Hey there,

Today’s discussion is on Peloton (PTON) with a fellow investor with whom I’ve spoken from time to time over the last 1.5 years about the name, Alex Morris, founder of

.Alex and I cover a lot of consumer names, and PTON happened to be one that we both had thoughts on a few years back. We’ve been trying to set up a podcast to talk about PTON and with their most recent earnings last month, it seemed like a good time to finally sit down and chat about the name.

To follow Alex and his work, I’ve included the links below.

His book: Buffett and Munger Unscripted

His most recent PTON article 👇🏼

To get my report on PTON, continue reading below. It’s free. Enjoy!

Disclaimer: All information provided herein by Cedar Grove Capital Management, LLC (“Cedar Grove Capital” or “the fund”) is for informational purposes only and does not constitute investment advice or an offer or solicitation to buy or sell an interest in a private fund or any other security. An offer or solicitation of an investment in a private fund will only be made to accredited investors pursuant to a private placement memorandum and associated documents.

Cedar Grove Capital may change its views about or its investment positions in any of the securities mentioned in this document at any time, for any reason or no reason.

Students can get access to our research at a reduced rate by clicking here. If you’re interested in using Koyfin (I highly recommend it), you can get 20% off your plan using my link here.

Interested in becoming an LP? Click here to fill out the contact form.

“Has the current moment changed your view of the size of your potential market?

It hasn’t changed my view at all. I see a couple [of] hundred million people on the Peloton platform in 15 years. But it has changed other people’s views for sure.”

- John Foley, former PTON CEO for Times, May 26, 2020.

Five years later, there are only 6.1 million people on the platform, and that number has been dropping since the first quarter of the 2022 calendar year.

Peloton (PTON) was one of those names that caught bulls in euphoria, especially the original CEO, and bears in the crosshairs during the COVID era. We, ourselves, ended up in the crosshairs when we went public in early 2022 that we were short the stock. Took a TON of heat on that one from the cultists at the time.

Since then, it obviously turned out to be a really great trade for us.

But we wanted to touch base on Peloton since the last time we put a report out on the stock, because a lot has happened over the last year, and it seems to be in a much better spot than when we closed our short in 2023.

Investors seemed to have flocked back to the name, and many are once again calling for it to rise like a phoenix from the ashes.

Perhaps it’s worth a revisit to go long? We’re not so sure.

If you recall, in our quick note from August of 2023, when the stock was trading at $5.87, we advocated for the company to just sell themselves and live on to fight another day under someone else. Someone with a healthier balance sheet and firepower to get them to where they need to go.

We echoed these statements when we talked to Reuters in May of 2024.

"Somebody needs to acquire them because at this rate, I don't even know if this company will still be a company on its own in the future.”

The company was struggling under its debt load, still losing app subs and Connected Fitness (CF) subs, FCF was down, and things all over were not looking rosy. Oh, and to top it off, Barry McCarthy stepped down abruptly, which was certainly a surprise to us.

Given how quickly FCF was leaving the door, it was not a contrarian take to think that a potential bankruptcy might be looming for the company if they couldn’t plug the holes in their ship.

But since then, the company has managed to refinance its debt, which immediately stemmed bankruptcy fears, and prevented a sinking ship from completely going under.

The name of the game, though, under both Barry and the interim CEO, was to ‘stop the bleeding’ by throwing anything not bolted down overboard (i.e., massive cost cutting).

This entailed the aforementioned debt refinancing, multiple rounds of layoffs, impairment charges, right-sizing inventory and supply chain costs, etc., etc.

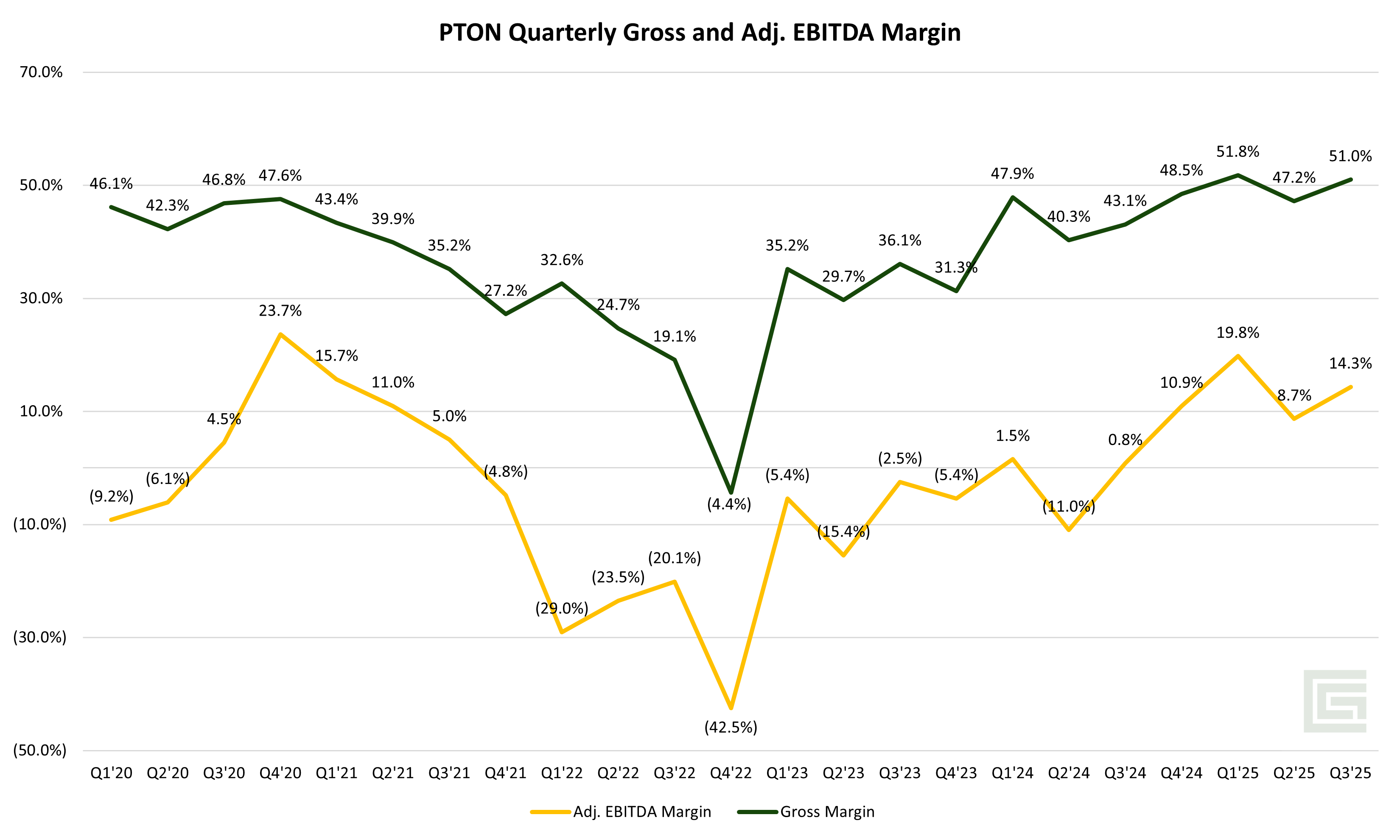

It panned out as of yet when adj. EBITDA margins finally broke positive territory last year, and gross margins have never been higher.

"From Q3 to Q4, the narrative has changed from Peloton needing a life jacket immediately to being able to tread water for a bit longer." - CGCM, Reuters August 2024

But while we applaud the much-needed turnaround, we’re skeptical if growth will come back in a meaningful way, considering that even though the company has been able to turn a profit, it still has yet to show that sales growth is returning.

This is after making major changes to its sales channels from

Partnering with Hilton Hotels, other gyms, and various business clients

Expanding beyond cardio by pushing strength training

Snapped back at the secondhand market with a one-time activation fee

Introduced the rental program to give prospective buyers a chance to try it out

And are testing different retail size layouts, along with a push towards holistic wellness

Despite throwing all the wet spaghetti they could at a wall to see what stuck, Y/Y quarterly sales growth continues to decline, and the fact that PTON can’t get growth back on the menu despite these efforts is what continues to worry us.

You could argue that post-COVID, many were looking to ditch their equipment to go back to the traditional gym or other fitness studios. This would lead to less convinced members churning at a higher rate, thus reinforcing a stickier base for the company to then build up on after it moderates.

This has shown up in the CF churn rate, which seems to be on par with the average in FY’23/24 (CY’22/23) when we fully returned to a world after COVID.

However, it doesn’t seem that bullish argument turned out to be the case since overall members continue to decline, but CF subs saw a modest 5,000 sub gain sequentially based on the Q3’25 shareholder letter, but we’re a little suspicious about that fact.

In the Q3 footnote, it says

“Beginning January 1, 2025, the Company migrated its subscription data model for reporting Ending Paid Connected Fitness Subscriptions, Average Net Monthly Paid Connected Fitness Subscription Churn, Ending Paid App Subscriptions, and Average Monthly Paid App Subscription Churn to a new data model that provides greater visibility to changes to a subscription's payment status when they occur. The new model gives the Company more precise and timely data on subscription pause and churn behavior. Prior period information has been revised to conform with current period presentation”

Emphasis on the bold part because we find it hard to believe that they’ve been calculating subscriptions inaccurately over the last 5 years, which allowed their Q2’25 CF subs to decrease from 2.879 million to 2.875 million, allowing a Q3’25 growth of 5,000 to 2.88 million. Coincidentally, this also boosted the paid app members from 582k to 585k. Not sure what new technology they implemented to really only affect the previous quarter, but it certainly smells.

On the debt front, net debt continues to decrease, and they have a $200 million convertible note due next February (2026), but with a current cash balance of $914 million, this shouldn’t be an issue.

Either way, we struggle to understand why investors are still optimistic about the future of this company as an investment, even though a lot of their ~$200 million in cost-cutting is priced in, and the traction just isn’t there.

Even for FY’25, granted it ends in just one quarter, the company is still expecting to see a sales decline of 9%, a CF sub count decline of 7%, and a paid app member decline of 12% y/y at the midpoint.

While it’s very clear that management is not messing around when it comes to this turnaround, we can’t imagine FY’26 being a gangbuster year for growth either, especially after a questionable consumer backdrop given tariffs (they are subject to the 25% aluminium tariffs which are not 50% as of yesterday), higher rates, and unemployment uncertainty.

We think that at an NTM EV/EBITDA multiple of 11.2x and a LTM P/FCF of 10.9x, much of the “easy” money has been made since the debt refinancing, and there’s better risk/rewards out there for capital deployment.

We’re choosing to stay out of this one and will watch from the sidelines.

As always, we appreciate your support of our work. If you have any questions, please make sure to message or comment below. If you think others would benefit from the research/commentary we release, we would greatly appreciate your sharing.

Until next time,

Paul Cerro | Cedar Grove Capital

Personal Twitter: @paulcerro

Fund Twitter: @cedargrovecm