FIGS: Not the lululemon of Healthcare Apparel

Why I believe that FIGS scrubs has been grossly overestimated to be the lululemon of healthcare

Summary

Despite a highly successful IPO, FIGS has reported earnings twice that have left investors to sharply sell off the stock

Their premium product inherently decreases the TAM despite management's constant reiteration of the opposite

The rate of insiders selling is quite alarming and doesn’t paint a good picture of future conviction of the stock price

Valuation of other high-growth apparel/footwear brands shows FIGS is still flying a little too close to the sun

Company Overview

FIGS FIGS 0.00%↑ is a fast-growing direct-to-consumer healthcare apparel brand. They design and sell apparel via two core categories, scrubs and other non-scrub offerings such as lab coats, under scrubs, outerwear, and other lifestyle products.

The company has been dead set on disrupting the over 100-year-old scrubs market through its comfortable and fashionable clothing. This has allowed the company to grow a large and loyal community of healthcare professionals propelling them from under $100k in sales in 2013 to $263 million in 2020.

This growth from any consumer apparel brand is impressive and should not be ignored. Additionally, FIGS mainly operates in the United States but within the last few years has been expanding internationally to Canada, the United Kingdom, and Australia.

Performance Since IPO

Since its May 26th IPO, the company priced at $22 a share above the range of $16 - $19 and increased the number of shares from 22.5 million to 26.4 million raising nearly $581 million. The stock ended up soaring 36% on its first trading day closing at $30.02. The stock has reported two earnings prints which saw the stock sell-off quickly after on both takes. Despite all this, many retail and sell-side analysts are bullish with an average rating of $44 a share.

Why Many Are Bullish

What I love about consumer companies is that they are a business that is incredibly easy to understand. There's nothing fancy or high-tech about them (usually) and your own experiences and general knowledge allow you to potentially formulate opinions that are not out of this world. In this particular case (FIGS), you might even have someone close to you that can provide you first-hand due diligence before you think about investing in this company.

Because of this, here's why I believe many are bullish on the stock.

Growth rate and key metrics impressive

Since going public earlier in the spring, FIGS has had two earnings releases that have each sent the stock price moving strongly in either direction. Overall sales in Q2 and Q3 grew 57.6% and 33.7% y/y to $101 million and $103 million, respectively. Even the full year jump from 2019 to 2020 posted an increase of 138.7% to $263 million in sales. The numbers that FIGS has been able to print are actually quite impressive. They also have a $1 billion sales goal in 2025 that they have been reiterating in their long-term guidance objectives which would put them at just under 300% growth from 2020 levels in 4 years.

What I love about FIGS financial statements is that it also posts two key metrics that investors like to have access to in order to help determine the health of the business. Average order value (AOV) and the number of active customers. Like it sounds, AOV is the average size of the basket of goods per order that a customer buys. The higher the number implies that either more people are buying more goods within each order or that they are adding higher-priced goods, both suggesting an increase in margins. Bigger orders mean better margins which in theory can translate to a fatter bottom line (all else being equal).

For active customers, the company labels them as customers that have purchased at least once from the company in the last 12-months.

They've been able to grow their active customer base from around 300k in 2018 to 1.7 million active customers by the end of Q3'21. An almost 8x growth in just a few years.

Gross margins

As I've scoured the internet digesting any and all reasons why people are in love with FIGS I continuously came to the point of how high their gross margins are. FIGS ended fiscal 2020 with gross margins of 72.3% which was up 50bps from 2019 and recently reported Q3'21 gross margins of 72.7%.

Management has constantly reiterated on earnings calls that they are targeting over 70% gross margins and 20% adjusted EBITDA margins over the next three fiscal years.

So how does this compare?

Not to say that FIGS should be compared to all of these companies, rather I just wanted to highlight how well they have done in achieving superior gross margins compared to various other retail apparel brands.

It's not hard to see why many would cling to this as an important metric but I'll touch on why one shouldn't apply too much weight to this further down in my article.

CAC and retention

Another point which I love is how well the company has been able to market their products with great efficiency. A few interesting points while I was reading through their S-1 and recent transcripts point to how well their marketing (both paid/organic) has led to explosive growth.

Given the $ paid in CAC, they are profitable with each customer on their first purchase.

From 2018 - 2020, CAC has decreased by 61% from $101 to $39.

Customers come back on average every 90 days to make a purchase.

Since 2017, FIGS has had healthy, double-digit repeat retention metrics as a % of total sales: 2017 - 44% repeat customers, 2018 - 52%, 2019 - 59%, 2020 - 62%.

This is solid for investors who want to make sure that the company isn't spending enormous amounts of money to attract customers to try their products. What I also love is that the CEO, Catherine Spear, mentioned in her Q2'21 earnings call just how much word of mouth plays in their organic growth.

If you think about word of mouth, for instance, health care professionals, as I discussed, they were in densely populated health care institutions. They're interacting with each other all the time, in the break room, in the coffee shop in the lobby, in the hallway, in between patient business. And they're looking -- they were looking at what they're wearing, and that's essentially free. It's like a walking billboard. No marketing is really necessary for that.

I am keen to believe her when she says this because when you think about it, you're wearing scrubs all day and surrounded by your other coworkers that are doing the same. It is not hard to believe that in passing or like Catherine mentioned, in the break room, a colleague asks "where did you get that?" As long as this method does not fundamentally change, I don't think anyone expects it to, we can continue to see FIGS having continued significant organic growth from their loyal fan base.

Premium quality, premium product

For many that already know and for those that don't already know, FIGS has a high-quality product that many customers all seem to agree on. Even when I was digging around for any possible negative reviews, I mainly found that even those that had a problem with the product (mainly sizing frustrations) still mostly admitted to liking the product quality.

Even the company website, which I usually discount since this can be heavily manipulated, has stellar reviews of their product, with an example of a men's scrub top having a 4.75/5 rating off of nearly 4,800 reviews. The bottom line, can't have a fast-growing company without a great product(s) to back it up.

NPS score best in class

FIGS boasts an NPS score of (+81). NPS is often held up as the gold standard customer experience metric. First developed in 2003 by Bain and Company, it’s now used by millions of businesses to measure and track how they’re perceived by their customers. NPS scores determine segmenting between poor and positive feedback.

It measures customer perception based on one simple question:

How likely is it that you would recommend [Organization X/Product Y/Service Z] to a friend or colleague?

Respondents give a rating between 0 (not at all likely) and 10 (extremely likely) and, depending on their response, customers fall into one of 3 categories to establish an NPS score:

Promoters (score 9-10) are loyal enthusiasts who will keep buying and refer others, fueling growth.

Passives (score 7-8) are satisfied but unenthusiastic customers who are vulnerable to competitive offerings.

Detractors (score 0-6) are unhappy customers who can damage your brand and impede growth through negative word-of-mouth.

Subtracting the percentage of Detractors from the percentage of Promoters yields the Net Promoter Score, which can range from a low of -100 (if every customer is a Detractor) to a high of 100 (if every customer is a Promoter).

To give you a benchmark of other apparel brands, lululemon (LULU) has a score of 6, Nike (NKE) has a score of 30, and Adidas has a score of 28.

Comparing this to some other high-profile names that have commanded massive PR from athletes and celebrities, FIGS is doing quite well relatively.

The Reasons to be a Bear

So from what I mentioned above, it seems very likely that this company could be a home run and an early lululemon (LULU). Margins are great, growth is extraordinary, their customers seem like they love the product and they are profitable.

I myself was looking to see if FIGS would be a great buy but as I continued my research, I started noticing things that made me feel as if the company might be overvalued.

TAM is grossly overstated

One of the main points I noticed that the company kept reiterating in their S-1 and all of their financial statements is just how big the total addressable market is. In their S-1, they say that:

The healthcare sector is the largest and fastest-growing job segment in the United States, employing over 20 million professionals in 2020

Total U.S. employment between 2019 and 2029 is expected to grow by 15% for all healthcare professionals versus just 4% for all occupations

The U.S. healthcare apparel industry was valued at $12 billion in 2020 and expected to grow at a CAGR of 6.1%

The global healthcare apparel industry was valued at $79 billion

Estimate that 85% of medical professionals now purchasing their own uniforms

Currently, management has said that they have about 3% market share and that they can have further penetration as they continue to disrupt the industry.

While these numbers may look very enticing for an investor, the way that the company markets it can be misleading. This figure ($12 billion) is on the overall healthcare apparel market but FIGS business doesn't actually apply to the whole thing at the moment.

Many places still offer their employees scrubs sponsored on their behalf, certain color requirements, and even requirements to wear branded healthcare apparel (i.e. lab coats, scrubs, etc.). *I found this out when I spoke to numerous sources in various fields about using/not using scrubs*

What's worse is that this market has been around for a hundred years and was dominated by the wholesale model, providing healthcare workers with relatively cheap access to clothing that cycles through quite often. Paying $100 for a scrubs work uniform is very expensive and inherently limits the TAM when there are other cheaper options readily available. I'll touch base on this more in the next segment of having no defensible moat.

Also, FIGS benefited, like many other companies during the pandemic, from having a pull-forward of sales because of COVID-19. Pre-COVID, many healthcare professionals opted for either wearing scrubs or doing business casual with a lab coat. Because of the unknowns of the virus early on and for some time through 2020, many medical offices required that all staff switch over to scrubs as a response to increased safety requirements. This made many have to increase their current scrubs count and those that needed to switch over entirely (confirmed by various working sources I spoke with).

Since this year, many have started to revert back to wearing business casual as more information about the virus has come to light and vaccine rollouts have already surpassed half the eligible U.S. population. This logic has shown in their sales growth as they grew 137% in 2020 but are only assuming 56% growth for 2021, and 33% growth in 2022. A steep decline that should be flashing warning signals when you're considering paying 12.5x forward EV/sales.

No real defensible moat

As I mentioned before and throughout this post, FIGS has produced very well-made apparel products. This is why many have put their chips in it for the sake of a lululemon comparison, but when it comes to the world of apparel, not much is proprietary, especially for branded clothing that has so much overlap with existing brands. Branded apparel typically commands higher margins (FIGS has proven this) so the thought of either incumbents creating 'branded' apparel or other FIGS-like competitors coming in is very likely.

In fact, one DTC company called Jaanuu hit the market shortly after Figs "with the idea to become the most disruptive and most contemporary medical apparel brand in the world." While the company doesn't release revenue information, it said in 2018 that Jaanuu saw multiple $500,000 revenue days that year and expected sales to double in 2019. It also announced that it had signed a deal to become the exclusive uniform provider for BronxCare, one of the country's largest not-for-profit hospital systems, with more than 4,000 employees.

One of the incumbent brands, Barco, has been around since 1929 and licenses the Skechers and "Grey’s Anatomy" brands in addition to producing scrubs under its proprietary label. One in three healthcare professionals in the U.S. has purchased Barco-made scrubs, and the company has doubled in size in the past nine years without any outside funding.

Even though the fabric might be nice, comfortable, and form-fitting, price sensitivity is very real when you look at the median wage for healthcare practitioners (such as registered nurses, physicians and surgeons, and dental hygienists) is ~$70k. Doing a quick side-by-side comparison of three brands, Greys Anatomy, Jaanuu, and FIGS, I've identified one single woman, black, 3-pocket v-neck top on all sites and provided the price comparison.

Grey's Anatomy - $31.50 MSRP, $23.50 discounted

Jaannuu - $36 MSRP, $18 discounted

FIGS - $38

Quick comparison puts FIGS as the most expensive, marginally to closest competitor Jaanuu, but 21% more expensive than Grey's Anatomy. Additionally, I've only given the percentage off the MSRP price which at face value doesn't look that bad but in fact, if you factor in the current discount, it gets worse. FIGS becomes 62% more expensive than Grey's Anatomy and 111% more than Jaanuu. *Note, I pulled these prices pre-black Friday so I'm not sure if this is a holiday promotion or just a normal promotion.

FIGS is not like lululemon where you can buy multiple pairs of leggings and yoga pants and not have to replace them too often. These are scrubs, which depending on your line of work and not getting into too much nasty detail can be very dirty. Either way, for many across the market that would wear scrubs, having to buy five or more pairs of scrubs on a regular basis might want you to reconsider buying premium if you're going to go through them quite often.

What the customer is saying

What really ticked me off to change my mind from going LONG on the company and considering it a potential SHORT was when I was looking at reviews online. So many youtube videos of people doing honest apparel reviews and so much positive PR out there that I thought something looked too good to be true. This led me to talk to actual people that worked in the industry. These were women that worked in various fields of the medical industry (nurses, social workers, med-students, practicing physicians, and dental hygienists). These working professionals owned anywhere from 3 to 10 sets of scrubs at a time. I asked them all three simple questions (with follow-ups if I needed more clarity):

Do you wear FIGS, if so why, and if not, why not?

If you do wear FIGS, why do you like them and what reasons would you give for buying them over competitor brands?

What would keep you from buying FIGS?

The most common things that I got from them all almost seemed like they practiced together. They all said that they liked the colors that you can't typically get from other places, the fit was nice, and the fabric was comfortable.

What I also got was that some said FIGS was the "it" thing to have. Some bought because they were "on-trend" and if you had them you were essentially "cool." While I am a fan of trends, trends in the apparel business are hard to maintain unless you just keep absolutely killing it with rollouts which made me initially skeptical when I heard that.

The reasons that I received about not buying them in general or purchasing additional ones were for the following reasons:

People might not pay for them once price reality hits them when they no longer labeled cool anymore

Would not purchase them on a regular basis because they're pricey

Many are wearing their scrubs for longer and consider FIGS to be a luxury item

They're a bit overpriced for what they are and I feel people try to justify it by convincing themselves how comfortable they are

Their colors don't always line up well with what I need at the hospital (got that one a lot)

While I boasted earlier that many of their sales were coming from repeat business in 2020 (62%), I'm concerned because since this is technically a majority of overall sales, any slowdown in current customers purchases from the reasons above could have a significant impact on their sales going forward.

So while many still love the product, I grew concerned about what I was hearing that would lead them to be repeat customers for their core product, scrubs.

Heavily concentrated in core products

According to the company S-1, 82% of the company's sales in 2020 came from their core styles. These core styles are an assortment of 13 articles of clothing (3 women's scrub tops, 4 women's scrub pants, 3 men's scrub tops, 3 men's scrub pants) all offered in six colors. 5% of their 2020 sales came from limited-edition scrub wear styles and 13% came from their lifestyle brand. What's worrying is that the company's sales are so focused on a particular area (core styles) that maintaining rapid growth rates appears difficult to achieve. This hypothesis is further supported by a callout in their S-1 that said:

We launch limited edition colors or styles approximately weekly, driving recurring traffic to our digital platform where customers often purchase limited edition products along with our core offerings. These launches not only drive interest in the limited edition products themselves, they also drive our core business, as, on average, 90% of sales on launch days are core styles.

If I'm interpreting this right, it almost seems like they're purposely creating new products to drive traffic to their site which ends up having customers buying their core styles instead. 90% to be exact. Though this was written in the company's "Highly Effective Merchandising and Product Launch Model" section, I'm not sure that creating products to drive traffic to your existing products is the best use of resources if only 10% of launch day sales end up being the new product. From personal experience in the industry I work in, launch days should be the biggest pop of sales for that product for a good while as a lot of marketing/CRM efforts go into the launch. High, continued growth rates are a concern here for me.

Growth in other uniform categories/international is overly ambitious

Another area that I've noticed many speaking on is their continuous call for international expansion and industry expansion. As mentioned, the company operates internationally in Canada, the UK, and Australia and as of the fiscal year 2020, 4.8% of all sales were generated abroad. While international expansion is a natural growth avenue for many companies, I'm curious to know why they've begun doing so while they in theory have plenty of runway here domestically. International expansion has never not been expensive and while the company is currently profitable now, penetrating a few new markets, despite having a large TAM of $67 billion in 2020, could have a negative impact on their bottom line as they increase marketing spend.

The other point is expanding into new industries that require uniforms. Management has said that these areas include; foodservice, hospitality, construction, and transportation. Though they haven't specified yet exactly which part of each market they'd likely target, I'm skeptical that they could make much disruption in an arguably lower-wage job, and buying premium uniforms doesn't quite fit the budget.

If you look at the average wages of each category, they don't seem like an obvious fit without additional context from management.

Foodservice - $27k

Hospitality - $33k

Construction - $50k

Transportation - $39k

Call me crazy but this might seem like an obvious choice because of 'uniforms' but not so much for people that buy premium products. Even in the company's S-1, they mention that 2/3 of their customer base make less than $100k and 1/3 make less than $50k. Doesn't look like the data supports the largest portion of whom they get their most business from.

Tasteless ad alienated customers

In October of last year, the company posted a very tasteless and quite offensive video of a woman in FIGS scrubs holding an upside-down "medical terminology for dummies" book misrepresenting healthcare professionals and DOs (doctor of osteopathic medicine).

The American Osteopathic Association says there's a harmful stigma toward DOs, who make up 11% of the physician workforce. Both DOs and MDs are trained physicians who are licensed by the same accrediting body. (The main difference is that DOs receive additional training in "whole-body" techniques, as holistic physicians.)

On Twitter, a handful of women health care professionals and DOs quickly criticized the video's contents and FIGS for producing it.

YouTube influencer and family physician Dr. Mike Varshavski encouraged medical students to stop wearing scrubs from the brand.

They're willing to put women down; they're willing to put DOs down to make more money. If they truly cared, there would be checks and balances in place to prevent this.

FIGS apologized for the video and pledged to donate $100,000 to the American Osteopathic Association, an organization for DOs, after the video generated backlash among Twitter's vibrant medical community.

This was definitely a setback for the company and considering how tight-knit the community is in this industry, I'm sure it has both permanently led to eligible customers to never support FIGS and pushed some towards the middle of the road on who to buy from next.

Rate of insider selling is alarming

While insider selling doesn't always suggest that the company might be headed into bad shape, FIGS has had some interesting movements from insiders since its IPO. One insider, in particular, is what caught my eye. Catherine (Trina) Spear.

On the 15th of November, Catherine Spear sold around 89k shares on-market at roughly $34.29 per share. This was the largest sale by an insider in the last 3 months. This was Catherine's only on-market trade for the last 12 months.

This transaction netted her ~$3.1 million and essentially meant that she sold 96% of her Class-A equity. Looking at the total insider shareholdings in a company can help to inform your view of whether they are well aligned with common shareholders. While it's usually not the best look for an insider to sell shares, it's not a good sign for the conviction of the future upside of the company.

Valuation is absurd

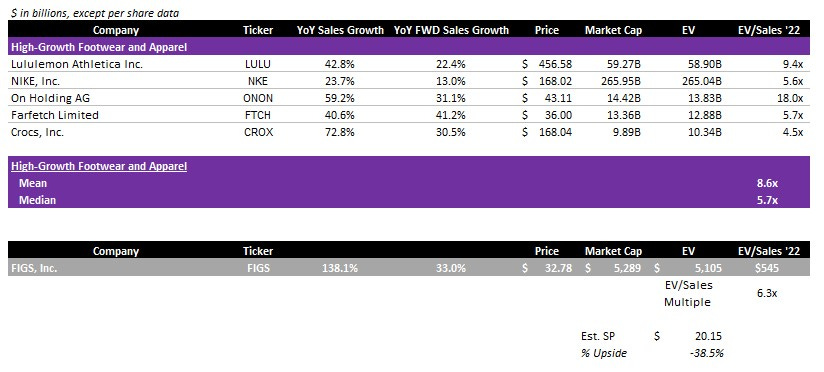

Now for the meat and potatoes, valuation. FIGS does have a rich valuation currently being priced at 12.5x FY'21 EV/Sales. When thinking about comps for this company I wanted to pick companies that operate in a similar space (being footwear and apparel) and also have a high growth rate to closely compare with FIGS trajectory. I explicitly excluded any healthcare companies because even if I were to find any close comparisons, they wouldn't be close to being apples to apples and they'd be slower growth.

This led me to the following companies that have great brand loyalty, similar past and forward growth rates, and sell in the apparel and footwear industry.

Even if the company were to fulfill the target of 33% sales growth for the fiscal year 2022, and strip out ON (ONON), you get a median EV/sales multiple of 6.3x and a price of ~$20. Though I'd rather not use EV/sales multiples, there was no point in analyzing EBITDA or P/E multiples since the company is still in the growth phase and was posting numbers in the upper 3-digits, some being 4-digits.

Even lululemon (LULU) which many have made the comparison to does not trade above 10x FY'22 sales and they have a long and proven track record of outperforming by posting double-digit growth rates.

Conclusion

Big fan of the company and the product but unfortunately, not the stock. Especially in this volatile market, high-growth companies that were trying to command high valuation multiples have been slaughtered, even if they don't raise guidance enough to convince investors to stay.

At these levels, I believe there's more risk than reward given new COVID variants shaking the markets and clear impacts of inflationary prices compressing margins everywhere.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Short position through short-selling of the stock, or purchase of put options or similar derivatives in FIGS over the next 72 hours.

Until next time,

Paul Cerro | Cedar Grove Capital