My first short idea: Chewy, Inc (CHWY)

Why this howling pet company will be losing steam in a post-pandemic world

Summary

Despite significant outperformance during the COVID-19 pandemic and the rapid adoption of online pet food & supplies shopping, Chewy, Inc CHWY 0.00%↑ ceases to remain a compelling investment at the current valuation

Though management has successfully capitalized on the massive shift to e-commerce for pets during the pandemic, multiple fast approaching headwinds such as:

Competitors expanding their respective market penetration within the pet space leading to higher customer acquisition costs and reduced growth expectations

Lack of a “secret sauce” that would provide a defensive moat against oncoming competitors

Failing to expand into new opportunistic business areas that would continue to convince investors to pay for a rich EV/EBITDA multiple

I believe that future growth been priced in at the current levels. Additionally, looking ahead, I anticipate that strong headwinds will lead to further downside in the overall equity value of the company as part of a valuation reset.

Assuming $8.9B in sales for FY22 (FYE Jan. 2022) and a 3x P/S multiple, I believe the stock price is currently worth $65 a share, or a ~22% downside.

Business Overview

Chewy, Inc., together with its subsidiaries, engages in the pure-play e-commerce business in the United States. The company provides pet food and treats, pet supplies and pet medications, and other pet-health products, as well as pet services for dogs, cats, fish, birds, small pets, horses, and reptiles through its chewy.com retail Website, as well as its mobile applications. It offers approximately 70,000 products from 2,500 partner brands. Chewy is also a subsidiary of PetSmart, Inc., which still has a minority stake in the company.

Investment Thesis

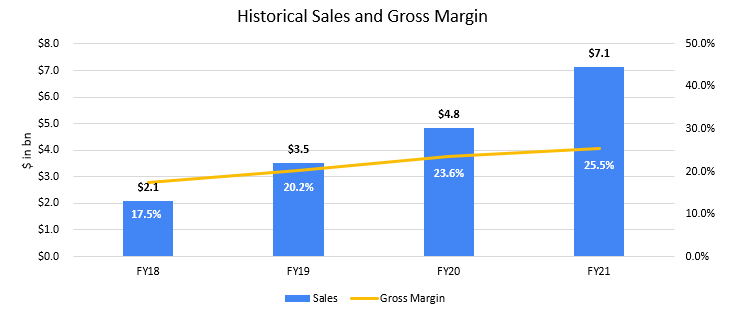

Because various retailers were so focused on providing household essentials like food and cleaning supplies last year during the pandemic, Chewy was able to capitalize on them diverting their attention away from the lucrative pet category and increased their overall sales by +47.4% for 2020.

That’s pretty impressive for a company when many other retailers were struggling, though one interesting point about the pet industry is that it’s pretty recession-proof. What do I mean by this? Think about it, when you have a pet and you go through an economic downturn, you’re sure going to be cutting back on going out to eat but certainly not providing for your living breathing pet.

For example, during the recession from 2008 to 2010, overall consumer spending in the U.S. declined while pet spending in the U.S. increased by 12%, according to the APPA. In 2010 alone, spending in the U.S. on entertainment decreased by 7.0%, food decreased by 3.8%, housing decreased by 2.0% and apparel and services decreased by 1.4%, according to the U.S. Bureau of Labor Statistics, while spending on pets increased by 6.2%, according to the APPA.

So if you’re interested in recession-proof stocks, the pet industry surely falls into that category, however, my prediction is that this freak growth story due to a Black Swan event will not last.

*For those of you who need a refresher on the pet industry, take a look at my other article where I go LONG on Petco.*

Competition, Competition, Competition

It’s safe to assume that there are many players in the pet space, maybe not from a pure-play perspective but who at least have a significant amount of pet products they sell.

Companies such as Amazon AMZN 0.00%↑, Target TGT 0.00%↑, Walmart WMT 0.00%↑, Petsmart, Petco WOOF 0.00%↑, and thousands of other brands and smaller retail stores.

As of last year, there is still a large number of people that shop at other locations than just Chewy. 60% of a Statista survey showed that respondents shopped at Amazon alone.

Competitors, realizing the market opportunity for pets, will utilize their current retail ecosystem, supply chain, and delivery logistics to penetrate further into the pet category.

As we are all familiar with, as soon as Amazon catches a whiff that something can be a big market for them, they usually launch that business segment on their own. Petco is increasing its online presence and so is Petsmart. It won’t be long until the other retailers follow suit like Target with their Shipt services.

Other pet-related companies entering the market either encroach on Chewy’s existing business or are establishing a foothold into other high TAM areas. For instance, there’s Bark Box for pet toy and treat subscription box, Figo/Petplan for insurance, Rover/Wag for dog sitting and walking, The Farmers Dog for fresh DTC pet food, and many others.

With so many other companies coming online in the pet space, Chewy’s first mover advantage that they’ve had since 2010 is under siege and will be attacked from all sides.

Increased online competition and a return to shopping in-store post-pandemic will lead to increased customer acquisition costs and overall advertising and marketing spend to maintain top-line growth momentum. This is in part why I believe growth will slow down and an increase in marketing expense will occur in an effort to win more customers putting downward pressure on operating margins.

Lack of a Defensible Moat to Fend Off Lurking Competitors

Shipping pet supplies online is nothing new

Let’s be honest, nothing about Chewy’s business proposition is proprietary or hard to implement, generating no “stickiness” or encompassing an ecosystem to keep customers loyal. It’s simply replicable to anyone else that wants to get in the business. Selling pet supplies online isn’t rocket science.

Chewy is just more of a well-known DTC pet supplier but that doesn’t make it a better value-add one. The company touts having over 75,000 products on its website, however, Amazon has over 60,000 with over 50,000 of them being available via Prime. Given that there are 200mm, Prime subscribers, having access to over 50,000 products represents a huge portion of the United States population.

Recurring revenue is becoming the new normal

Their auto-ship service has been growing rapidly, representing 68% of total sales in FY 2021, down from 69% in FY 2020. This, however, is not revolutionary either. Amazon, Petsmart, Petco, and many other retailers offer this service to grow consistent recurring revenue and keep customers on their platform. Petco in their filings has stated that their repeat delivery service increased 13% in fiscal 2019 and 43% in fiscal 2020.

Chewy’s delivery logistics are fast, but not fast enough

Chewy boasts their 1–3 day shipping timeframe though with over 50k pet items on Prime and Petco/Petsmart have partnered with Door Dash for same-day delivery to leverage their retail network as fulfillment centers put them at an unfair advantage against Chewy’s current delivery model.

Over 70% of Americans mostly buy pet

Not focusing on expanding into other revenue-generating businesses to sustain current growth rate

Chewy only operates in two lines of business:

DTC e-commerce of pet food, supplies, and medication

Virtual clinic

Chewy’s foray into pet health with “Connect with a Vet” is what seems to be a great money-making idea, at least on the surface, however, it is free to auto-ship customers which make up almost 70% of all sales. Not only will this not generate revenue, but the real kicker is also that it cannot diagnose or prescribe medication at all. The main purpose of this offering is just for veterinarians to give recommendations for pet owners quickly, should the need arise.

For instance, your dog eats a whole box of pizza and you’re wondering what the repercussions are. The vet would give them their two cents and you’d be on your merry way. Not much in the sense of growing into a revenue-generating business. This is why I believe this entire endeavor, in its current form, should be dismissed entirely when it comes to being priced into the stock.

Just to paint you a picture of what I mean by diversification of revenue-generating businesses. Petco has made significant investments in its digital app, e-commerce platform, in-store services, lucrative pet health category via its vet clinics and hospitals, and expanded its delivery logistics to build an enclosed ecosystem to increase customer retention but also to create multiple avenues of growth besides just traditional food and supplies.

Key Risks/Considerations

Recently increased online consumer buying habits shift back to pre-Covid in-store levels

Chewy has built a business on getting everyday pet food and supplies to customers doors fast, however, with increased vaccinations and a hopeful return to normalcy, consumers might opt for shopping back in-store rather than online

Headwinds from retailers not focusing on the pet space during COVID will slow market penetration going forward

Part of Chewy’s success in 2020 was the fact that competitors were more focused on getting everyday food and household supplies in the hands of consumers to ride out this pandemic safely

This allowed Chewy to go full steam ahead and grow in an area that others overlooked for the time being

Once other companies realize the opportunity they neglected, an all-out customer acquisition war will commence and the winner with the most value proposition offering will claim the crown

Successful customer acquisition methods during COVID-19 may not prove fruitful in a post-pandemic world

Vying for additional sales per customer, Chewy might have to deploy more dollars towards advertising and marketing to sustain the same level of growth from the prior year

Competitors continue focusing on expanding larger e-commerce TAM categories

Grocery delivery/curbside pickup, one of the biggest TAMs, has grown exponentially during the pandemic and will continue to do so going forward

Model Summary

Valuation

Trading at ~225x FY22 EV/Adj. EBITDA, the company is well above comparable high growth consumer-focused companies which trade at ~28x.

On an absolute basis, 225x is an unrealistic multiple to be sustained without having years of future growth already priced into the stock.

Chewy must bring in over $1.6Bin revenue to break even on an adjusted EBITDA basis when Bark Box can provide positive adjusted EBITDA on just $221M in sales.

Unclear whether 10% EBITDA margins are achievable given customer acquisition costs will increase and CHWY will have to step up advertising and marketing spend.

Conclusion

Chewy has done remarkably well during the pandemic and sped up 3-4 years of growth and adoption in just 2020 alone. Though this growth is impressive, I would definitely chalk it up as a fluke and that growth will slow down once others feel more comfortable shopping in-store again or realize they can get their products delivered same-day.

What I do want to stress is that me labeling this as a SHORT recommendation does not mean I believe the business model or its management team is flawed or misguided. I think they have a stellar business model and management has proven they know what they’re doing. However, I think even post the company reaching all-time highs in February of $120 a share, it’s still too rich in valuation and I would personally hesitate to jump into the stock at current levels.

I look forward to seeing where the stock goes next and if I’m right, a nice additional pullback of 15-20% in the stock would make it more attractive.

*The current stock price at the time of this article: $84.04.