricing action in the U.S. Consumer segment to mitigate commodity inflation.

“As we look to fiscal 2022, we have continued confidence in our strategy and ability to drive long-term shareholder value. Certain macro issues beyond our control may present challenges we haven’t faced for a while, but I’m confident in our team’s ability to execute. We expect to continue pursuing acquisition opportunities throughout the year and remain committed to using our financial flexibility to return cash to shareholders. That is why, in addition to the $113 million of share repurchases in fiscal ’21, we plan to repurchase as much as another $300 million in 2022.” - James S. Hagedorn, CEO

Hawthorne sales are expected to grow approximately 8 to 12% with most of the growth expected in the second half of the year.

“At Hawthorne, we expect the current over-supply of cannabis to put negative pressure on our growth rate through the rest of the calendar year and into the second quarter, at which point we anticipate a more normal growth rate,” - Cory Miller, CFO

What does this mean for valuation?

Inflationary pressure

There is one thing that made me change my FY’22 PT that came from management which was that they expect to see higher costs due to inflation.

"Commodity prices were a headwind throughout fiscal '21. We have communicated to our retail partners that we will take additional pricing actions effective in January as we continue to battle higher costs from urea, resin, grass seed and other commodities." - Cory Miller, CFO

Because of this, management expects gross margin to decline by 100 to 150 basis points (1-1.5%), and SG&A in a range of minus -6% to +1%. Interest expense is expected to increase by approximately $25 million.

My new assumptions

Based on management sales guidance and the impact on gross margin, I’ve included my assumptions below along with my valuation.

Overall sales growth of 6.6% with its US Consumer segment growing 4%, Hawthorne growing 12%, and its other segment growing 7%.

Gross margins at 28.4% (realizing the full 1.5% decline), SG&A at 14.8% (down from 15.1%), and EBIT margin of 13.7% (down from 14.8%).

After modeling this out, I came to the FY’22 EPS target of $9.12. This is in comparison to the mean EPS estimate of $8.70 given by management.

Last post I valued SMG on EV/Sales which historically is not how SMG is typically valued. Because it does have positive earnings, P/E is the better way to portray things and that’s what I’ve decided to use in my updated figures.

With FY’22 EPS at $9.12, and factoring in a fair 21x forward P/E multiple and you arrive at a PT of ~$192 vs my original of $195, representing an additional upside of +16%.

Given how the stock is already up 13.7% since I wrote my post, an additional 16% relative gain would represent an absolute gain of +32%.

Given the volatility in the markets these days, I’m happy to hold SMG in my portfolio and look forward to seeing what the coming quarters bring in terms of return. Keep in mind though that SMG is a seasonal business (winter no bueno for lawn care) so do be shocked about slimmer figures during the winter months, this is expected.

Disclaimer: I do currently have a position in Scotts Miracle-Gro SMG 0.00%↑ at the time of this post being published. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from the Substack subscription). I have no business relationship with any company whose stock is mentioned in this article.

One last thing!

Please be sure to follow my Twitter @paulcerro to stay updated with commentary around positions and other miscellaneous news that might not be in-depth enough to warrant a newsletter post.