M&A Arb: Betting Against Soho House (SHCO)

Why we speculate that the take private deal won't go through

Key Highlights

Company received a $9/share take-private offer a week before Christmas contingent on certain stakeholders rolling their equity.

One of the largest shareholders, Ron Burkle of Yacaipa Companies, is in favor of the deal happening.

This is not the first time an offer has come through with a ‘substantial premium’ and has been rejected.

Not confident that the other largest stakeholders want to be taken private and perhaps “lose control” of their ability to execute on strategy.

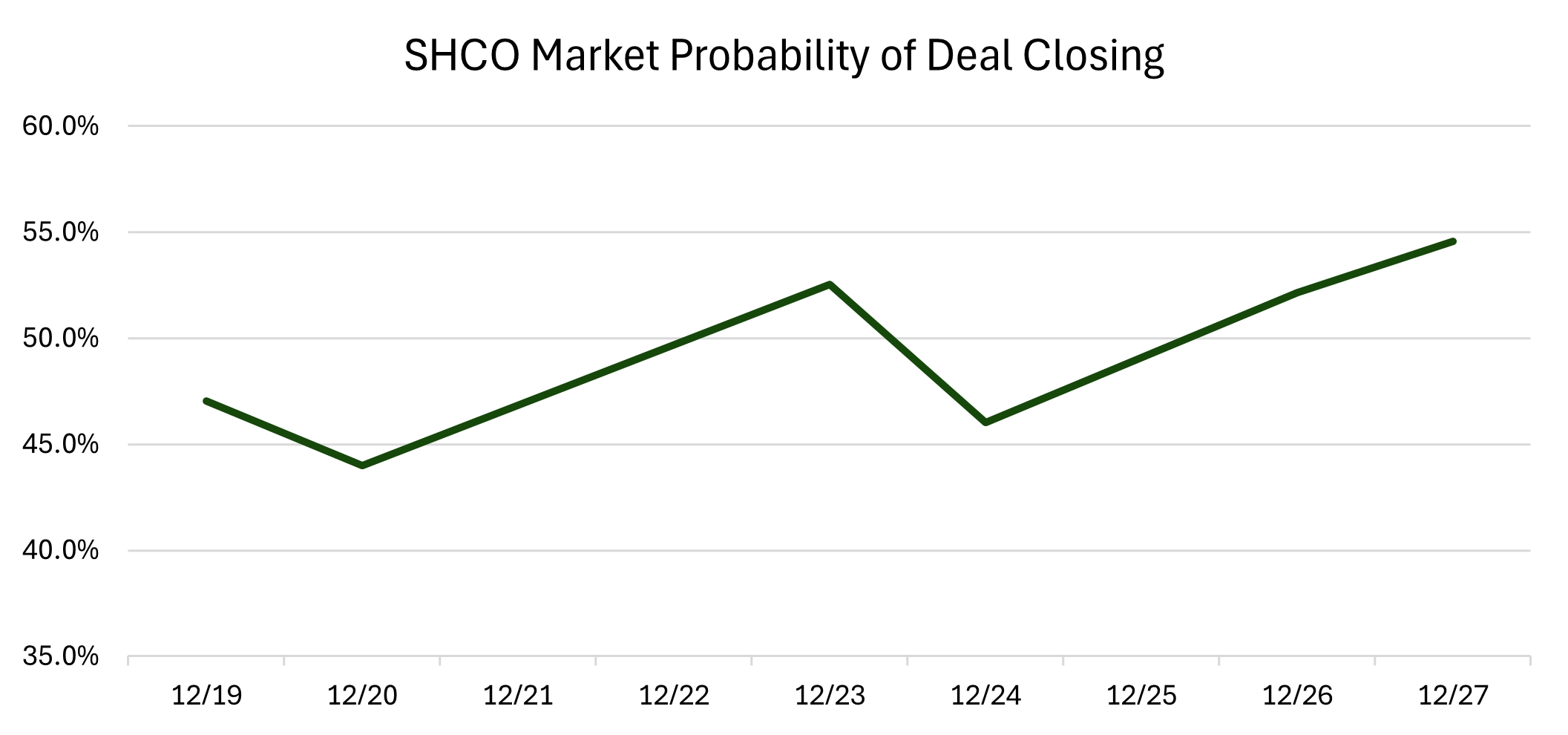

We think this offer is not as solid as investors might hope, so the market is assigning a mere 55% of happening despite no regulation risk.

Disc: We are short Soho House (SHCO) which we disclosed Friday morning.

The Rise and Quick Fall of Soho House

Soho House (SHCO) is the exclusive, referral-only club in the hottest cities worldwide, from New York to Berlin. It was once the epitome of cool, drawing celebrities including Taylor Swift, Justin Timberlake, Jessica Biel, and Leonardo DiCaprio to hang out by a rooftop pool first endorsed by the ladies of “Sex and the City.”

But what was once cool quickly faded as the allure of exclusivity slowly died in its run-up to COVID, and then it seemed to have taken a shot to the abdomen once COVID came.

>100,000 members joined the club during that time — which pushed memberships above 250k by the end of 2023 — and “opened the floodgates” to become overcrowded clubs in the name of growth.

The stock IPO’d through a SPAC in 2021 and has almost nothing but gone down.

A recent thorn in the side came from Glasshouse Research who noted on February 7, 2024, that they were short the company and made a subtle link to the future of SHCO being similar to that of WeWork, which is now bankrupt. You can see their report below.

Once they released their short report, which we find to be credible, the company announced that if this is the way the public markets will treat them, perhaps going private again is in the best interests of the company.

Then in March of this year, they announced they were in talks with CC Capital to take the company private. Ron Burkle, a billionaire and one of the company's largest shareholders through Yucaipa Companies, stated that he would be rolling his equity into the deal and advocated that SCHO should take it.

The above is important because it also pertains to the current offer on the table which we’ll discuss in a minute.

The odd part of this announcement was that it was all just talks, there were no concrete statements or facts, and it didn’t even suggest the price for it to be private.

Long story short, in May, the company stated that it had “rebuffed an offer by an unnamed party despite it being at a ‘substantial premium’ to its current market cap.”

“The special committee concluded that the offer did not adequately reflect the value of the company and was not in the best interests of its public stockholders.”

More on this in a minute as well.

Since then, the stock has been going back to its slow decline and completely ignored the broader market rally from the FED cuts this year + the Trump rally post-election.

All of this brings me to my next point which is the most recent announcement that they got the day they announced Q3’24 earnings.

Offer to Go Private

On December 19th, SCHO received an offer from a third-party consortium to acquire the company for $9/share. This third-party consortium was not named but there was a condition tied to this offer.

“The offer is conditioned on certain significant shareholders, including amongst others the Company’s Executive Chairman, Ron Burkle, and The Yucaipa Companies and its affiliates (“Yucaipa”), rolling over their equity interests in the Company as part of the transaction.”

This would make sense because Burkle has stated in the past that the stock market has not been valuing the company appropriately.

“When we went public I believed the market would reward growth, but it seemed to quickly switch to rewarding free cash flow and profit over our top-line growth. So at this point in time we have all the costs of being a public company with few benefits.”

Ron Burkle and Yucaipa have already publicly stated that they are supportive of the $9/share deal (just like last time) and he currently owns ~47% of SHCO.

Together with the Voting Group (Richard Caring and founder Nick Jones), they own 74%, and control 96.6% of the voting (Class B) shares. BofA estimates that the remaining shareholders (51.1M shares ex. the Voting Group) must approve of the deal.

Why We’re Skeptical

When we first looked at this deal, we originally thought it might warrant going long the common shares since there was an offer on the table (allegedly) with a set price ($9) that involved the biggest players rolling their equity.

The rolling of the equity was interesting given that would mean the company might not have to be levered up like in a traditional LBO. Given that the company’s balance sheet is not in the best health (current LTM net debt / EBITDA of 7.9x) and has never been profitable, the company can’t really handle more leverage.

While they also haven’t raised capital through an equity offering recently, they have raised debt to help expand and buy back shares in an effort to sustain some semblance of a floor on the stock price.

The additional point that we liked was that there would be no regulation risk (FTC) that would need to be cleared in order for a deal to close. All of these points, the rolling of the equity, one of the largest shareholders saying yes (once again), and no regulation risk, all seemed good.

However, when you think about all the positives here, you’d think the arb spread would be much tighter. Perhaps not within 0% - 5% of the closing price but ~10% - 15% given there wasn’t much detail on the offer besides the condition they mentioned.

As of Friday’s close, the market was still only pricing in just a 55% chance of the deal happening which was very surprising to us. Yes, the trend has been going “up” but given that we’re in the Santa Rally zone, anything is possible but given recent ADV being above the rolling 10D average before the deal, we don’t think it’s an issue of volume.

Why we turned skeptical is three-fold.

The market probability is not as high as it typically would be if investors thought the deal was likely given no regulation risk.

Not believing that enough stakeholders will want to roll their stakes (Richard Caring and founder Nick Jones).

The conditions of the deal might not be suitable.

We’ve already gone over point #1 and to expand on point #2, I’m not 100% sure that Richard or Nick want to go back to being private.

As a reminder from above, the company received an offer earlier in the year that was “rebuffed” because it was too low. Prior to the “talks” announcement, the stock was trading at $4.97/share and quickly shot up to $6.

As time went on, the stock trickled down to ~$5/share when the “rejection” took place. Since in the PR, they said the offer was a ‘substantial premium’ to the then-current market cap, it begs to question how different was it versus the $9/share they just received.

The stock was trading at ~$5/share before the most recent PR, similar to what happened before, and given the fundamentals have not improved much, will Nick and Richard view this as any different than the previous offer?

We won’t deny that SHCO being a public company is expensive and not ”benefitting” them but at the same time, being public allows for liquidity and to at least tap into equity capital markets.

We bring up liquidity because while he’s just a part of management, Andrew Carnie (CEO) treats his shares like a piggy bank.

Not a bad setup if he’s continuously selling his shares but also not a vote of confidence in the stock. Additionally, based on Q3 earnings, it seems like they’re trying to turn things around given the transition of their ERP system, restructuring, and 1x issues in Malibu/Farmhouse.

We bring this up because Nick and Richard might not want to limit their upside if a turnaround is in place but we still feel that a turnaround is not likely.

To point #3, while the publicly stated conditions of rolling equity were a must, we would assume that there is some level of strategy shift needed given that the current strategy isn’t working.

Taken from the PR,

“No assurances can be given that the Special Committee's assessment will result in any change in strategy, or if a transaction is undertaken.”

Granted, we have no hard evidence for this fact but given our experience with companies taken private due to the market not giving it the public valuation it deserves, it’s usually not because they’re unprofitable or because the current strategy isn’t working.

Ron Burkle, the most outspoken person on SHCO says that the company is profitable if you just look at it the ‘right way.’

That definitely gave us vibes related to WeWork’s “community-adjusted EBITDA” metrics when they were going public.

All of which makes us uneasy that

This offer is a genuine offer that only consists of just the rolling equity condition, and

Everyone besides Burkle is as excited about it.

But just like every arb trade, there is risk.

Trade Risk

First things first, there’s no regulation risk so we can go ahead and rule that out. Now let’s look at the risk/reward going forward.

The upside from here is the implied $9/share takeout price and based on the closing price on Friday of $7.59, there’s ~18.6% of juice left. However, we believe that if we’re right in calling this bluff, the stock can easily mean revert to ~$5/share before the announcement and then some if you believe the company is still in for a slow decline, especially after cutting EBITDA guidance.

If we account for the $5/share mean reversion, then a possible ~34% decline is in the cards if the bluff is correct.

A $1.41 upside to a $2.59 downside (with a further decline in fundamentals) is worth it in our view to take a small speculative position in the name by shorting SHCO shares, which we have done.

The last talks of being taken private occurred in the middle of March with a rejection on the last day of May. I imagine the same amount of time if not less, would take place so we can estimate an update by the end of February or before as part of the timeframe considerations.

As always, we appreciate your support of our work. If you have any questions, please make sure to message or comment below. If you think others would benefit from the research/commentary we release, we would greatly appreciate you sharing.

Until next time,

Paul Cerro | Cedar Grove Capital

Personal Twitter: @paulcerro

Fund Twitter: @cedargrovecm