Green Thumb Industries is growing like a weed, pun intended

Cannabis is booming, are you coming along for the ride?

Summary

Green Thumb Industries’ (GTBIF) excellent track record of effective cash management and operational discipline will allow them to continue being one of the best-positioned cannabis companies to lead the market forward

Continued same-store sales growth and an emphasis on improving margins will get the company to net income positive in the next one to two years

Current industry valuations show that Green Thumb is undervalued compared to its peers on a price/sales multiple

Background Context

Back when I was an investment banker on Wall Street, I was one of three analysts that were covering the cannabis industry. I was covering clients like Hexo, Tilray, Charlotte’s Web, etc.

This was back in 2018 when the cannabis/CBD market was really coming full swing. I remember seeing Tilray’s stock jump from $30 a share to almost $150 in a matter of 2 months. Giving it an enterprise value north of $10bn on sales of just ~$25M USD. It was nuts, and people made tons of money!

The 2018 Gold Rush

2018 was the new gold rush for cannabis. Various companies, both headquartered in the U.S. and Canada were going public on exchanges and institutional and retail investors wanted in. Valuations were going sky high on no real growth fundamentals other than FOMO.

Cannabis companies were smart and took advantage of their sky-high valuations to merge with other players in an effort to consolidate or issue equity to bolster their war chest for the impending blitz of U.S. legalization.

Once these companies had the cash they needed, an all-out land grab started. Players were buying up physical land to grow more crops and build facilities. Others wanted to expand internationally and plant the flag before anybody else was able to get there.

This period was literally a grow and expand at all costs.

Needless to say, that ended very quickly once investors understood that legalization was not going to be happening as fast as they thought, and investing at a 200x sales multiple made little to no sense.

This being said, cannabis was still growing and was poised for a comeback, which if you paid attention last year, 2020 was the time to put your chips on the table.

Total Addressable Market

In 2019 the U.S. legal cannabis industry generated an estimated $13.2 billion in sales across all medical and adult-use state markets. However, in 2020, despite socioeconomic disruptions amid the COVID-19 pandemic, total legal cannabis sales are projected beyond $19 billion.

Projecting a compound average growth rate (CAGR) of 18% over the next five years, by 2025 total annual U.S. legal sales should exceed $35 billion.

Between 2020-2025, the total combined U.S. market opportunity for legal cannabis sales is estimated at $172 billion.

Projecting that 18% CAGR, annual medical cannabis sales are estimated to nearly triple from $5.8 billion in 2019 to $16 billion in 2025.

Meantime, annual legal adult-use sales are projected to grow at a 17% CAGR, from $7.4 billion in 2019 to $19 billion in 2025.

Conversely, illicit market sales will slow due to legal markets: New Frontier Data estimates that 17% of all 2019 U.S. cannabis sales were legal; in 2025 more than one-third (34%) of total annual demand will be met through legal markets.

Legal cannabis industry expansion is fueled both by new markets as more states adopt legalization and by sustained demand growth as consumers transition from illicit to legal markets.

But let’s get to why you’re all here.

Green Thumb Industries

Business Overview

Green Thumb Industries manufactures, distributes, and sells various cannabis products for medical and adult-use in the United States. As of the most recent quarter, it owns and operates 48 retail stores (with licenses for 96 locations) across 12 states. It has 7 private label brands under its portfolio and sells them through third-party retail stores as well as its own ‘Rise’ retail stores.

It is headquartered in Chicago, IL, and one of the bigger players in the cannabis market that is of U.S. origin.

Why Green Thumb? Why Now?

Good question! You’re probably wondering after its meteoric rise in 2020, having increased its share price by a whopping 259%, if the stock has more room to grow or if Green Thumb is even the right horse to bet on given the pick of the litter of cannabis players.

The short answer is, yes. It has plenty of room to grow and I think Green Thumb is the right horse to bet on. Even if you look at how it performed against its competitors in 2020, it blew them out of the water (Tilray, Canopy, Aphria, and Aurora). Many investors must have been feeling the same way especially with the potential of a Democratic president coming to the office and a slimmer chance of there being a blue wave.

When it comes to investing in cannabis, there are a number of key considerations that I specifically look at to make sure I’m covering most areas of importance. These are not in any particular order.

Overall growth

Same-store sales growth

Cash management and debt levels

Margin improvement

Unlike tech firms, cannabis companies cannot light money on fire in the name of growth and expect their high product margins to save them at the expense of marketing spend. Cannabis, in a complete reversal, is a very capital-intensive business, with lots of marketing and financial red tape, and investing in the company that has grown responsibly and who has set itself up for success for the long-term will be a real winner.

I believe that Green Thumb has met, if not excelled, at the aforementioned areas of focus. So let’s start diving into the good stuff!

Overall Growth

Aside from the run-up in the stock, which has surely made a lot of people rich, Green Thumb has seen sales grow by at least double, every year, for the last few years.

Not only has the company caught up to its competitors but it has even surpassed them for the first nine months of 2020.

Green Thumb has seen an impressive 278% sales growth in 2018, and another 246% in 2019. With average FY 2020 sales estimates of $545M, that would imply an over 150% jump from 2019 figures.

With more and more states coming online, some a little faster than anticipated, has led to the company recognizing growth in a reduced timeframe. The company has made significant investments in its cultivation and retail operations (which I’ll touch upon in a bit) which have led to increased sales.

In their most recent earnings call, management said that what happened in their home state of Illinois is exactly what they think will happen with the rest of the country as each state opens up.

“Five years into legal cannabis in our home state of Illinois and only 10 months into adult-use here, industry-wide cannabis sales for the state are approaching $1.5 billion on an annual run rate basis. Illinois adult-use grew double digits for the month of October and over 330% year-over-year. That's impressive growth, but amazingly, nowhere near the top…….We have 8 open stores across the state with the potential for 10. We believe what is happening in Illinois will happen across the country. It is a matter of when, not if.”

This market is in no way slowing down and with the recent passing in New Jersey and hints that NY governor Cuomo wants to legalize cannabis will leave incredible amounts of whitespace for the company to profit off of.

Given that retail stores can only be grown to the extent of the number of licenses you have (the company has 96 in total to use), continued growth in the CPG category, estimated to be a $100 billion market and grow at an annual rate of 20% in the next decade, will help drive sales and overall margin improvement.

Heck, they even announced a partnership with the cannabis beverage brand Cann, to help them distribute nationally.

Productivity and a great product mix will be the name of the game going forward, both of which Green Thumb is currently doing a very good job with.

Same-Store Sales Growth

As mentioned previously, many states have a cap on licenses in the name of creating a free and fair market. This means that you can’t have a monopoly in many states and have to be creative to your growth once certain limitations have been met.

For cannabis companies, being able to secure retail licenses is key for continued growth. Once they have been issued and secured, the next step is optimizing your store’s sales. With nearly half of Green Thumbs licenses currently being used, I want to point out that it’s time to start recognizing how their stores have been performing.

Looking at their retail operations sales figures and comparing that to the number of stores that they have at the end of the quarter, the average sales per store has grown from $1.1M to ~$2.3M in Q3 of 2020.

Before you throw me to the wolves, I understand that this is not a perfect apples-to-apples comparison since not all stores may have been open at the beginning of the year. This is true, however, when you look at their same-store sales growth (stores that have been open for at least 12 months) Green Thumb has posted some pretty impressive figures. In both Q1 and Q2 of 2020, same-store sales figures have exceeded 75% and in Q3’20 they exceeded 65%. That’s nuts! Back when I covered retailers in my banking career, you’d be happy that they hit high single or low double digits, depending on what type of company it was.

Better yet, according to American Cannabis Consulting,

“More than a quarter of dispensaries generate annual revenues exceeding $1 million. Another 15 percent report annual revenues between $500,000 and $1 million.

Well-established dispensaries often have thousands and even tens of thousands of loyal clients, tested products, professional packaging, and a dozen more employees.

Such businesses report annual sales that climb as high as $10 million, while dispensaries located in remote areas bring in closer to $3 million.”

Even if we were to peg the company to the $3M market, at its current store count, that would almost at an additional $34M to topline figures. Factor in the $10M count, which might happen years down the road with total legalization, we’re talking upwards of half a billion in additional retail sales.

Cash Management and Debt Levels

Another key point, where I feel many cannabis companies have either failed on or mismanaged, is effective cash deployment and maintaining debt levels. Like I mentioned towards the beginning of this report, the mid-2018 blitz of many of these companies going public and selling their shares at the peak of their valuations was an excellent call by management. With this said though, not many deployed their newfound capital in effective ways. I labeled it a “land grab” previously and that’s exactly what it was.

Many of these companies used their cash to buy massive amounts of land for cultivation in anticipation of a supply glut, the construction of new processing and growing facilities, expanding internationally to Europe and Latin America, acquiring smaller players in cash/stock deals all in the name of needing to be a front runner in an explosive market.

Boy, they were wrong, kind of. They put the cart before the horse and valuations came tumbling down once the market realized that it wasn’t going to grow as quickly as many thought. The once-massive war chests were now dwindling and with negative free cash flow being generated from these companies, their burn rates were blinking red, telling management that the brakes need to start being applied.

So with that context, what do I mean by this in relation to Green Thumb?

Over the last few quarters, and in 2019 and 2018, the company has been able to effectively keep enough cash on the balance sheet in order to meet short-term obligations without needing to raise money.

Post the massive cash inflows of 2018, Green Thumb has been able to keep its current ratio (an indicator of a company’s ability to pay short-term obligations or those due within a year) above 1, which is good. This doesn’t necessarily mean that they are the best in the industry with this, but rather that I have no concerns about their ability to meet these short-term obligations. Aka, no cash crunch.

In addition, they have announced, earlier in February, a $100M raise, which was completed by a single institutional investor. Management labeled the reason for this raise was to take advantage of their current valuation and shore of their balance sheet and use it for general purposes.

I believe the company has shown operational discipline over the last few years, and with realistic expectations of the cannabis market growing sooner rather than later in the U.S., they want to position themselves appropriately when the time comes.

To further reinforce this point, I wanted to also bring up their debt/EBITDA ratio over time.

What’s encouraging to see here is their multiple going down significantly over time. While their debt levels have grown marginally from $91M in 2019 to $97M in Q3’20 (a 6% increase), EBITDA has grown from a loss of $4M in 2017 to over $100M in the first nine months of 2020. Having achieved positive EBITDA margins this past nine months is a major feat and should not be downplayed in the slightest.

I’m very curious to know how their 2020 ends on an adj. EBITDA basis, but in the meantime, I’m happy to see management putting an emphasis on becoming profitable on an EBITDA basis instead of running in the red for longer.

This growth will be able to help the company eventually pay down debt and keep future debt raises at a minimum, especially with rates expecting to rise over the next few years.

Margin Improvement

Supporting all of the above callouts between topline growth, same-store sales increases, cash, and debt management have all trickled down to the table below.

When looking at valuable companies to invest, keeping an eye on margins is incredibly important. I mean, how do you expect a company to eventually become profitable if they aren’t improving margins in their respective areas in order to get there? Hence, why companies like UBER haven’t been profitable in the entirety of their existence.

Green Thumb has been able to improve margins and as you can see from the table, even became net income positive during Q3’20. Gross margin increase since 2017 has increased 15bps from 40.7% to 55.4% and what I touched upon previously, EBITDA margin has increased 56bps from (24.7%) to positive 31% in the same period.

This is a direct result of management’s strict operational focus and carefully curated strategic investments to advance the company in a responsible but also defensible way.

I strongly believe that the company will achieve better margins in the years to come with increased economies of scale and organic growth from the millions of consumers still itching to buy into the recreational market.

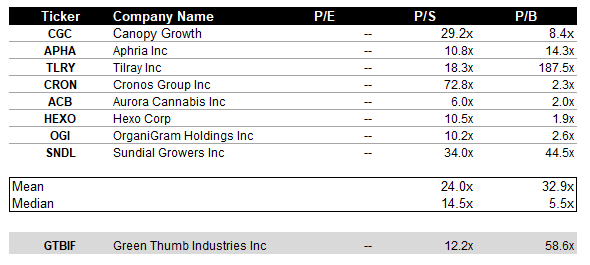

Valuation

Valuing cannabis is difficult. Many are not net income profitable or even profitable on an EBITDA basis. So what is Green Thumb worth then? I laid out for you a comps table below, trying to incorporate a few of the public cannabis players to give you a more holistic view of the current landscape.

As of Tuesday’s close, the company had a ~$6.8B market cap. Applying the median P/S multiple of 14.5x to estimated 2020 sales of $545M, the company is valued at $7.9B. This is a 16% upside from Tuesday’s value and if we want to get more creative and cut negative growing Aurora (ACB), the median multiple is 18.3x and the implied valuation becomes $9.9B. Even though this number looks better for obvious reasons, I believe this is a more accurate picture of what Green Thumb Industries can become in the next few years.

*Callout*

Anticipated earnings release scheduled for March 17, 2021, to announce Q4’20 and full-year 2020 earnings. Though this is my opinion on Green Thumb Industries, please do not act solely on the information written in this article and make sure to do your own due diligence before taking a position.