Market Ignores CPRI Divestment; An Opportunity For New Investors

Why we still think CPRI shareholders can make an outsized return from selling Versace

Students can get access to our research at a reduced rate by clicking here. If you’re interested in using Koyfin (I highly recommend it), you can get 20% off your plan using my link here.

Interested in becoming an LP? Click here to fill out the contact form.

Trade Update

If you’ve been following us this year, we’ve sent out a few updates regarding the potential Capri (CPRI) divestment trade of both Versace and Jimmy Choo. You can see our most recent note below, which we’ve removed the paywall to so you can see not only our math but the news that led to a higher conviction in the trade.

On Thursday, Capri (CPRI) formally announced that Prada (1913:HK) was acquiring Versace from the brand for $1.375 billion. This was a step down from the $2.1 billion it acquired it for back in 2018, but that’s not the important part here.

While it was a win for us on the situation, our original math did not anticipate tariffs taking effect, which suggested that the company should be trading well over $25/share once the deal was announced. However, it’s not a secret that Trump imposed reciprocal tariffs and went above and beyond that for China exclusively.

The day after his presser at the Rose Garden, CPRI went down by >30% and put the deal into peril. Despite the tariffs, the deal went through with a price reduction, though the price did not react the way we thought it would.

This leads us to believe that the current economic policies under Trump (tariffs on China + other SE Asian countries) are overshadowing what would have been a blow-off top for this stock.

Since the announcement, technically, CPRI is now running as a net-cash company (excluding operating leases), which is why we think holding the name to get the return deserved could be warranted.

Under normal divestment circumstances, we think that the net cash position of CPRI without a re-rating of the company should have led to a significant jump in the stock price after the announcement.

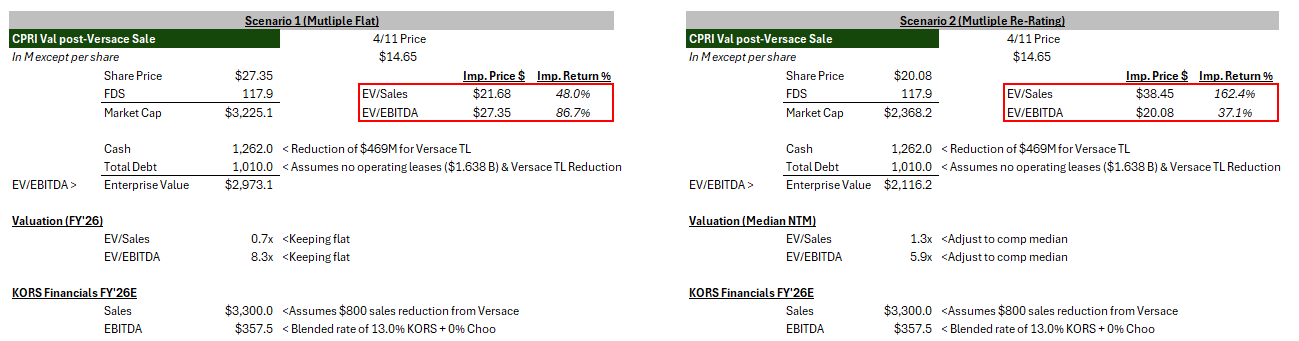

To understand what we mean, we've highlighted two scenarios where 1) there isn’t a multiple re-rating (mentioned above) and 2) one where there is, which would re-rate to the comps of its peers.

For FY’26 estimates, we’re using what CPRI gave for their LT financial targets.

Both of these scenarios result in a share price much higher than it is today, which, again, would be warranted under a normal situation. Granted, all of this is just Excel math, which doesn’t mean much when the global economy is up in the air and tariffs on China are at 145%, which completely kills anyone getting product from that country, so take it with a grain of salt.

However, the point here is to show that this stock should be worth more if it weren’t for that considering the newfound cash position is almost the entire current market cap of the company.

Per our last update in our Q1’25 letter, we expected it to at least trace back up to near $20/share as our base case or beyond that for the bull case.

Clearly it didn’t, but here’s why we’re still optimistic about that happening.

1) Tariffs For Now, But Not For Long

With the remaining business (KORS + CHOO), a sizeable amount is still made in China and other parts of Asia for Michael Kors, and mainly in Europe and some Asia countries for Jimmy Choo.

As we just mentioned, the 145% tariffs kill anything and everyone that gets product from there, which is why CPRI’s negative move on the announcement made sense. Not to mention that KORS and CHOO have just under ~15% of their sales in Asia, which has been ever so slightly tapering down since 2021.

But the tariffs are so extreme that eventually one side has to break, and we think it’s going to be Trump first. Despite him lowering reciprocal tariffs to just 10%, excluding certain countries, the effective tariff rate actually went UP from 26.8% to 27.0%.

There is just no way this works in any scenario. So we believe that Trump will fold soon on clothing and textiles, just like he did on Saturday with smartphones, computers, and other electronics, and when he does, the stock should rip higher like it did the day he announced the 90-day pause.

2) Bond Market Forcing Trump

The other reason we believe Trump will fold on the tariffs, besides the obvious, is that the Bessent and Trump have been trying their best to get the 10Y down as low as they can (without breaking anything) so they can refinance the US’s debt.

Trump’s policies are having the complete opposite effect, and the 10Y breaking through 4.5% the other day was really the reason he initiated the 90-day pause. However, that didn’t assure bond investors at the long end of the curve for that long.

10Y yields have continued to go up and completely blew past 4.5% today as if it were nothing before settling back down to just under that key level.

If the world continues to dump US treasuries and the basis trade continues to unwind, he’s going to be forced to pull back on this suicidal agenda of his, which further reinforces our point #1.

3) Net Cash And Various Options

Looking back at our math, even if they pay off the remaining balance of debt ($1.0 billion; $521 million Revolving Credit Facility, $450 million 364 Day TL, and other debt at $41 million), they’re still looking at a net-cash position of ~$250 million.

That’s if they used all of their cash to pay down debt, which I highly doubt they will. Though the bright side is that in their PR, they did mention that they could use the newfound cash for three things.

Business investments

Debt reduction

Future share repurchases

All of which are excellent ideas. So no matter how you cut it, the company has plenty of options to increase shareholder value with one, let alone all three of these areas of focus.

A good problem to have going into a tough environment ahead.

Wrapping Up

Do we like CPRI as just predominantly KORS and CHOO? No. We’re just in it for the trade, and while we got the trade right, the outcome was a different story, which we believe is suffering because of all the noise/implications coming from Trump’s tariff war.

We think that soon enough, either the economy (or enough CEOs) or the bond market will force Trump to wake up to the reality that his tariff plan is a terrible idea and reverse course. Once that happens, CPRI will be able to properly get the rating that it should be getting after selling off money-losing Versace and pop heavily on that news.

On top of it, because the company is now running at net cash, as long as they don’t incinerate capital, the options for CPRI to get back on track are abundant, and investors should be rewarded once negative market sentiment rolls over and again, gets repriced.

We’re still holding on to this trade for now, mainly because we just can’t see a world where the China tariffs stick for much longer.

The potential for a 25%+ move higher from these levels is quite enticing in our opinion.

As always, we appreciate your support of our work. To continue getting research such as the one you just read, consider signing up as a paid subscriber.

Until next time,

Paul Cerro | Cedar Grove Capital

Personal Twitter: @paulcerro

Fund Twitter: @cedargrovecm