💰 Robinhood Not Worth the Coin

Why the hottest trading platform of 2020 is more expensive than what it's presumably worth

Summary

Robinhood has become a household name but for many wrong reasons attracting lawmakers and politicians to paint a target on its back

With its current business model under threat and a large reliance on crypto trading volume, the company is quite exposed to the downside

The average retail investor has mixed feelings towards the company and with referrals making up 80% of new organic users, word of mouth can make or break Robinhoods growth

Business Overview

Robinhood HOOD 0.00%↑ set out on a quest to democratize finance and give the power back to the little guy. They pioneered the brokerage world by offering zero-commission stock trading which inevitably pushed incumbents like Fidelity, Charles Schwab, and E-Trade to follow suit.

Its sleek, game-like design helped lure in many first-time investors making them the preferred choice to open their very first brokerage account.

It was a well-laid-out app that made investing super easy, maybe a little too easy.

Since its founding in 2013 up until the end of 2020, the platform has added 13 million users. It added another 6 million users in the first two months of 2021.

Weekly downloads from U.S. app stores surged in the first half of 2020, making it the fourth most downloaded finance app, according to Sensor Tower—the first time it cracked the top 10.

According to the market news site Business of Apps, the average account size is about $3,500, compared to $100,000 for E-Trade and $240,000 for Schwab. This can more or less put into perspective who Robinhood is catering to if you didn’t already know.

In a regulatory filing that gave the first look at its financial performance, Robinhood said revenues more than tripled to $959m last year, up from $278m in 2019, and its explosive growth continued in the first quarter of this year.

For the year ended Dec. 31, 2020, Robinhood reported a profit of $7.1 million, compared with a loss of $106.6 million in 2019.

The platform has more than doubled its registered users since the start of 2021 to 31m. Of these, 18m were funded accounts at the end of the first quarter, up 151% from the end of 2020. It had revenue of $522m in the first three months of the year, a 309% increase from the same period the year before.

The company had $1.4 billion in losses for the March 31 quarter, up from $52.5 million in losses for the same period in 2020. Most of the first-quarter losses were a result of a write-off from a change in the fair value of convertible notes and warrants after a $3.4 billion fundraising in February.

With all this success, the company is riddled with red flags that would make me skeptical that the company is worth $30bn. The juice is just not worth the squeeze, at least not at these levels.

Investment Thesis - SHORT

Ever since the start of the pandemic, Robinhood has become almost a household name and synonymous with the average investor sticking it to the traditional Wall Street hedge funds (queue a Gamestop meme).

However, with all its recent success and hyper-growth, I believe that the company is not worth the estimated $30bn it plans to achieve in the public markets and I would be hesitant to bet on its long-term potential given how some walls are closing in on them.

Below I’ve outlined why I believe Robinhood makes for a SHORT position at elevated valuation levels, north of $30bn.

Hyper-growth was temporary and not sustainable

We all know what happened in 2020. We were home long enough to not have really missed anything that happened in the outside world that directly affected our ability to return to normalcy.

To sum it up, in a few words, people stayed home. They didn’t spend money because they really couldn’t. People got bored. They decided to put their money in the stock market, and the rest is history.

Let’s revisit the numbers quickly:

18m funded accounts as of March 31, up from 12.5m at end of 2020 and 5.1m as of 2019

$522m in revenue for the first quarter of 2021 compared to $128m YoY

$959m in sales in 2020, up from $278m in 2019

$80.9bn in customer assets as of March 31

If you’re looking at it with a quick glance, this company is firing on all cylinders. However, there’s more to the story than just what the data shows. Like I mentioned at the beginning of this section, a Black Swan event happened last year in case you weren’t aware.

Millions of Americans poured their money into the stock market to occupy their time and to capitalize on a once-in-a-decade event that effectively drops the market so much that you can hop in and go along for the ride upwards. If you had money on the sidelines ready to use, 2020 was possibly the year that either changed your life financially or wish that it did.

According to Bloomberg Intelligence via The Wall Street Journal, individual investors made up an estimated 19.5% of U.S. equity trading volume. This was a jump of over 4% compared to 2019 and a doubling compared to 2010.

Overall, this is a positive development as, anecdotally, it appears that many of the new investors entering the market are younger and have the advantage of time on their side. With the ease of opening a new account and the ability to invest with only a smartphone, the barriers to getting started are lower than ever before.

Robinhood was quick to capitalize on this with its marketing, mobile app, and easy-to-use interface. According to the company’s S-1, over 50% of Robinhood customers are first-time investors.

These two facts (staying home and not being able to spend money + being bored) coupled with 3 separate stimulus checks from the federal government equating to a couple of thousand dollars (if you qualified) set the stage for why the company was able to do so well with new retail investors.

What we’ve all been waiting for, however, is when can we get back to our everyday lives. This is what commentators have called, “the grand reopening.” This is when establishments such as gyms, restaurants, clubs, travel, etc. all open back up and we can start living again. In essence, spend the money that we’ve been hoarding this whole time.

Given that consumer spending accounts for almost 70% of the U.S. economy, keeping it in your savings just isn’t going to cut it. Also, let’s be real, we’ve been dying to get back out there and start living.

Another point to all this is, 2020 was an easy way to make money in the stock market. You could throw darts at a dartboard in the dark and still hit winners. Many new investors didn’t know what it was like to lose and go through a time where volatility can bite you every other day. With 2021 not being so easy, I imagine many might be throwing in the towel or just reducing their trading activity.

Their dependence on crypto isn’t a good one

Ever heard of this thing called Bitcoin? Perhaps Dogecoin? Well, they’re all cryptocurrencies and they’ve made normal people become millionaires overnight.

At its peak, BTC was up over 100% for the year and dogecoin rallied over 4,500%! Wild numbers considering dogecoin was trading for a fraction of a penny in Jan.

With the hype around cryptocurrencies, many retail investors dove headfirst into any project that they thought could make them a quick buck overnight. Names like cumrocket, tittycoin, and boobcoin. Literally stupid things that people threw money at because of “hype” culture.

This asset class was also fueled by some legitimate reasons like more institutional investors dabbling in it, more merchants accepting it as payment but none more than the Dogefather himself, Elon Musk.

This guy could move markets with a single tweet without even naming the crypto.

Cryptocurrency Price Over Time - Bloomberg")

Investing in a stock/asset that has the ability to move +/-10% based on a tweet makes sense. I believe Warren Buffet approved of this in one of his shareholder letters.

Millions of people invested in bitcoin because of how Elon was pumping it up, even announcing that Tesla would accept it as a form of payment only to revoke it weeks later.

The best was when after he made the claim that dogecoin was the currency of the people, he announced that he would host SNL. Millions tuned in to hear him drive up the asset higher only to see it crash after he called it a hustle.

To tie this into Robinhood, in the first quarter, crypto trading accounted for 17% of the company’s revenue, up from 3% in 2020. Crypto also makes up 14% of the company’s assets under custody. Because cryptocurrencies are so volatile, companies that depend on them for even a small fraction of their revenue sometimes trade in tandem with popular coins like Bitcoin and Dogecoin. In fact, Dogecoin accounted for 34% of the company’s crypto transaction revenue in the first quarter.

Robinhood’s increasing reliance on crypto could help it when the industry is hot, but cause sharp swings to the downside.

I mentioned this as a risk in my Coinbase article COIN 0.00%↑ too, however, the circumstances are different.

Even if you were to drop crypto revenue as a percent from currently 17% to 10%, you’re still talking about a ~$40 - $70m hit to revenue for the next quarter.

This ties into the hypergrowth issue I mentioned above but specifically to this particular asset class. Either way, I would not be betting on Robinhood to keep this growth up especially when other crypto exchanges like Binance and Coinbase are quickly expanding the number of assets they host, on top of a slew of other product releases related to crypto.

With BTC trading in the mid $30k level (down from over $60k) and Dogecoin trying to find footing at $.20 (down from ~$.70), many people have been burned and might be sitting on the sidelines until more momentum can entice them to jump back in. Whenever that is.

Robinhood users are PISSED

Remember the meme craze back in January when a stock such as GME went from a few bucks a share to touching $500 mid-month?

Yea well because of actual business liquidity issues, Robinhood restricted its customers from selling GME and only allowed them to buy. You can imagine how angry people were when they would see their account values skyrocket only to not be able to execute a trade that would lock in profits.

Needless to say, users were not happy with this. What’s funny is that Robinhood wasn’t the only one to restrict trading to some degree. Other major brokerages slowed down orders or temporarily restricted selling. Robinhood just happened to be the one that took the most heat from it.

Many Redditors took to comment how they were able to quickly transfer money to other brokerages like Fidelity and Merrill to continue trading. This spat with trading restrictions left a bad taste in customers’ mouths and Robinhood with a dented reputation, especially after they are the ones that are supposed to be for the little guy.

Word of mouth is a powerful tool, and according to the company’s S-1, over 80% of new customers that join organically come from their referral program. This helps with overall payback when you talk about customer acquisition costs but now imagine millions of angry Robinhood users vocally telling their friends to use something else.

Churned accounts (those that have closed) as a percent of the number of accounts at the beginning of the most recent quarter, increased to 4.8% compared to 2% YoY.

I’ll be curious to see what the second quarter rates look like after all the recent volatility in the crypto and equity markets. Signs point to not being that good.

Regulators have a target on Robinhood’s back

It’s a widely known fact that the Democratic party is not the biggest fan of Wall Street. They feel that banks and other institutions are greedy and only look out for themselves when it comes to making a buck while putting the little guy at risk.

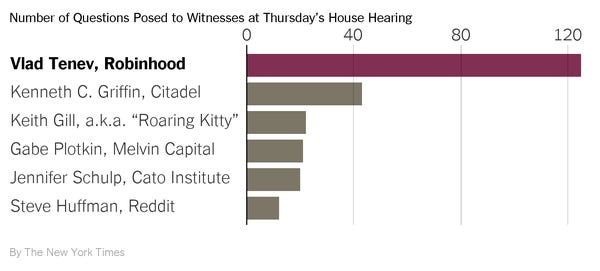

This has become front and center during the meme stock blowup earlier this year when the CEO of Robinhood had to go before Congress to explain what happened that made them restrict users from selling their shares, effectively leaving the small guy out to dry as their accounts plummeted.

During the Congress hearing related to the debacle, CEO Vlad Tenev definitely was on the chopping block more than others when it came to questions.

Vlad apologized for his company’s failings — without specifying which mistakes were made — but said his company broke no laws and didn’t prioritize Wall Street business partners over retail users. “We don’t answer to hedge funds,” he said.

Simple response but that hasn’t stopped politicians from continuing to put pressure on the company.

Current business model under threat

There are a few ways that Robinhood makes money.

Transaction-based revenues (PFOF) - which means it gets paid by market-makers who execute orders for Robinhood customers and take a cut of the spread between the bid and ask prices.

Interest revenue - this is in regards to lending out money to users on margin (more on this later)

Other revenue - primarily monthly paid subscriptions like Robinhood Gold, proxy rebates, and misc charges.

The one that I want to focus on is the Payment for Order Flow (PFOF) and the regulation of it, which they actually label as a risk in their S-1.

In essence, Robinhood takes your trade data and sells it to hedge funds and other high-frequency traders so that they can capitalize on price information. This is the exact reason why Robinhood was able to pioneer the zero-commission trading initiative in the first place.

No longer needing to pay a fee on stock transactions and empowered by easy-to-use trading apps like Robinhood, individual investors poured into stocks and options at record levels last year.

Payment for order flow critics—including the country’s top market regulator, Securities and Exchange Commission Chairman Gary Gensler —are wary of the practice. They argue that it poses a conflict of interest for brokerages because the brokers can either collect more money for selling their customers’ order flow or pass that money on to customers in the form of price savings on their trades.

Still, the SEC hasn’t given any indication of how it might change its rules on payment for order flow. Prohibiting PFOF might force some brokerages to abandon zero-commission trading, which could lead to an outcry as small investors face the prospect of paying for trades again. That would undermine arguments that banning PFOF would help investors. Many of the potential benefits of such a change—such as possibly increased activity on transparent public exchanges—wouldn’t be as tangible to ordinary investors.

Either way, should regulation come down that PFOF is null and void, that will severely capitulate Robinhood’s prospects of maintaining any sort of growth-based valuation.

Gamified interface creating casino like circumstances

Let’s be honest, the Robinhood app is super sleek, modern, easy to use and understand, which has allowed them to attract many first-time investors onto the platform. I have an account with Charles Schwab and Robinhood (just for options) and the Schwab platform/app I would label as an old-school ‘big boy’ account.

The problem with how Robinhood has made its user interface/experience is that it basically makes the app feel like more of a casino than a trading platform.

Several lawmakers have also criticized the Robinhood app’s so-called “gamification” approach, where trades are celebrated with virtual confetti and made to feel more fun. “You are encouraging your customers to tap 1,000 times a day,” said Ritchie Torres, Democrat of New York. They have since rectified this and no longer have this function.

Even Charlie Munger, Warren Buffet’s partner at Berkshire said in a recent annual meeting…

“Well, it’s most egregious in the momentum trading by novice investors lured in by new types of brokerage operations like Robinhood. I think all of this activity is regrettable. I think civilization would do better without it.”

When you treat something as if it’s a game, specifically involving money, people can become hooked and essentially addicted to it.

Scott Galloway, Professor of Marketing at NYU Stern, outlined this in his newsletter “No Mercy/No Malice” last week when it came to Robinhood and gaming addiction.

Robinhood, on the other hand, is the Sith Lord of finance — monetizing the addictive nature of day trading. Day trading is gambling. And it doesn’t pay off. I wrote about this a year ago, when a 20-year-old Robinhood customer killed himself after the app mistakenly suggested he was down $730,000.

Capitalizing on an investment boom through gamification, essentially creating an addiction, will not sit well with regulators and I believe that continued scrutiny and pressure will keep Robinhood in check and slow down product releases.

Enticing its users to use risky methods for more reward

Piggybacking on what I mentioned above, part of how Robinhood makes money is through interest generated from margin accounts.

Margin accounts, using leverage (borrowed money) can significantly increase your returns on a trade or leave you in the hole. It’s something to take seriously though many first-time users do not understand the repercussions.

In a margin account, Robinhood charges a measly 2.5% on anything above $1,000. This is pocket change considering Schwab charges me 8% on anything under 25k and then has a progressive rate depending on the amount borrowed and assets in my account.

The Financial Industry Regulatory Authority (FINRA), a government-authorized regulator of brokerage firms, mandates that investors deposit at least $2,000 before trading on margin.

What ties into this is that a lot of first-time investors were hammered with so many stories of how people got rich quickly in options trading and using margin that they wanted to replicate it for themselves. Half of Robinhood’s revenue in 2020 came from options trading, which is also receiving more scrutiny from regulators because of its inherent risks.

While Robinhood has offered options trading since December 2017, FINRA says it has

“failed to exercise due diligence before approving customers to place options trades,” relying on algorithms, rather than people, to approve customers for the risky investing move.

As a result, Robinhood approved thousands of customers for options trading who either did not satisfy the firm’s eligibility criteria or whose accounts contained red flags indicating that options trading may not have been appropriate for them.”

Some issues with that business (margin lending) attracted the attention of CBS MoneyWatch, which found that investors who borrowed money from Robinhood were nearly 14 times as likely to be unable to repay those loans when compared to other brokerages.

Playing with fire can leave you burned and honestly, the Wall Street Bets forum is filled with fallen young “investors” that YOLO’d their savings on margin.

This is just one of many but the platform has not made much effort to curb the uneducated from taking on massive risks.

They have introduced educational material so that new investors can learn before they act on risky trades but making access to capital that much easier and affordable doesn’t really keep many from saying no.

Meat and Potatoes (Valuation)

So I’ve spoken so far about all the issues that I believe prevent what some have labeled as a $40bn company after the IPO. First of all, I want to say that I think there is no way that Robinhood is worth $30bn let alone $40bn.

Let’s start with a simple proxy for valuation as a baseline. Given Robinhood reported first-quarter sales of $522M, a jump of 309% YoY, this implies a run-rate of $2.1bn by year-end. To get to a $30bn valuation, that implies a 14.2x fwd sales multiple.

Coinbase, which had sales of $1.6bn in the first quarter and a growth rate of 845% currently trades at 8.1x fwd sales ($6.3bn for the year). I will give it the benefit of the doubt though that at IPO, Coinbase hit an intraday high of $429 a share putting it over $90bn for a brief minute before it descended into what it is today, giving it a multiple of 15.9x. However, as this is history, Coinbase dropped all the way down to $208 a share effectively cutting its valuation by more than half.

The reason I want to use Coinbase as the closest competitor is for a number of reasons.

High growth fintech startup that offers multiple financial products

Deals in cryptocurrency

Heavily utilized by the younger, first-time investor

Recently gone public during a very volatile market

Being closely monitored by regulators, minus the target on its back

To help you understand where I’m coming from, let’s play with the numbers for a second. $2bn in annual run-rate revenue as it stands. That’s about a 119% jump from 2020 revenue.

However, this is not the full story, and haircuts to this run-rate revenue will need to take place.

Robinhood also said it anticipates the growth rate of new clients will be lower in the third quarter of 2021, compared to the second quarter. Apply a haircut of 5% to run-rate revenue for the slow down in user growth on the platform which the company recently admitted to for the 3rd quarter.

“due to the exceptionally strong interest in trading, particularly in cryptocurrencies, we experienced in the three months ended June 30, 2021 and seasonality in overall trading activities”

Another point to warrant a revenue haircut is a report that came out stating that crypto trading volume plummeted in the month of June. Given 17% of revenue came from crypto trading in Q1, this further suggests that growth at these levels is not sustainable.

Now we’re at $2.0bn in revenue. Apply a second haircut of 5% because of reduced trading activity in equities and crypto due to fear of losing money during this market volatility and retail investors using their cash to take part in living life again.

“We expect our revenue for the three months ending September 30, 2021, to be lower, as compared to the three months ended June 30, 2021, as a result of decreased levels of trading activity relative to the record highs in trading activity, particularly in cryptocurrencies, during the three months ended June 30, 2021, and expected seasonality,”

Now we’re at $1.9bn in revenue.

Using the middle of the range of where Coinbase peaked after the IPO and where it’s trading at now (8.1x and 15.9x) gets you 11.7x. Applying this to the new sales figure of $1.9bn and you get a valuation of ~$22bn and change. Far less than the $30bn - $40bn.

Conclusion

I think Robinhood is a great company that definitely is going through growing pains in numerous categories but the hype going around that people are making it seem worth over $30bn is just ludicrous.

I would stay away from taking a long position in this company and labeling it a SHORT recommendation. Too much inherent risk with growth prospects and I’d rather not be in a company going through 49 class action lawsuits and congressional hearings.

Since I’m sending this article out prior to it going public, I have no reference point for the price but will announce it on my Twitter for accountability when I do. If I feel the price is north of the $30bn, I would highly consider shorting it. By the sound of it, it looks like it will price around the $35bn range.