[SHORTs Update] Buy to Cover +36.5%

If you haven't already, it's time to cover most the SHORT positions from earlier in the year

Background

Throughout this year, I published multiple SHORT articles on five companies in various categories.

Chewy CHWY 0.00%↑ - article here

The Honest Co HNST 0.00%↑ - article here

Virgin Galactic SPCE 0.00%↑ - article here

AppHarvest APPH 0.00%↑ - article here (original) + follow up here

Robinhood HOOD 0.00%↑ - article here

Four out of the five companies have each hit the price targets that I initially wrote for them, and then some. You can take a look at the chart below which outlines the current return as of 10.29.21 and how many days it took to hit my PT.

If you decided to act on my research of each, you’ve made quite a pretty penny if you haven’t sold yet. Though the percentages are quite nice, let’s apply a dollar value to it for reference.

Had you invested $1,000 in each of the five stocks ($5,000 initial investment), you’d have an account value of $6,823 as of me writing this post. That’s a 36.5% return from your initial investment in less than half a year.

But, with that being said, if you have not sold yet I would strongly recommend you lock in your gains. Being greedy can really make you regret things later on.

I’ve included commentary below on the five stocks I’ve covered which includes:

My original thesis

How accurate it was (did I account for all, some, or few of what drove the price down)

What inevitably made me write this article to cover

Select Commentary

AppHarvest

Ticker: APPH

Original Thesis: When I first took a look at AppHarvest, I was a fan because of what they were trying to accomplish, farming vegetables in an efficient way. In their investor presentation, they had all the right things too: how they were going to scale their business, new farm expansions, technology for capturing heat, reusing water, etc.

All of this seemed great, except for one thing, it was too good to be true. AppHarvest was just starting out and I was betting that it would take a lot longer for management to realize the over ambitious sales goals that they were trying to achieve. I said that they would run into problems that would just increase costs and delay their roll-outs of their other farms thus sending its shares cratering.

Even in my original analysis, I gave them the benefit of the doubt and said they were worth $9 a share based on just a 5% haircut on the remaining years past 2021E.

My valuation perspective was more so on a multiple re-rating than a steep sales growth decline which proved to be way too generous of a discount factor given what happened next.

What Played Out: All came to light once they released their Q2 figures. At the end of the first quarter, AppHarvest said it expected $20 million to $25 million in sales in 2021, which would be quite strong from just one tomato farm. However, in Q2, that figure was dropped to $7 million to $9 million.

Considering that AppHarvest sold $3.1 million in product this quarter and $2.3 million last quarter, AppHarvest is predicting a terrible second half of the year. Even if they reach their higher estimate of $9 million in sales, this would represent second-half 2021 revenue of $3.6 million, divided into two separate quarters. This would mean that, if revenue was split equally between Q3 and Q4, AppHarvest would only have $1.8 million in sales each quarter, or 58% of their total sales from this quarter.

Why Sell Now: Based on the sales miss mentioned above, adjusted guidance really damages the long-term revenue outlook for their business. AppHarvest is supposed to be a fast-growing company, so a huge reduction in guidance can have a big impact on the share price. The stock has dropped well below where I initially covered. Like, more than 33% lower. At this point, the company has net debt per share of ~$2 and while it bottomed out at $5.08, the R/R (risk/reward) is worth locking in gains now rather than potentially deal with unnecessary volatility and allocate funds elsewhere.

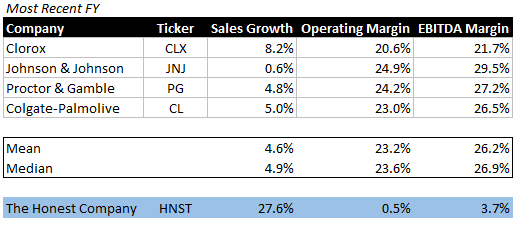

Honest Co.

Ticker: HNST

Original Thesis: To begin with, I just dislike Jessica Alba. This stems from a movie I saw with her in it that really pissed me off and I forever disliked her after that (Awake). Anyways, when it came to her company going public earlier this year, I knew it was crap the second they came out with the valuation that they were targeting. They were aiming for a ~$1.5B valuation which I knew was BS.

Despite my unwarranted loathing of her, I like what the company was doing → creating eco-friendly consumer products for your household and yourself. What I didn’t like, was that a lot of their growth came from their household cleaning products during COVID and they projected that their growth would moderately slow down in rapidly growing categories. I thought otherwise.

What I also found distressing was that their operating margins were trailing that of other CPG peers.

Though they were growing faster, they just weren’t able to generate anywhere close to the same level of margins their other peers were. Yes, I did account that the other CPG players have been established for some time and I gave HNST the benefit of the doubt that in 5 years’ time, they could increase their margins to just 12.5% (highly unlikely and only HALF what others were accomplishing).

With that in mind, I plugged that assumption into my DCF and I still did not get anywhere close to the >$16 per share they were offering at their IPO.

Even with this highly unlikely outcome taking place, I arrive at a per-share price of $11.30. Well below the ~$21 price it was trading at while I was writing the article.

At the end of the day, like I mentioned in my initial article, they're selling baby wipes and cleaning supplies. Nothing about this is screaming high multiple valuation. Not then, not now.

What Played Out: Just like most catalysts that set in motion short positions, earnings came out. Long story short, they haven’t been good.

In June, the company posted first-quarter results, with shares still trading at $18 at the time. Revenues were up 12% to $81.0 million, just ahead of the guidance as flattish sales in the key diapers and wipes category were more than offset by strong growth in skin & personal care and household & wellness products. Worrisome is that 12% revenue growth looks slow in relation to a 54% increase in marketing expenses, resulting in an operating profit of $0.7 million turning into a loss of $4.1 million.

Second-quarter sales were up just 3% to $74.6 million, marking some sequential revenue declines. Adjusted for a positive impact by the pandemic last year, growth is estimated at around 9%. Operating losses ballooned to $19.5 million. Some $10.6 million of these losses were the result of IPO-related costs. Adjusted for that, still, a $9 million loss was reported, in part because of higher stock-based compensation expenses following the public offering.

Why Sell Now: The stock has been punished enough for me to recommend taking money off the table and reallocating elsewhere. Over the last couple of months, it's been trading within a band of ~$9 - ~$10 and with two quarters officially in the books, Wall Street has adjusted earnings to be less optimistic than they initially had thought. Going forward, investors should have better visibility in what management can and cannot execute on and the R/R leans more positive here for the upside.

Virgin Galactic

Ticker: SPCE

Original Thesis: Believe it or not, I actually liked, and still do like the company. However, I hate the stock. Aside from it being a meme stock a few times and rallying off of little to no meaningful news, this stock has proven to be highly volatile.

My main thesis was three-fold, 1) I believed that they were going to not launch as many spaceships into the atmosphere as they had scheduled, 2) the price was too expensive for many elites to want to just throw that much cash away on a regular basis for the business to be sustainable and, 3) they would need to raise more money in order to fund operations and build out new craft and launching stations.

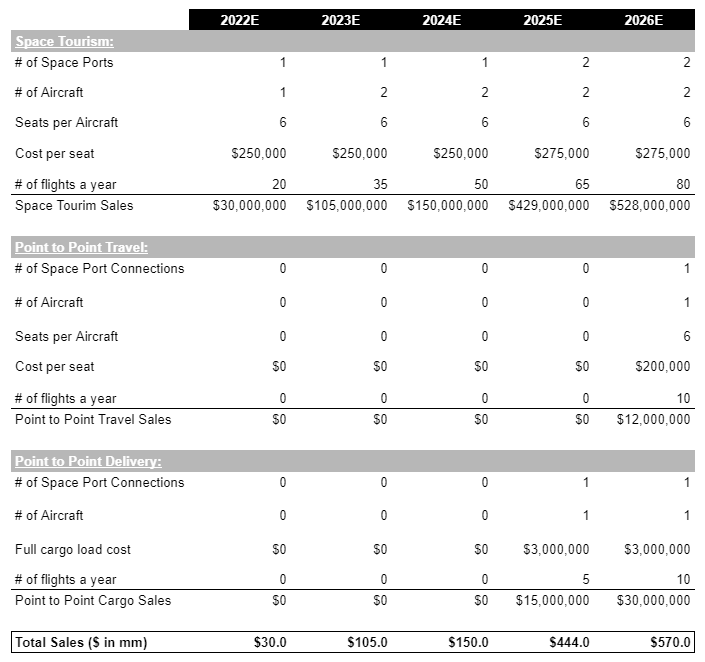

I modeled out for everyone what I presumed would transpire given the price, B2C and B2B operations.

Taken from my original article,

Considering that they are charging $250,000 per ticket for a human ($1.5m per full flight), then a cargo load of double that ($3m) is not that farfetched.

Even with these numbers starting in 2022, factoring the number of flights that grow over time that aren’t affected by weather or any other issues bridges me to just $444m in 2025 compared to a consensus of $550m.

Virgin Galactic has 240m shares outstanding, of which 164.6m are available to the public for trading – which is known as float. Based on Friday’s closing price of $49.20, Virgin’s $500m offering would equate to nearly 10.2m shares.

Factoring in fully diluted share estimates after their $500M stock offering ~250m shares, at a more than a generous forward multiple of 200x and 2022E sales of $30m (13.5x 2025E sales), gets you a price per share of $24.00, best case scenario.

No chance a virtually pre-revenue company was worth that much.

What Played Out: First off, following Branson's flight over the summer, Virgin Galactic reopened ticket sales with prices starting at $450,000 per seat during its Q2 earnings report on Aug. 5. The starting price is above the previous price point of $250,000. So far, 600 people have booked space flights before ticket sales were closed.

If it was already a small pool of people to begin with when the prices were that low, it got even smaller after they increased prices by 80%. This essentially just reduced the TAM from a pure number of individuals that have that kind of petty cash laying around. No bueno.

Also, like I predicted, the company said on Oct. 14 that it would delay the start of commercial flights until the fourth quarter of 2022 as it starts its lengthy enhancement and refurbishing program.

The commercial space company also reshuffled some test launch targets. It now expects the Unity 23 test flight with the Italian Air Force, which was originally targeted for late October, to fly after the enhancement program is completed next year.

Virgin Galactic had expected commercial service to start in late Q3, later than a previous timeline for early 2022, which was pushed back from early 2021.

But Virgin Galactic said the delay was unrelated to a supplier warning of a possible "manufacturing defect" in a component of the flight control actuation system in September.

Why Sell Now: It’s just too speculative to gauge what will happen including that it is still a meme stock and prices can swing up and down by +/- 20% at a moments notice. Just from announcing Branson would go to space, the stock popped 20% and after he went up, the stock also sank ~20% as well. Too unpredictable and too removed from reality of the markets for me to accurately determine where it's going to go.

Could the stock still drop further, sure, but at the same time I would rather lock in the gains and allocate elsewhere than stomach another insensible +20% move.

Chewy

Ticker: CHWY

Original Thesis: Chewy is a great company and they have rewritten the playbook on how consumers buy their pet products via e-commerce. They've grown their business considerably during COVID and increased two key metrics every quarter for the last few years, 1) the number of active customers that shop with them within a certain time frame and, 2) the average sales per active customer.

Despite this and the support of overall tailwinds, I foresaw the company running into some headwinds. The pull forward during COVID was not sustainable in the long-term, competition was becoming more fierce between larger players like Amazon, Walmart, Petco and Target and because of this, marketing expenses would increase in order to meet the same level of growth as they had during COVID.

What Played Out: Chewy reported Q2 2021 earnings after the market closed on Sept. 1, 2021. The results were solid; however, the guidance for the remainder of the year disappointed investors, sending the shares down over 9% the following day. The company is now projecting sales growth of 26% for fiscal 2021 (the fiscal year ends Jan. 31, 2022). This is a rapid deceleration of growth compared to the 47% sales growth registered in fiscal 2020.

During the conference call for investors, CFO Mario Marte said that although supply chain issues are improving, "Out-of-stock levels remained elevated in the second quarter." He added that the current macro environment makes forecasting difficult, but "Consumers may have started redirecting some of their discretionary spending back to areas like travel or dining out." That could imply that consumers might splurge less on toys or extra treats for their pets.

Why Sell Now: Actually, I recommended selling the stock when it came within a few percentage points of my $65 PT back on May 12th on Twitter. Since then, it’s floated around in the $60s and even briefly touched up in the mid-90s in August, though has come down since then.

They’ve also been making more pushes into the healthcare side of pets which is pretty lucrative. So, with the addition of a new strategy of pet health, things have changed and I think at these levels, the market has allowed it to bottom out and the R/R leans more towards the upside since its massive drop from its 52-week high of $120.

One last thing!

Writing about the stock market and individual companies is something that I enjoy doing and I work on all these posts in my free time.

As I look to grow this community, I ask that if you think your friends could benefit from this newsletter, please feel free to share it with them and make sure you subscribe to never miss out on a money-making idea.